Stocks retreated from record highs last Monday. The S&P 500 fell 0.5% — its largest single-day drop in nearly four weeks. Small caps and tech shares dove lower, pulling down the Russell 2000 (-1.4%) and the Nasdaq (-1.0%). The Dow slipped 0.4% and the Global Dow was unchanged. Crude oil prices rose and Treasuries advanced, while the dollar fell. Among the market sectors, only real estate was able to post a modest (0.3%) gain. Consumer discretionary plunged 1.1% and information technology declined 0.9%.

Last Tuesday, stocks fell for the second consecutive day, despite an initial round of solid corporate earnings reports. Investors may be concerned that the growing number of virus cases at home and around the world may stunt economic recovery. The small caps of the Russell 2000 dropped 2.0%, followed by the Global Dow (-1.6%), the Nasdaq (-0.9%), the Dow (-0.8%), and the S&P 500 (-0.7%). Among the market sectors, energy plunged 2.7% as crude oil prices sank. Financials declined 1.8%, consumer discretionary dipped 1.2%, and industrials lost 1.1%. Utilities (1.3%) and real estate (1.1%) advanced. The dollar rose slightly, while the yields on 10-year Treasuries fell 2.4%.

Stocks gained last Wednesday for the first time in three days. More favorable earnings reports may have influenced investors, but the greater likelihood for the stock surge can be traced to dip buyers. In any case, the Russell 2000 led the advance, gaining 2.2%, followed by the Nasdaq, which climbed 1.2%. Both the Dow and the S&P 500 increased 0.9%, while the Global Dow moved up 0.3%. Communication services and utilities were the only market sectors to fall. Materials (1.9%), energy (1.5%), industrials (1.4%), and consumer discretionary (1.3%) advanced. Yields on 10-year Treasuries inched up, while crude oil prices and the dollar fell.

Equities tumbled last Thursday following a report that President Biden may propose a substantial increase in the capital gains tax for the wealthy. Each of the benchmark indexes plunged, with the Dow, the S&P 500, and the Nasdaq each falling 0.9%, followed by the Russell 2000 (-0.3%), and the Global Dow (-0.2%). Each of the market sectors also sank, with materials, energy, information technology, consumer discretionary, and financials each declining more than 1.0%. Treasury yields fell, while the dollar and crude oil prices advanced.

Dip buyers pushed stocks higher last Friday following Thursday’s plunge. The Russell 2000 and the Nasdaq climbed the highest, adding 1.8% and 1.4%, respectively. The S&P 500 reached another record high after advancing 1.1%. The Dow climbed 0.7% and the Global Dow gained 0.6%. Treasury yields and crude oil prices rose, while the dollar fell. Nearly all of the market sectors increased, led by financials, materials, information technology, and communication services. Consumer staples and utilities fell.

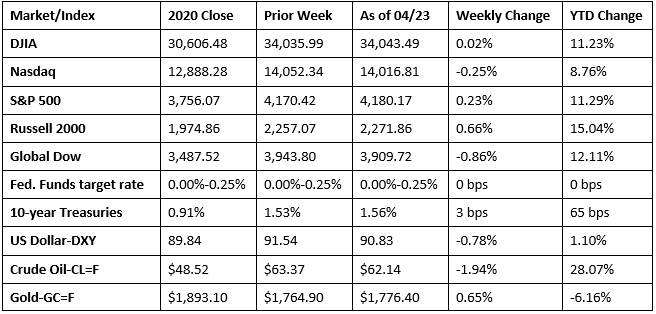

The possibility of a capital gains tax hike proposed by President Biden sent stocks reeling last week. However, bargain hunters plucked enough low-hanging stocks to push several of the benchmark indexes higher by week’s end. The market sectors closed the week mixed, with real estate and health care leading the way. Energy and consumer discretionary each dropped more than 1.0%. The Dow, the S&P 500, and the Russell 2000 eked out gains last week, while the Nasdaq and the Global Dow lost value. The yields on 10-year Treasuries inched higher. Crude oil prices dropped nearly 2.0%, yet remained over $62.00 per barrel. The dollar fell, while gold prices advanced. Year to date, the small caps of the Russell 2000 remain well ahead of last year’s pace, with the Dow, the S&P 500, and the Global Dow more than 11.0% over their respective 2020 closing marks. The tech-heavy Nasdaq, which was the highest-gaining index in 2020, trails the other benchmarks this year, but still has added nearly 9.0% to its year-end value.

The national average retail price for regular gasoline was $2.855 per gallon on April 19, $0.006 per gallon more than the prior week’s price and $1.043 higher than a year ago. U.S. crude oil refinery inputs averaged 14.8 million barrels per day during the week ended April 16, which was 286,000 barrels per day less than the previous week’s average. Refineries operated at 85.0% of their operable capacity last week. Gasoline production decreased last week, averaging 9.4 million barrels per day.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- Sales of existing homes, which had been one of the few areas of the economy to progress during the pandemic, are now showing definite signs of slowing. According to the National Association of Realtors®, existing-home sales declined in March for the second consecutive month. Total existing-home sales fell 3.7% last month following a 6.6% drop in February. Overall, sales are 12.3% higher than a year ago. Relatively low inventory may be the primary reason for the slippage in sales volume. According to the report, unsold inventory of existing homes sits at a 2.1-month supply at the current sales pace, marginally up from February’s 2.0-month supply and down from the 3.3-month supply recorded in March 2020. The median existing-home price in March was $329,100, 5.1% above the February price and up 17.2% from March 2020. Sales of existing single-family homes also fell in March, declining 4.3% from the prior month but up 10.4% from a year ago. The median existing single-family home price was $334,500 in March ($317,100 in February), up 18.4% from March 2020.

- Unlike existing homes, sales of new, single-family homes continued to surge in March. According to the latest information from the Census Bureau, sales of new single-family homes increased 20.7% over February’s total and are 66.8% above the March 2020 estimate. The median sales price of new houses sold in March 2021 was $330,800 ($345,900 in February). The average sales price was $397,800 ($394,300 in February). In March, inventory sat at a supply of 3.6 months at the current sales rate, down from 4.4 months in February.

- For the week ended April 17, there were 547,000 new claims for unemployment insurance, a decrease of 39,000 from the previous week’s level, which was revised up by 10,000. This is the lowest level for initial claims since March 14, 2020, when it was 256,000. According to the Department of Labor, the advance rate for insured unemployment claims was 2.6% for the week ended April 10, a decrease of 0.1 percentage point from the previous week’s rate. For comparison, during the same period last year, there were 4,202,000 initial claims for unemployment insurance, and the insured unemployment claims rate surged to 11.0% as the effects of the pandemic continued to impact the labor market. The advance number of those receiving unemployment insurance benefits during the week ended April 10 was 3,674,000, a decrease of 34,000 from the prior week’s level, which was revised down by 23,000. This is the lowest level for insured unemployment since March 21, 2020, when it was 3,094,000. States and territories with the highest insured unemployment rates in the week ended April 3 were in Nevada (5.6%), Connecticut (5.2%), Alaska (5.1%), New York (4.4%), Illinois (4.2%), Pennsylvania (4.2%), the District of Columbia (4.1%), Rhode Island (4.0%), Vermont (4.0%), and California (3.7%). The largest increases in initial claims for the week ended April 10 were in New York (+16,028), Florida (+9,377), Alabama (+5,517), Washington (+5,380), and Georgia (+4,759), while the largest decreases were in California (-76,082), Virginia (-23,492), Ohio (-21,831), Texas (-17,436), and Kentucky (-15,424).

Eye on the Week Ahead

Several important economic reports are available this week. The Federal Open Market Committee meets this week. Interest rates are certain to remain at their present range based on statements from Federal Reserve Chair Jerome Powell. The latest information on durable goods orders is out on Monday. New orders for durable goods fell in February, but are expected to reverse course in March. The estimate of the first-quarter gross domestic product is available on Thursday. The 2020 fourth-quarter GDP advanced at an annualized rate of 4.3%. It is expected that growth in the first quarter economic will exceed the prior quarter’s figure.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.