Stocks jumped to record highs last Monday after President Trump signed a pandemic relief package into law. The S&P 500, the Dow, and the Nasdaq closed the day at record highs as investors saw the stimulus relief as a boost to economic recovery. Only the small caps of the Russell 2000 failed to advance, ending the day down 0.4%. Treasury yields rose, crude oil prices fell, and the dollar was mixed. Several market sectors climbed higher, led by communication services, consumer discretionary, and information technology.

Equity indexes gave up early gains last Tuesday, ultimately closing lower. The Russell 2000 fell 1.9%, followed by the Nasdaq (-0.4%). The Dow and the S&P 500 dropped 0.2%. The Global Dow gained 0.4% on the heels of last week’s trade deal between the United Kingdom and the European Union. Crude oil prices and Treasury yields advanced, while the dollar declined. Consumer discretionary and health care were the only major market sectors to post gains on the day.

Investors reacted positively to the passage of the latest round of fiscal stimulus in the hopes that it will give the economy a boost entering 2021. Each of the benchmark indexes posted gains last Wednesday, with the small caps of the Russell 2000 outperforming large caps and tech stocks. Treasury yields fell as did the dollar, while crude oil prices advanced. Among sectors, energy, industrials, financials, and materials performed the best, while communication services fell.

The last day of the month and year saw both the S&P 500 and the Dow close at record highs. Utilities, financials, real estate, and health care all gained more than 1.0% on the day. Treasury yields, crude oil prices, and the dollar closed up by the end of trading last Thursday.

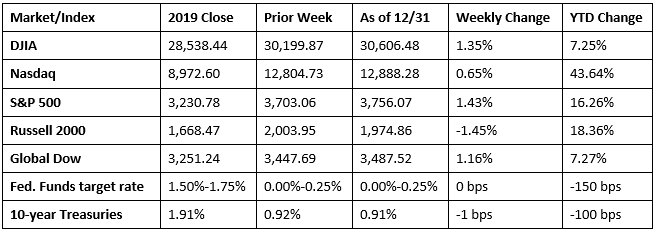

The last week of December and 2020 was generally a good one for stocks. Only the small caps of the Russell 2000 failed to post a gain. The remaining benchmark indexes closed ahead, led by the S&P 500, followed by the Dow, the Global Dow, and the tech stocks of the Nasdaq. Stocks recovered in fine fashion from their COVID-impacted drop, as each of the indexes listed here closed well ahead of their 2019 year-end value, led by the Nasdaq, the Russell 2000, the S&P 500, the Global Dow, and the Dow.

Crude oil prices ended the last week of the month and year slightly higher, closing at $48.43 per barrel by Thursday afternoon, up from the prior week’s price of $48.23 per barrel. The price of gold (COMEX) closed last week at $1,901.70, up from the prior week’s price of $1,883.20. The national average retail price for regular gasoline was $2.243 per gallon on December 28, $0.019 higher than the prior week’s price but $0.328 less than a year ago.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The international trade in goods deficit was $84.8 billion in November, up 5.5% from the October total. Exports of goods for November were $127.2 billion, 0.8% higher then October. Imports of goods for November were $212.0 billion, up 2.6% over October imports.

- For the week ended December 26, there were 787,000 new claims for unemployment insurance, a decrease of 19,000 from the previous week’s level, which was revised up by 3,000. According to the Department of Labor, the advance rate for insured unemployment claims was 3.6% for the week ended December 19, unchanged from the prior week’s rate. For comparison, during the same period last year, there were 220,000 initial claims for unemployment insurance, and the insured unemployment claims rate was 1.2%. The advance number of those receiving unemployment insurance benefits during the week ended December 19 was 5,219,000, a decrease of 103,000 from the prior week’s level, which was revised down by 15,000. States and territories with the highest insured unemployment rates in the week ended December 12 were in Puerto Rico (7.5%), the Virgin Islands (6.8%), Alaska (6.5%), Nevada (6.2%), New Mexico (6.2%), California (5.8%), Kansas (5.8%), Pennsylvania (5.8%), Illinois (5.7%), and Hawaii (5.2%). The largest increases in initial claims for the week ended December 19 were in Pennsylvania (+8,047), Illinois (+6,695), Colorado (+4,544), Georgia (+2,971), and Florida (+2,591), while the largest decreases were in California (-45,727), New York (-17,047), Ohio (-7,209), Kansas (-4,290), and Texas (-3,666).

Eye on the Week Ahead

The employment figures for December are out this week. There were 245,000 new jobs added in November, well below the October and September totals. Also out this week are the December purchasing managers’ surveys for manufacturing and services. Growth slowed in both manufacturing and services sectors in November.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.