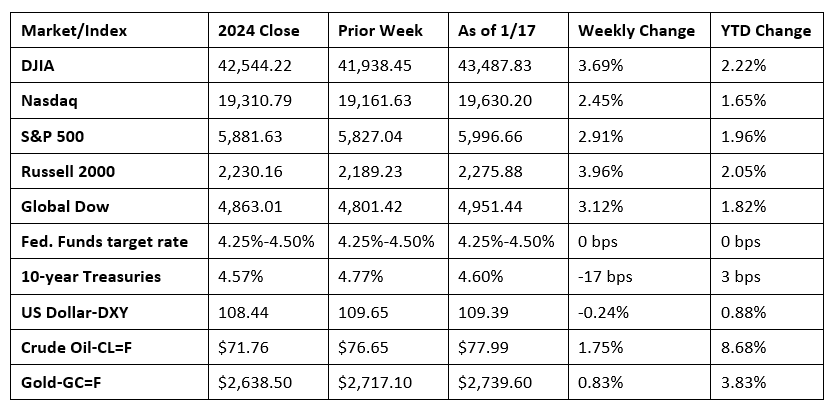

Stocks closed higher last week, despite a few shaky days. Each of the benchmark indexes listed here posted gains, led by the Russell 2000 and the Dow. Consumer discretionary stocks outperformed along with energy, financials, materials, and industrials. Investor sentiment improved following favorable inflation data and solid earnings from major banks. Crude oil prices increased for the fourth straight week, primarily driven by concerns of new U.S. sanctions against Russian oil producers, which raised worries of tighter global oil supplies. The dollar index declined, snapping a six-week rally.

The week kicked off with stocks closing mostly higher with the exception of tech shares, which lagged. The Dow led the benchmark indexes listed here, gaining 0.9% followed by the Global Dow (0.3%), the S&P 500 (0.2%), and the Russell 2000 (0.1%). The NASDAQ edged down 0.4%. The yield on 10-year Treasuries reached its highest level since late 2023, settling at 4.80%. Crude oil prices continued the prior week’s surge, climbing to $78.71 per barrel, the highest rate in more than four months. The dollar inched up 0.2%, while gold prices fell 1.3%.

Stocks closed last Tuesday mixed, with the Russell 2000 (1.1%), the Global Dow (0.5%), and the Dow (0.5%) leading the benchmark indexes listed herek while the S&P 500 edged up 0.1%. The NASDAQ fell 0.2% as some megacaps declined. Ten-year Treasury yields slid to 4.78%. Crude oil prices declined 1.3% to $77.76 per barrel. The dollar dropped 0.7%, while gold prices rose 0.4%.

Wall Street enjoyed the biggest daily gains in over two months last Wednesday on the heels of strong bank earnings and moderating core inflation growth (see below). The NASDAQ, which had been floundering, gained 2.5%. The Russell 2000 followed a solid performance the previous day by gaining 2.0% on Wednesday. The S&P 500 added 1.8%. The Dow rose 1.7%, and the Global Dow gained 1.4%. With rising stock values, bond prices also advanced, pulling yields lower. Ten-year Treasury yields fell 13.5 basis points to 4.65%. Crude oil prices climbed to $80.48 per barrel, the highest price since August. The dollar ticked lower, while gold prices rose 1.4%.

Stocks closed mostly lower last Thursday. Shares of big tech companies receded, dragging the market lower. The NASDAQ fell 0.9%. The S&P 500 saw its three-day rally end after declining 0.2%. The Dow slid 0.2%. The Global Dow (0.4%) and the Russell 2000 (0.2%) moved higher. Ten-year Treasury yields continued their two-day slide, falling to 4.60%. Crude oil prices fell 1.6%, settling at $78.77 per barrel. The dollar slipped 0.1%, while gold prices gained 1.1%.

Tech shares rebounded at the end of the week, helping to push most stocks higher last Friday. The NASDAQ gained 1.5%, followed by the S&P 500 (1.0%), the Dow (0.8%), the Global Dow (0.6%), and the Russell 2000 (0.4%). Ten-year Treasury yields were flat. Crude oil prices fell for the second straight day, declining 0.8%. The dollar gained 0.4%, while gold prices dipped 0.5%.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The Consumer Price Index (CPI) increased 0.4% in December, in line with expectations but up from a 0.3% advance in November. Energy prices rose 2.6% last month, accounting for over 40% of the overall increase in the CPI. Food prices also increased in December, rising 0.3%. Prices less food and energy rose 0.2% in December, down from November’s 0.3% increase. Price indexes that increased in December include shelter, airline fares, used cars and trucks, new vehicles, motor vehicle insurance, and medical care. The indexes for personal care, communication, and alcoholic beverages were among the few major indexes that decreased over the month. The CPI rose 2.9% over the 12 months ended in December after increasing 2.7% over the 12 months ended in November. Prices less food and energy rose 3.2% over the last 12 months. Energy prices decreased 0.5% for the 12 months ended in December. Food prices increased 2.5% over the last year.

- Prices at the producer level rose a less-than-expected 0.2% in December. Producer prices rose 0.4% in November. Producer prices rose 3.3% in 2024 after increasing 1.1% in 2023. The December increase was attributed to a 0.6% jump in prices for goods. Prices for services were unchanged after rising 0.3% in November. Last month, energy prices increased 3.5%, while prices for foods ticked down 0.1%.

- Retail sales rose 0.4% in December and were up 3.9% since December 2023. Year to date, retail sales were up 3.0%. Retail trade sales were up 0.6% in December and rose 4.2% from last year. Motor vehicle and parts dealers sales were up 8.4% over the last 12 months, while nonstore (online) retailer sales were up 6.0% from December 2023.

- Import prices ticked up 0.1% in December for the third straight month. Import prices advanced 2.2% over the past 12 months, the largest 12-month increase since the period ended December 2022. Import fuel rose 1.4% in December, the largest monthly advance since the index increased 3.9% in April 2024. Import fuel prices rose 0.3% over the past 12 months, the first yearly increase since the 12-month period ended July 2024. Import prices excluding fuel inched up 0.1% last month and have not decreased on a monthly basis since May 2024.

- Industrial production (IP) increased 0.9% in December after moving up 0.2% in November. In December, gains in the output of aircraft and parts contributed 0.2 percentage point to overall IP growth following the resolution of a work stoppage at a major aircraft manufacturer. Manufacturing output rose 0.6% after gaining 0.4% in November. The indexes for mining and utilities climbed 1.8% and 2.1%, respectively, in December. From December 2023, industrial production was 0.5% above its year-earlier level.

- The U.S. Treasury budget deficit was $86.7 billion in December, well below the November deficit of $366.8 billion and under the December 2023 deficit of $129.4 billion. Last month, government receipts were $454.4 billion of which $212.0 billion was attributable to individual income taxes. December outlays totaled $541.1 billion with the biggest contributor being Social Security payments ($124.0 billion). For the fiscal year, which began in October, the deficit was $710.9 billion, about $200.0 billion above the deficit over the comparable period last fiscal year.

- The housing sector saw a dip in new home construction in December. The number of issued building permits fell 0.7% for the month and was 3.1% below the December 2023 rate. However, building permits for single-family homes increased 1.6% in December. For 2024, the number of issued building permits were 2.6% below the 2023 figure. Housing starts rose 15.8% last month but were 4.4% under the December 2023 figure. Housing starts for single-family homes ended December 3.3% over the November rate. For the year, housing starts were 3.9% below the prior year’s total. Housing completions declined 4.8% in December and 0.8% under the December 2023 total. The number of single-family home completions was 7.4% below the November rate. In 2024, total home completions were 12.4% above the 2023 pace.

- The national average retail price for regular gasoline was $3.043 per gallon on January 13, $0.004 per gallon below the prior week’s price and $0.015 per gallon less than a year ago. Also, as of January 13, the East Coast price climbed $0.008 to $2.998 per gallon; the Midwest price decreased $0.039 to $2.899 per gallon; the Gulf Coast price rose $0.010 to $2.665 per gallon; the Rocky Mountain price fell $0.020 to $2.879 per gallon; and the West Coast price increased $0.017 to $3.810 per gallon.

- For the week ended January 11, there were 217,000 new claims for unemployment insurance, an increase of 14,000 from the previous week’s level, which was revised up by 2,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended January 4 was 1.2%. The advance number of those receiving unemployment insurance benefits during the week ended January 4 was 1,859,000, a decrease of 18,000 from the previous week’s level, which was revised up by 10,000. States and territories with the highest insured unemployment rates for the week ended December 28 were New Jersey (2.9%), Rhode Island (2.9%), Minnesota (2.8%), Washington (2.5%), Massachusetts (2.3%), California (2.2%), Connecticut (2.2%), Illinois (2.2%), Alaska (2.1%), Montana (2.1%), and Pennsylvania (2.1%). The largest increases in initial claims for unemployment insurance for the week ended January 4 were in New York (+22,233), Georgia (+7,636), Texas (+5,812), South Carolina (+2,844), and Oregon (+2,567), while the largest decreases were in Michigan (-7,040), New Jersey (-4,683), Massachusetts (-4,201), Connecticut (-3,749), and Iowa (-3,555).

Eye on the Week Ahead

The holiday-shortened week includes one economic report of note: the December data on sales of existing homes. November saw sales increase 4.8% for the month and 2.6% over the last 12 months.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.