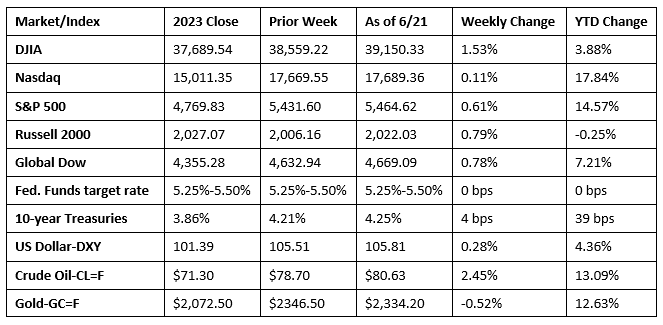

Wall Street rode a rally in tech and AI stocks for most of last week. The end of the week saw a bit of a downturn, but not enough to keep the benchmark indexes listed here from closing the week higher. The large caps of the Dow led the indexes, followed by the Russell 2000, the Global Dow, and the S&P 500. The Nasdaq inched higher. Despite a dip at the end of the week, crude oil prices posted a second straight weekly gain. Ten-year Treasury yields rose higher after positive economic data prompted the Federal Reserve to refrain from cutting interest rates in the third quarter. The market sectors mostly advanced last week, led by consumer discretionary, financials, and communication services. Utilities declined, while information technology ticked lower.

Monday saw megacaps rally, pushing both the S&P 500 and the Nasdaq to new record highs. Each of the benchmark indexes listed here posted gains, led by the Nasdaq, which advanced 1.0%, while the S&P 500 and the Russell 2000 rose 0.8%. The Dow gained 0.5% and the Global Dow climbed 0.4%. Ten-year Treasury yields added 6.6 basis points to close at 4.27%. Crude oil prices broke the $80.00 per barrel mark after gaining $2.17 to reach $80.62 per barrel. The dollar (-0.2%) and gold prices (-0.7%) slid.

Stocks continued to rally last Tuesday as both the S&P 500 and the Nasdaq again reached record highs. The Global Dow (0.6%) led the benchmark indexes listed here followed by the S&P 500 (0.3%). The Dow and the Russell 2000 gained 0.2%, while the Nasdaq eked out a 0.03% advance. The yield on 10-year Treasuries fell 6.2 basis points to 4.21%. Crude oil prices rose to $81.46 per barrel. The dollar slipped 0.1%, while gold prices gained 0.7%.

The stock market was closed last Wednesday for Juneteenth, which gave investors a chance to review and reset. Thursday saw a pullback in tech megacaps, as investors captured recent gains, which led to a decline in the Nasdaq (-0.8%) and the S&P 500 (-0.3%). The small caps of the Russell 2000 also fell, dropping 0.4%. The Dow advanced 0.8% and the Global Dow rose 0.2%. Yields on 10-year Treasuries inched up to 4.25%. Crude oil prices continued to climb higher, gaining nearly 1.0% to $82.34 per barrel. The dollar rose 0.4% and gold prices gained 1.1%.

Stocks declined last Friday to close out the week. The Global Dow fell 0.5%, the Nasdaq and the S&P 500 dipped 0.2%, while the Russell 2000 rose 0.2%. The Dow was essentially flat. Ten-year Treasury yields ended the day where they began. Crude oil prices rose $0.64 to $80.65 per barrel. The dollar inched up 0.2%, while gold prices fell 1.4%.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- Retail sales inched up 0.1% in May and 2.3% above May 2023. Retail trade sales were up 0.2% last month and 2.0% above May 2023. Nonstore retailer sales were up 0.8% in May and 6.8% over the last 12 months. Sales at food services and drinking places fell 0.4% in May but were up 3.8% from May 2023.

- Industrial production rose 0.9% in May. Manufacturing output posted a similar gain of 0.9% last month after declining in each of the previous two months. Mining increased 0.3% in May, and utilities advanced 1.6%. Total industrial production in May was 0.4% higher than its year-earlier level.

- The number of issued residential building permits fell 3.8% in May and 9.5% from a year ago. The number of issued building permits has not increased since February. Building permits for single family homes declined 2.9% last month. Housing starts fell 5.5% last month and 19.4% below the May 2023 estimate. Single-family housing starts in May were 5.2% under the April estimate. Housing completions also declined last month, falling 8.4%. However, residential completions were 1.0% above the May 2023 figure. Single-family housing completions were down 8.5% for the month.

- Sales of existing homes declined 0.7% in May and 2.8% over the last 12 months. Unsold inventory sat at a 3.7-month supply at the current sales pace, up from 3.5 months in April and 3.1 months in May 2023. The median price for existing homes in May was $419,300, the highest price ever recorded and an increase of 3.1% from April ($406,600) and up 5.8% from one year ago ($396,500). According to Freddie Mac, the 30-year fixed-rate mortgage averaged 6.87% as of June 20, down from 6.95% the prior week but up from 6.67% one year ago. Sales of single family homes declined 0.8% from April and 2.1% from the prior year. The median existing single-family home price was $424,500 in May, up from $411,100 in April and well above the May 2023 estimate of $401,500.

- The national average retail price for regular gasoline was $3.435 per gallon on June 17, $0.006 per gallon above the prior week’s price but $0.142 per gallon less than a year ago. Also, as of June 17, the East Coast price fell $0.013 to $3.357 per gallon; the Midwest price increased $0.053 to $3.315 per gallon; the Gulf Coast price rose $0.041 to $2.992 per gallon; the Rocky Mountain price advanced $0.067 to $3.330 per gallon; and the West Coast price declined $0.078 to $4.293 per gallon.

- For the week ended June 15, there were 238,000 new claims for unemployment insurance, a decrease of 5,000 from the previous week’s level, which was revised up by 1,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended June 8 was 1.2%, unchanged from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended June 8 was 1,828,000, an increase of 15,000 from the previous week’s level, which was revised down by 7,000. States and territories with the highest insured unemployment rates for the week ended June 1 were New Jersey (2.3%), California (2.2%), Washington (1.8%), Rhode Island (1.6%), Illinois (1.5%), Massachusetts (1.5%), Minnesota (1.5%), Nevada (1.5%), New York (1.5%), and Pennsylvania (1.5%). The largest increases in initial claims for unemployment insurance for the week ended June 8 were in California (+9,793), Minnesota (+4,397), Pennsylvania (+4,131), Texas (+2,309), and Illinois (+2,265), while the largest decreases were in North Dakota (-746), Missouri (-508), Tennessee (-279), Kansas (-245), and Idaho (-175).

Eye on the Week Ahead

The final and most complete edition of the gross domestic product report for the first quarter is out this week. Thus far, data has shown that the economy accelerated at an annualized rate of 1.3%. Also available this week is the report on personal income and outlays for May. April saw income rose 0.3%, while consumer prices increased 0.3% for the month and 2.7% over the 12 months ended in April.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.