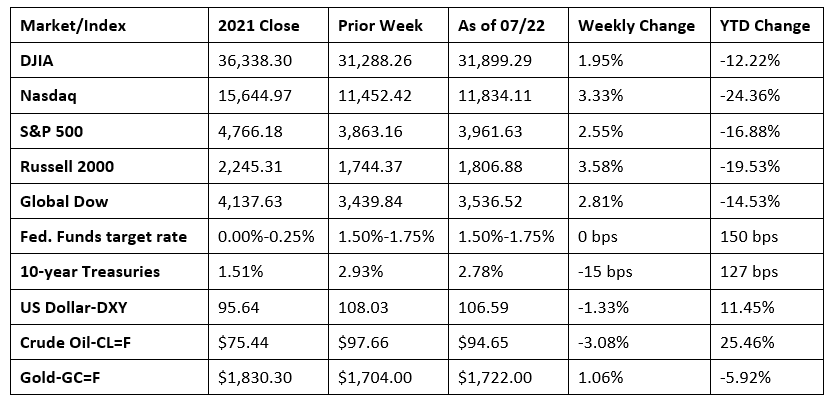

Stocks ended last week in the black, with the market posting its best week in a month. Despite a late-week decline, each of the benchmark indexes listed here posted solid weekly gains, led by the Russell 2000 and the Nasdaq. Bond prices rose, pulling yields lower. Crude oil prices ended a volatile week down by about $3.00 per barrel. The dollar edged lower, while gold prices advanced.

Wall Street began last week on a sour note as each of the benchmark indexes listed (except for the Global Dow) lost value. The S&P 500 and the Nasdaq led the declines, dropping 0.8%. The Dow fell 0.7% and the Russell 2000 dipped 0.3%. The Global Dow rose 0.6%. Tech and health-care shares waned after a large tech company announced plans to slow hiring and spending next year in anticipation of a possible economic downturn. Ten-year Treasury yields climbed 3.0 basis points to close at 2.96%. Crude oil prices gained $4.58 to push the price per barrel to $102.17. The dollar fell, but gold prices rose higher.

Stocks surged higher last Tuesday, pushing each of the benchmark indexes up by at least 2.0%. Strong corporate quarterly earnings reports may have given traders confidence that the economy is still strong, despite rising inflation and corresponding interest rates. The Russell 2000 led the upswing, gaining 3.5%, while the Nasdaq jumped up 3.1%. The S&P 500 (2.8%) and the Dow (2.4%) advanced notably. The Global Dow rose 2.1%. Crude oil prices continued to climb above $100.00 per barrel, reaching $104.10 per barrel after rising $1.50. Ten-year Treasuries added nearly 6.0 basis points to settle at 3.01%. The dollar slid lower for the second day, while gold prices advanced.

The S&P 500 posted its first back-to-back gains in nearly two weeks after advancing 0.6% last Wednesday. The Nasdaq and the Russell 2000 led the indexes, advancing 1.6% as tech shares climbed higher for the second straight day. The Dow inched up 0.2%, while the Global Dow was unchanged. Ten-year Treasury yields inched up to 3.03%. Crude oil prices slipped down to $102.61 per barrel. The dollar advanced, while gold prices fell.

Stocks enjoyed their best three-day rally since May last Thursday. Tech shares led the charge once again, with the Nasdaq gaining 1.4% by the close of trading. The S&P 500 added 1.0%, while the Dow and the Russell 2000 rose 0.5%. The Global Dow was flat for the second day in a row. Ten-year Treasury yields dipped 12.6 basis points, slipping to 2.91%, likely influenced by the European Central Bank’s 50 basis-point interest rate hike — the first one since 2011. The dollar fell, while gold prices advanced. Crude oil prices slid $3.45, reaching $96.43 per barrel.

Stocks fell last Friday, ending a three-day rally. Investors retreated from risk following disappointing earnings reports from some social media companies. Tech shares gave back much of the gains from earlier in the week, pulling the Nasdaq down 1.9%, while the Russell 2000 fell 1.6%. The large caps of the S&P 500 (-0.9%) and the Dow (-0.4%) ended the day down, while the Global Dow ended flat for the third consecutive day. Yields on 10-year Treasury yields slid nearly 13.0 basis points to close at 2.78%. Crude oil prices declined to $94.65 per barrel. The dollar dipped, while gold prices rose.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- Rising mortgage rates and overall inflationary pressure appear to be impacting new home construction. Building permits, housing starts, and housing completions fell in June following a downturn in May. Issued building permits dipped 0.6% last month but are 1.4% above the June 2021 estimate. Single-family authorizations slid 8.0% in June and are 11.4% under the June 2021 pace. Housing starts in June were 2.0% less than the May estimate and 6.3% below the June 2021 rate. Single-family housing starts were 8.1% below the May figure and 15.7% less than the June 2021 figure. Housing completions dipped 4.6% last month but are 4.6% higher than a year ago. Single-family housing completions in June were 4.1% below the previous month’s total but 8.5% higher than in June 2021.

- Sales of existing homes declined for the fifth straight month in June, according to the National Association of Realtors®. Total existing home sales dipped 5.4% last month from May and are down 14.2% year over year. Rising home prices and mortgage rates have impacted the market. The median existing home price for all housing types was $416,000 in June, up from May’s price of $408,400 and 13.4% higher than the price in June 2021. Total housing inventory for sale sits at a 3.0 month supply at the current sales pace. Sales of single-family existing homes dropped 4.8% in June and 12.8% from a year ago. The median existing single-family home price was $423,300 in June, up from $415,400 in May and 13.3% greater than the price in June 2021.

- The national average retail price for regular gasoline was $4.490 per gallon on July 18, $0.156 per gallon below the prior week’s price but $1.337 higher than a year ago. Also as of July 18, the East Coast price decreased $0.127 to $4.345 per gallon; the Gulf Coast price fell $0.190 to $4.000 per gallon; the Midwest price dropped $0.171 to $4.428 per gallon; the West Coast price slid $0.177 to $5.394 per gallon; and the Rocky Mountain price fell $0.097 to $4.850 per gallon. Residential heating oil prices averaged $3.699 per gallon on July 15, about $0.026 per gallon more than the prior week’s price. According to the U.S. Energy Information Administration report of July 20, gasoline production increased the previous week, averaging 9.4 million barrels per day. Crude oil refinery inputs averaged 16.3 million barrels per day during the week ended July 15, 321,000 barrels per day less than the previous week’s average.

- For the week ended July 16, there were 251,000 new claims for unemployment insurance, an increase of 7,000 from the previous week’s level, marking the third consecutive weekly increase for initial claims. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended July 9 was 1.0%, an increase of 0.1 percentage point from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended July 9 was 1,384,000, an increase of 51,000 from the previous week’s level, which was revised up by 2,000. States and territories with the highest insured unemployment rates for the week ended July 2 were Puerto Rico (2.1%), New Jersey (1.9%), California (1.7%), Rhode Island (1.7%), New York (1.5%), Pennsylvania (1.5%), Massachusetts (1.4%), Connecticut (1.3%), Alaska (1.2%), and Illinois (1.2%). The largest increases in initial claims for the week ended July 9 were in New York (+10,051), Kentucky (+3,061), Arizona (+2,447), Ohio (+2,274), and Indiana (+2,234), while the largest decreases were in California (-3,801), New Jersey (-3,332), Georgia (-1,859), Mississippi (-678), and Rhode Island (-484).

Eye on the Week Ahead

This week is replete with market-moving economic data, headlined by the Federal Open Market Committee meeting. Also out this week is the initial estimate of the second-quarter gross domestic product. The economy retracted 1.6% in the first quarter.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.