The week began with the stock market picking up where it left off the previous week. Each of the benchmark indexes listed here advanced in value, led by the tech-heavy Nasdaq, which jumped 1.10%, pushed higher by Amazon and Adobe. Last Monday’s run marked the seventh straight advance for the Nasdaq — its longest rally of the year. The Russell 2000 gained 1.00%, followed by the S&P 500, the Dow, and the Global Dow. Crude oil reached $40 per barrel for the first time in quite a while, the dollar dropped, and the yield on 10-year Treasuries inched higher. Stock values climbed despite the accelerating number of COVID-19 cases reported.

Tuesday saw both the Nasdaq and Russell 2000 continue to surge. In fact, the Nasdaq hit an all-time high as investors seemed to focus on signs of economic growth and the expectation of more government stimulus. President Trump tweeted that the U.S.-China trade deal remains fully intact, which further encouraged investors despite U.S. health advisor Anthony Fauci’s warning of a disturbing surge in COVID-19 cases. Apple, Amazon, and Microsoft were winners at the end of the day, as were road and rail stocks, real estate, utilities, airlines, and retailers.

Stocks took a nosedive midweek as the growing number of reported COVID-19 cases was too much for investors to ignore. The pandemic is prompting fears that renewed restrictions will slow economic growth. Money poured into bonds, pushing prices higher and driving yields lower. Among sectors taking a particularly hard hit last Wednesday were energy, financials, and industrials. Airline stocks, which had been climbing as restrictions eased, got pummeled. Each of the indexes listed here took a sizeable hit, led by the small caps of the Russell 2000, which gave back nearly 3.50%. The Dow closed down 2.72% on the day, followed by the Global Dow, the S&P 500, and the Nasdaq, which ended its run of daily gains by sinking 2.19%.

Thursday was a better day for equities as each of the benchmark indexes listed here posted gains, led by the Russell 2000, which climbed nearly 2.00%. Bank stocks enjoyed a good boost after the Federal Deposit Insurance Corporation eased limits on bank risk-taking. As stocks climbed, more bad news came from the COVID-19 front. Thursday, the number of new virus cases surpassed April’s peak, prompting the governor of Texas to pause the process of reopening. Also, new weekly claims for unemployment insurance approached 1.5 million — a figure that’s lower than the prior week, but still indicative of the number of people who have lost their jobs.

Both Texas and Florida imposed new restrictions as reported virus cases surged last Friday, sending stocks tumbling. These are the first states to reimpose restrictions, although several other states are considering added restrictions and/or delaying reopenings. The Dow fell 2.84%, the Nasdaq dropped 2.59%, and both the S&P 500 and Russell 2000 gave back more than 2.40%, respectively.

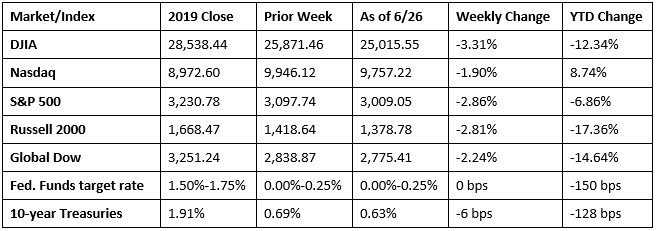

For the week, each of the benchmarks lost notable value, led by the Dow, which fell more than 3.30%. Clearly, rising COVID-19 cases throughout several parts of the country have curbed investor enthusiasm over encouraging economic news. The market swung up and down for much of the week, with bank stocks being particularly volatile. After the FDIC eased restrictions on bank investing last Thursday, the Federal Reserve indicated its plan to restrict banks’ sharing of profits through dividends and share repurchases. Of the remaining indexes listed here, the S&P 500 fell back into correction territory after dropping 2.86%. The small caps of the Russell 2000 lost nearly 3.00%, the Global Dow declined nearly 2.25%, while the Nasdaq fared the best, losing less than 2.00% for the week.

After climbing higher the week before, crude oil prices sank lower last week, closing at $38.10 per barrel by late Friday afternoon, down from the prior week’s price of $39.50. The price of gold (COMEX) advanced again last week, closing at $1,784.10 by late Friday afternoon, up from the prior week’s price of $1,755.10. The national average retail regular gasoline price was $2.129 per gallon on June 22, 2020, $0.031 higher than the prior week’s price but $0.525 less than a year ago.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The third and final estimate of the gross domestic product for the first quarter of 2020 showed the economy slowed at an annual rate of 5.0%. In the fourth quarter, the GDP increased 2.1%. A main contributor to the deceleration of the economy in the first quarter was consumer spending, which fell 6.8%, exhibiting the initial impact of the pandemic. Business investment fell 1.3%, although residential investment soared 18.2%. The personal consumption expenditures price index increased 1.3%. Excluding food and energy prices, the PCE price index increased 1.7%.

- According to the latest report from the Bureau of Economic Analysis, consumer spending ramped up 8.2% in May following downturns in March and April, when personal consumption expenditures fell 6.6% and 12.6%, respectively. Consumer prices inched ahead 0.1% last month and are up 0.5% since May 2019. Personal income sank 4.2% last month and disposable, or after-tax, income dropped 4.9%, each figure impacted by a decrease in payments from federal economic recovery programs.

- The international trade in goods deficit was $74.3 billion in May, up $3.6 billion from $70.7 billion in April. Exports of goods for May were $90.1 billion, $5.5 billion less than April exports. Imports of goods for May were $164.4 billion, $1.9 billion less than April imports.

- Existing home sales fell 9.7% in May, declining for the third consecutive month. Overall, existing home sales are down 26.6% from a year ago. The median existing-home price for all housing types in May was $284,600, down from April’s $286,800 but 2.3% ahead of the May 2019 median sales price ($278,200). Total housing inventory at the end of May totaled 1.55 million units, up 6.2% from April but down 18.8% from one year ago (1.91 million). Unsold inventory has increased, sitting at a 4.8-month supply at the current sales pace, up from 4.0 months in April.

- While existing home sales may have fallen in May, sales of new homes soared. According to the Census Bureau, sales of new single-family homes in May were 16.6% above the April total and 12.7% ahead of May 2019. The median sales price of new houses sold in May 2020 was $317,900 ($303,000 in April). The average sales price was $368,800 ($352,300 in April). The estimate of new houses for sale at the end of May was 318,000, which represents a supply of 5.6 months at the current sales rate.

- New orders for manufactured durable goods rebounded in May, advancing 15.8% over April’s totals. Transportation equipment, primarily vehicles and aircraft, led the increase, climbing a whopping 80.7%. Excluding transportation, new orders increased 4.0% with orders for core capital goods (nondefense capital goods excluding aircraft) up 2.3%. Shipments of durable goods increased 4.4% in May following April’s 18.6% decline. New orders for nondefense capital goods in May increased 27.1%. Shipments increased 0.4%.

- For the week ended June 20, there were 1,480,000 claims for unemployment insurance, a decrease of 60,000 from the previous week’s level, which was revised up by 32,000. According to the Department of Labor, the advance rate for insured unemployment claims decreased 0.5 percentage point to 13.4% for the week ended June 13. The advance number of those receiving unemployment insurance benefits during the week ended June 13 was 19,522,000, a decrease of 767,000 from the prior week’s level, which was revised down by 255,000.

Eye on the Week Ahead

The employment numbers for June are out this week. May’s report was unexpectedly favorable with 2.5 million new jobs added. However, weekly unemployment claims continue to remain in the millions, which could be an indication that June’s employment figures may not be as favorable as they were the previous month.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.