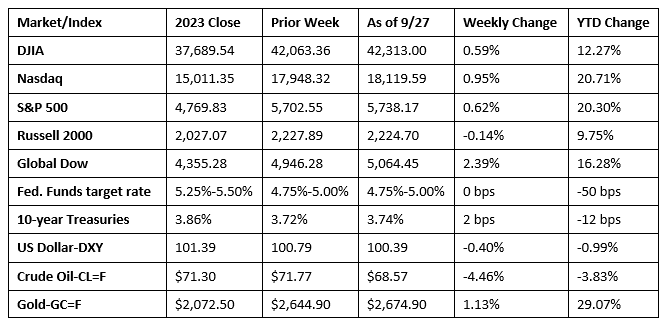

Wall Street enjoyed a solid week of gains following a rough start to the month. Each of the benchmark indexes listed here advanced, with the exception of the Russell 2000, which is generally the most volatile of the aforementioned indexes. Eight of the 11 S&P 500 market sectors closed the week ahead, led by materials and utilities. Only health care, financials, and energy declined. The personal consumption expenditures (PCE) price index, the preferred inflation indicator of the Federal Reserve, inched up 0.1% in August and 2.2% over the last 12 months, nearing the Fed’s 2.0% target. Signs of cooling inflationary pressures likely fueled expectations that the Fed may cut interest rates again this year. Gold prices hit a record high earlier in the week, only to pull back later. Crude oil prices fell below $70.00 per barrel.

Stocks began the last week of September with mixed results. The Global Dow (0.4%) led the benchmark indexes listed here. The S&P 500 (0.3%) and the Dow (0.2%) ticked up higher, but enough to achieve fresh record highs. The NASDAQ ticked up 0.1%. The Russell 2000 (-0.3%) lagged. Ten-year Treasury yields inched up 1.1 basis points to 3.73%. Crude oil prices fell 0.7%, settling at about $70.52 per barrel. The dollar and gold prices posted marginal gains.

The S&P 500 and the Dow hit new records last Tuesday after climbing 0.3% and 0.2%, respectively. The Global Dow (0.8%) gained the most of the remaining benchmark indexes listed here, followed by the NASDAQ (0.6%) and the Russell 2000 (0.2%). Crude oil prices jumped 1.6% to settle at $71.51 per barrel, pushed higher by China’s major economic stimulus measures and escalating tensions in the Middle East. Yields on 10-year Treasuries were unchanged, closing at 3.73%. The dollar fell 0.5%, while gold prices rose 1.4%.

Last Wednesday saw an early-day rally lose steam by the close of trading. Among the benchmark indexes listed here, only the NASDAQ was able to avoid ending the session in the red by less than 0.1%. The remaining indexes declined, with the Russell 2000 falling 1.2%, followed by the Dow (-0.7%), the Global Dow (-0.4%), and the S&P 500 (-0.2%). Bond prices also dipped, sending yields higher, with 10-year Treasuries settling at 3.78%. Crude oil prices slipped just below $70.00 per barrel after declining 2.6%. The dollar (0.5%) and gold prices (0.3%) advanced.

Strong corporate earnings and favorable economic data helped lift stocks higher last Thursday. The Global Dow led the indexes after gaining 1.1%. The NASDAQ, the Dow, and the Russell 2000 each climbed 0.6%. The S&P 500 rose 0.4%, enough to notch another record high. Ten-year Treasury yields ticked up to 3.79%. Crude oil prices decreased for the second straight day, falling 3.2% to $67.47 per barrel. The dollar fell 0.3%, while gold prices advanced 0.4%.

Stocks finished mixed on Friday as investors contemplated how the Federal Reserve would view the latest inflation data. The Russell 2000 gained 0.7%, the Global Dow rose 0.5%, while the Dow reached another record high after increasing 0.3%. The NASDAQ fell 0.4% and the S&P 500 dipped 0.1%. Crude oil prices rebounded after advancing 1.3%. Yields on 10-year Treasuries dipped to 3.74%. The dollar and gold prices declined.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- Gross domestic product (GDP) rose 3.0% in the second quarter, according to the third and final estimate from the Bureau of Economic Analysis. Personal consumption expenditures, the largest contributor to over all GDP, rose 1.90%. Current dollar GDP increased 5.6% in the second quarter. The personal consumption expenditures (PCE) price index increased 2.5% (3.4% in the first quarter). Excluding food and energy prices, the PCE price index increased 2.8% (3.7% in the first quarter).

- Personal income increased $50.5 billion, or 0.2%, in August, according to estimates released today by the U.S. Bureau of Economic Analysis. Disposable personal income, personal income less personal current taxes, increased $34.2 billion, or 0.2%, and personal consumption expenditures (PCE) increased $47.2 billion, or 0.2%. The PCE price index increased 0.1%. Excluding food and energy, the PCE price index also increased 0.1%. Since August 2023, the PCE price index has risen 2.2%, while the PCE price index less food and energy rose 2.7%.

- Sales of new single-family houses in August 2024 were 4.7% below the July rate but 9.8% above the August 2023 estimate. The median sales price of new houses sold in August 2024 was $420,600. The average sales price was $492,700. Inventory of new single-family houses for sale represented a supply of 7.8 months at the current sales rate.

- New orders for manufactured durable goods in August, up six of the last seven months, were unchanged from July, which estimated a 9.9% increase in durable goods orders. Excluding transportation, new orders increased 0.5%. Excluding defense, new orders decreased 0.2%.

- The international trade in goods deficit was $94.3 billion in August, down $8.6 billion from July. Exports of goods for August were $177.0 billion, $4.1 billion more than July exports. Imports of goods for August were $271.3 billion, $4.5 billion less than July imports.

- The national average retail price for regular gasoline was $3.185 per gallon on September 23, $0.005 per gallon above the prior week’s price but $0.652 per gallon less than a year ago. Also, as of September 23, the East Coast price fell $0.033 to $3.052 per gallon; the Midwest price increased $0.072 to $3.077 per gallon; the Gulf Coast price rose $0.005 to $2.733 per gallon; the Rocky Mountain price climbed $0.034 to $3.434 per gallon; and the West Coast price decreased $0.025 to $4.111 per gallon.

- For the week ended September 21, there were 218,000 new claims for unemployment insurance, a decrease of 4,000 from the previous week’s level, which was revised up by 3,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended September 14 was 1.2%, unchanged from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended September 14 was 1,834,000, an increase of 13,000 from the previous week’s level, which was revised down by 8,000. States and territories with the highest insured unemployment rates for the week ended September 7 were New Jersey (2.4%), California (2.0%), Puerto Rico (2.0%), Rhode Island (2.0%), Nevada (1.7%), Washington (1.7%), Massachusetts (1.6%), New York (1.6%), Illinois (1.5%), and Pennsylvania (1.4%). The largest increases in initial claims for unemployment insurance for the week ended September 14 were in Texas (+2,216), New York (+1,842), California (+1,108), Georgia (+1,014), and Michigan (+787), while the largest decreases were in Massachusetts (-1,969), Wisconsin (-794), Connecticut (-569), Nebraska (-517), and Louisiana (-224).

Eye on the Week Ahead

October kicks off with the release of the September employment figures. Job gains have slowed notably over the past few months, which contributed to the cut in interest rates by the Federal Reserve. It appears that the Fed is nearing its goals of maximum employment and 2.0% inflation.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.