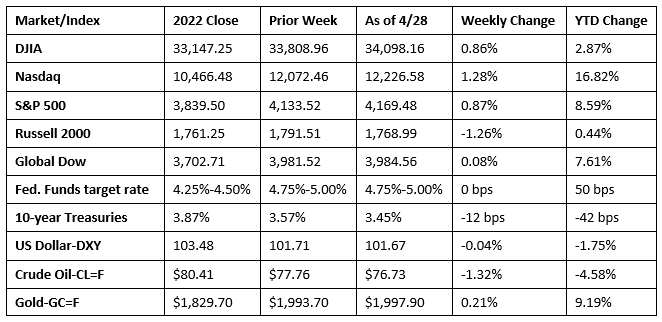

Stocks ended the week higher as strong corporate earnings data helped offset worries of another round of interest rate hikes, following the Federal Reserve’s meeting this week. Each of the benchmark indexes listed here posted weekly gains, with the exception of the Russell 2000. Ten-year Treasury yields slipped on rising bond prices. Crude oil prices ended the week lower, the dollar was flat, while gold prices advanced.

Investors were pensive at the start of last week, apparently waiting for a big week of corporate earnings before making a move. Monday saw technology, communications, and real estate lag, while health care, consumer staples, and utilities outperformed. Overall, the Dow and the Global Dow advanced 0.2%, the S&P 500 inched up 0.1%, while the Nasdaq and the Russell 2000 fell 0.3% and 0.2%, respectively. Ten-year Treasury yields dropped 5.5 basis points to close at 3.51%. Crude oil prices advanced 1.0% to about $78.66 per barrel. The dollar dipped about 0.5%, while gold prices rose 0.5%.

Stocks fell last Tuesday, pulled lower by downturns in financials, energy, technology, materials, and industrials. The Russell 2000 dropped 2.4%, followed by the Nasdaq (-2.0%), the S&P 500 (-1.6%), the Global Dow (-1.1%), and the Dow (-1.0%). Treasury bonds gained value, dragging yields lower, with the yield on 10-year Treasuries falling nearly 12.0 basis points to 3.39%. Crude oil prices fell to $77.09 per barrel amid concerns over weakening demand. The dollar and gold prices advanced.

Tech shares led the way last Wednesday on an otherwise lackluster day for stocks. Utilities, health care, industrials, energy, financials, and materials tumbled lower. Of the benchmark indexes listed here, only the Nasdaq closed higher, ending the session up 0.5%. The Russell 2000 led the declining indexes after giving up 0.9%, followed by the Dow (-0.7%), the S&P 500 (-0.4%), and the Global Dow (-0.4%). Bond prices slipped lower as yields increased, with 10-year Treasury yields closing at 3.42%. Crude oil prices continued to swoon, falling 3.5% to $74.39 per barrel. The dollar and gold prices declined.

Wall Street enjoyed a favorable day of trading last Thursday, with each of the benchmark indexes listed here posting impressive gains, led by the Nasdaq (2.4%), followed by the S&P 500 (2.0%), the Dow (1.6%), the Russell 2000 (1.2%), and the Global Dow (1.0%). All 11 market sectors of the S&P 500 rose, led by communications and consumer discretionary. Strong earnings from big tech companies helped fuel the rally. Ten-year Treasury yields rose 9.6 basis points to 3.52%. Crude oil reversed course, edging up 0.7% to $74.81 per barrel. The dollar was flat, while gold eked out a minimal gain.

Last Friday saw stocks close the session on an upswing. Each of the benchmark indexes listed here posted gains, led by the Russell 2000 (1.0%), followed by the large caps of the Dow and the S&P 500, which rose 0.8%. The Nasdaq climbed 0.7%, while the Global Dow rose 0.5%. Crude oil prices jumped 2.5% to $76.73 per barrel. Gold prices were flat, while the dollar inched higher. The yield on 10-year Treasuries fell 7.6 basis points, ending the session and the week at 3.45%.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The initial estimate of first-quarter gross domestic product showed the economy accelerated at an annualized rate of 1.1%. Compared to the fourth quarter, when the GDP rose 2.6%, the deceleration in the first quarter GDP primarily reflected a downturn in private inventory investment and a slowdown in nonresidential (business) fixed investment. These movements were partly offset by an acceleration in consumer spending, an upturn in exports, and a smaller decrease in residential fixed investment. The Personal Consumption Expenditures Price Index, an indicator of inflation, increased 4.2% in the first quarter, an increase of 0.5 percentage point over the fourth quarter. Excluding food and energy prices, the PCE price index increased 4.9% in the first quarter, compared with an increase of 4.4% in the prior quarter. Personal consumption expenditures increased 3.7% in the first quarter after inching up 1.0% in the fourth quarter.

- Personal income increased in March, while consumer spending saw no change from the prior month. The latest information from the Bureau of Economic Analysis saw personal income climb 0.3% in March, the same increase as in February. Disposable personal income advanced 0.4% (0.5% in February). Personal consumption expenditures were unchanged in March from February. The closely watched Personal Consumption Expenditures Price Index inched up 0.1% in March, following a 0.3% increase in February. Prices excluding food and energy rose 0.3%. Spending on goods declined 0.6%, while services increased 0.4% in March. Over the last 12 months, consumer prices rose 4.2%, down from 5.1% for the 12 months ended in February.

- While sales of existing homes declined in March, sales of new single-family homes advanced for the fifth straight month. March saw sales of new single-family homes increase 9.6% from the previous month. However, sales were 3.4% below their year-earlier total. The median sales price of new houses sold in March 2023 was $449,800. The average sales price was $562,400. Inventory for new single-family homes available for sale in March sat at a 7.6-month supply at the current sales pace, down from 8.4 months in February.

- In March, new orders for durable goods increased 3.2%, following two consecutive monthly decreases. Excluding transportation, new orders advanced 0.3%. Excluding defense, new orders rose 3.5%. Transportation equipment led the overall increase in new orders, climbing 9.1% in March after decreasing in each of the prior two months.

- The advance report on international trade in goods revealed that the trade deficit declined $7.4 billion to $84.6 billion in March. Exports in March were $4.9 billion more than February exports, while imports were $2.5 billion less than February imports. The trade in goods deficit is $40.6 billion less than the March 2022 deficit. Over the last 12 months, exports have risen 2.7%, while imports have fallen 12.3%.

- The national average retail price for regular gasoline was $3.656 per gallon on April 12, $0.007 per gallon less than the prior week’s price and $0.451 less than a year ago. Also, as of April 24, the East Coast price increased $0.031 to $3.543 per gallon; the Gulf Coast price decreased $0.086 to $3.255 per gallon; the Midwest price fell $0.038 to $3.552 per gallon; the Rocky Mountain price increased $0.023 to $3.547 per gallon; and the West Coast price increased $0.023 to $4.548 per gallon.

- For the week ended April 22, there were 230,000 new claims for unemployment insurance, a decrease of 16,000 from the previous week’s level, which was revised up by 1,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended April 15 was 1.3%, unchanged from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended April 15 was 1,858,000, a decrease of 3,000 from the previous week’s level, which was revised down by 4,000. States and territories with the highest insured unemployment rates for the week ended April 8 were California (2.4%), New Jersey (2.4%), Massachusetts (2.1%), Minnesota (2.0%), Rhode Island (1.9%), Illinois (1.8%), New York (1.8%), Alaska (1.7%), Oregon (1.7%), Puerto Rico (1.6%), and Washington (1.6%). The largest increases in initial claims for unemployment insurance for the week ended April 15 were in New York (+6,600), Georgia (+3,245), Connecticut (+1,223), Rhode Island (+1,058), and South Carolina (+688), while the largest decreases were in California (-4,456), Texas (-2,801), Pennsylvania (-1,789), Indiana (-1,516), and Oregon (-1,202).

Eye on the Week Ahead

The Federal Open Market Committee meets this week, where the Committee is likely to announce a 25-basis point interest rate increase. The week closes with the release of the April jobs data. March saw 236,000 new jobs added, while average earnings rose 0.3%.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.