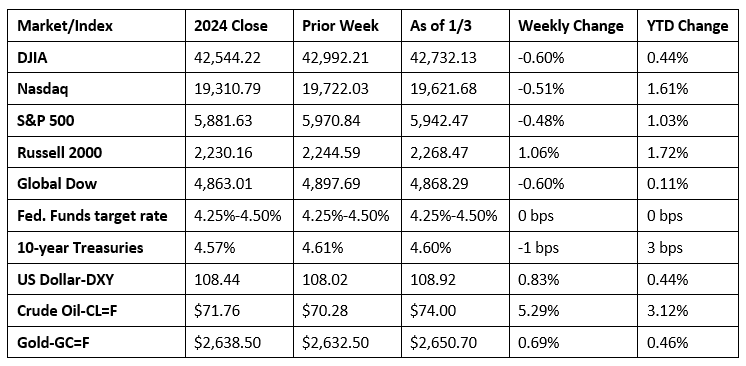

A rise in values last Friday wasn’t enough to prevent stocks from closing generally lower last week. Each of the benchmark indexes declined to start the new year, with the exception of the Russell 2000. Among the market sectors, only energy, utilities, real estate, and health care advanced, while consumer discretionary fell the furthest. Ten-year Treasury yields ended the week where they began. Crude oil prices reached a two-month high, driven by cold weather in Europe and the U.S. coupled with growing optimism over increasing Chinese demand. The dollar remained near its highest levels in two years as investors banked on continuing U.S. economic resilience and fewer interest rate cuts. Gold prices rose following a dip in prices the previous week.

Stocks closed lower for a third straight session last Monday to begin the final trading days of 2024. Tech shares, which had been the bellwether of the market all year, took a tumble, along with consumer staples, consumer discretionary, and communication services. The NASDAQ declined 1.2%, followed by the S&P 500 (-1.1%), the Dow (-1.0%), the Russell 2000 (-0.8%), and the Global Dow (-0.7%). Ten-year Treasury yields fell to 4.54%, a loss of 7.4 basis points. Crude oil prices gained 0.8% to close at $71.14 per barrel. The dollar ticked up 0.1%, while gold prices slid 0.4%.

Wall Street ended December and 2024 on a bit of a sour note. Megacaps declined for the second straight day, pulling stocks lower last Tuesday. The NASDAQ fell 0.9%, the S&P 500 lost 0.4%, and the Dow dipped 0.1%. The Russell 2000 and the Global Dow each edged up 0.1%. Crude oil prices continued to climb higher following news that China’s manufacturing activity grew in December for the third straight month. Yields on 10-year Treasuries ticked up 2.8 basis points to 4.57%. The dollar and gold prices advanced.

The first day of trading in the new year saw stocks get off to a rough start, continuing the slump that marked the end of 2024. Of the benchmark indexes listed here, only the Russell 2000 closed up, and that was by just 0.1%. The Dow fell 0.4%, the Global Dow declined 0.3%, the S&P 500 and the NASDAQ each ended the session down 0.2%. Ten-year Treasury yields remained at 4.57%. Crude oil prices continued to surge, gaining 2.0% to close at $73.12 per barrel. The dollar rose 0.7%, and gold prices advanced 1.1%.

Stocks closed higher last Friday, led by a surge in tech shares. The NASDAQ advanced 1.8% followed by the Russell 2000 (1.7%), the S&P 500 (1.3%), the Dow (0.8%), and the Global Dow (0.4%). Yields on 10-year Treasuries ticked up 0.2 basis points to settle at 4.59%. Crude oil prices rose for the fourth straight session, gaining 1.2%. The dollar and gold prices declined.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- According to the survey of purchasing managers by S&P Global, the manufacturing sector ended 2024 trending lower. After advancing in November, December saw a sharp reduction in new orders, while the rate of decline in production quickened. Business confidence waned and input costs to manufacturers rose sharply, prompting an increase in selling prices. One plus is that employment increased modestly for the second straight month. At 49.4, the S&P Global US Manufacturing Purchasing Managers’ Index™ fell from November’s rate of 49.7, indicating that manufacturing declined.

- The national average retail price for regular gasoline was $3.006 per gallon on December 30, $0.018 per gallon below the prior week’s price and $0.083 per gallon less than a year ago. Also, as of December 30, the East Coast price ticked up $0.011 to $2.956 per gallon; the Midwest price decreased $0.060 to $2.875 per gallon; the Gulf Coast price slid $0.034 to $2.613 per gallon; the Rocky Mountain price fell $0.006 to $2.881 per gallon; and the West Coast price decreased $0.005 to $3.770 per gallon.

- For the week ended December 28, there were 211,000 new claims for unemployment insurance, a decrease of 9,000 from the previous week’s level, which was revised up by 1,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended December 21 was 1.2%, a decrease of 0.1 percentage point from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended December 21 was 1,844,000, a decrease of 52,000 from the previous week’s level, which was revised down by 14,000. States and territories with the highest insured unemployment rates for the week ended December 14 were New Jersey (2.4%), California (2.2%), Minnesota (2.2%), Washington (2.2%), Alaska (2.1%), Rhode Island (2.1%), Illinois (2.0%), Massachusetts (1.9%), Montana (1.8%), Nevada (1.7%), New York (1.7%), and Pennsylvania (1.7%). The largest increases in initial claims for unemployment insurance for the week ended December 21 were in New Jersey (+4,085), Kentucky (+2,135), Missouri (+2,108), Connecticut (+2,088), and Tennessee (+2,018), while the largest decreases were in New York (-965), Florida (-883), West Virginia (-473), Minnesota (-368), and Kansas (-295).

Eye on the Week Ahead

Heading into the new year, all eyes will be on the December employment figures, released at the end of this week. Employment rose by 227,000 in November, although the unemployment rate ticked up 0.1 percentage point to 4.2%. The Federal Reserve pays particular attention to the jobs report as it relates to the Fed’s primary policy goals of full employment and 2.0% inflation. A favorable jobs report supports moderation in the timing of further interest rate reductions.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.