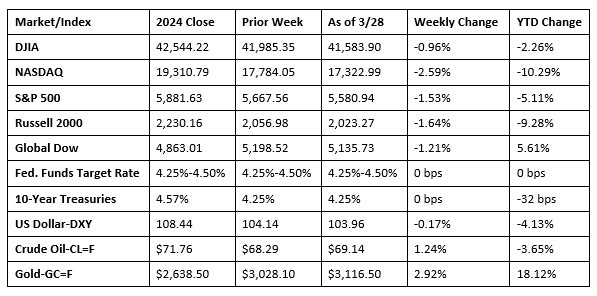

Despite getting off to a good start, stocks wavered throughout much of last week, ultimately closing lower. Each of the benchmark indexes lost ground, with the S&P 500 finishing the week lower for the fifth time in the last six weeks after reaching record highs in mid-February. Several negative factors weighed on investors, including hotter-than-expected core consumer prices (see below) and a slowdown in consumer spending. Last Monday saw stocks rise as investors were encouraged by the prospect of the Trump administration selectively imposing tariffs, reducing the likelihood of a full-blown trade war. Both the S&P 500 and the NASDAQ gained again last Tuesday, marking their third consecutive sessions of gains. A tech stock selloff, coupled with mounting tariff concerns, led to a sharp fall in stocks last Wednesday. Crude oil prices rose to $69.90 per barrel, the highest in nearly four weeks, as concerns over tightening global supply drove prices up. Stocks continued to trend lower last Thursday after President Trump announced new tariffs on foreign-made autos, raising concerns of a potential trade war and its broader impact on the global economy. The week ended with equities closing lower, dampened by growing concerns over rising inflation and trade wars. Among the market sectors, only consumer discretionary, consumer staples, and energy closed higher, with information technology dropping 2.1%. Bond yields ended the week where they began. Gold prices ended the week at a record high. The dollar index ended the week lower after reaching a three-week high earlier in the week.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- Gross domestic product (GDP) increased at an annual rate of 2.4% in the fourth quarter of 2024, according to the third and final estimate released by the U.S. Bureau of Economic Analysis. In the third quarter, GDP increased 3.1%. The increase in GDP in the fourth quarter primarily reflected increases in consumer spending and government spending that were partly offset by a decrease in investment. Imports, which are a subtraction in the calculation of GDP, decreased. Compared to the third quarter, the decrease in GDP was primarily attributable to downturns in investment and exports, while consumer spending increased from 3.7% in the third quarter to 4.0% in the fourth quarter. For 2024, GDP rose 2.8% from 2023.

- According to the latest information from the Bureau of Economic Analysis, personal income increased 0.8% in February. Disposable personal income (less personal income taxes) rose 0.9% last month. Personal consumption expenditures (PCE), a measure of consumer spending, increased 0.4%. The PCE price index, a preferred measure of inflation for the Federal Reserve, increased 0.3% in February. Excluding food and energy, the PCE price index increased 0.4%. Over the last 12 months, the PCE price index increased 2.5%. Excluding food and energy, the PCE price index rose 2.8% over the past 12 months.

- Sales of new single-family houses in February were 1.8% above the revised January rate and were 5.1% higher than the February 2024 estimate. The median sales price of new houses sold in February was $414,500. The average sales price was $487,100. The estimate of new houses for sale at the end of February represented a supply of 8.9 months at the current sales rate.

- New orders for manufactured durable goods in February, up two consecutive months, increased 0.9%, according to the U.S. Census Bureau. The February increase followed a 3.3% January advance. Excluding transportation, new orders increased 0.7% last month. Excluding defense, new orders increased 0.8%. Transportation equipment, also up two consecutive months, led the increase after rising 1.5%.

- The international trade in goods deficit was $147.9 billion in February, down $7.7 billion, or 4.9%, from January. Exports of goods for February were $178.6 billion, $7.0 billion, or 4.1%, more than January exports. Imports of goods for February were $326.5 billion, $0.6 billion, or 0.2%, less than January imports.

- The national average retail price for regular gasoline was $3.115 per gallon on March 24, $0.057 per gallon above the prior week’s price but $0.408 per gallon less than a year ago. Also, as of March 24, the East Coast price ticked up $0.012 to $2.961 per gallon; the Midwest price increased $0.126 to $3.020 per gallon; the Gulf Coast price advanced $0.111 to $2.740 per gallon; the Rocky Mountain price increased $0.045 to $3.043 per gallon; and the West Coast price dipped $0.006 to $4.055 per gallon.

- For the week ended March 22, there were 224,000 new claims for unemployment insurance, a decrease of 1,000 from the previous week’s level, which was revised up by 2,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended March 15 was 1.2%. The advance number of those receiving unemployment insurance benefits during the week ended March 15 was 1,856,000, a decrease of 25,000 from the previous week’s level, which was revised down by 11,000. States and territories with the highest insured unemployment rates for the week ended March 8 were Rhode Island (2.9%), New Jersey (2.8%), California (2.4%), Massachusetts (2.4%), Minnesota (2.4%), Illinois (2.3%), Washington (2.3%), Montana (2.1%), District of Columbia (2.0%), Connecticut (1.9%), New York (1.9%), and Pennsylvania (1.9%). The largest increases in initial claims for unemployment insurance for the week ended March 15 were in Michigan (+2,842), Mississippi (+1,775), Texas (+1,458), Nebraska (+395), and Missouri (+206), while the largest decreases were in California (-3,625), Illinois (-1,365), Virginia (-895), Pennsylvania (-877), and New Jersey (-860).

Eye on the Week Ahead

The employment figures for March are out this week. February saw jobs increase by 151,000, while the unemployment rate ticked up to 4.1%.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.