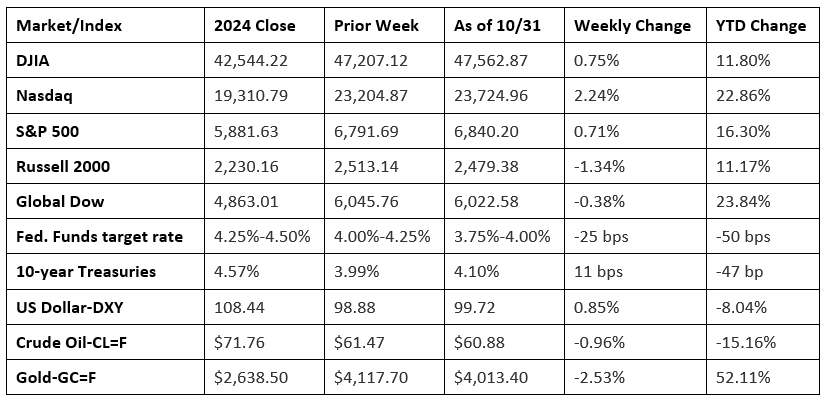

Stocks moved generally higher last week, largely driven by solid corporate earnings from some big tech firms. The S&P 500 and the NASDAQ each reached record highs during the week, extending a significant rally. The push higher was moderated somewhat by the Federal Reserve’s cautious stance on future rate cuts. Despite a lack of updated economic information, the Fed identified concerns about the potential for a weakening job market and stubbornly elevated inflation rates. While trade tensions between the U.S. and China were tempered following a meeting between President Trump and Chinese leader Xi Jinping, analysts cautioned that underlying issues still had not been resolved. Following last week’s interest rate cut, U.S. Treasury yields rose sharply, extending a three-session rally that pushed the 10-year Treasury yield to a three-week high. Despite an early-week rally, crude oil prices dipped lower last week, primarily due to concerns of global oversupply and increased production.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The release of most economic data has been delayed due to the government shutdown.

- The Federal Open Market Committee lowered the federal funds rate by 25 basis points to 3.75%-4.00% following its meeting last week. This marks the lowest range for the federal funds rate since 2022. The decision was based on a 10-2 vote, with Stephen I. Miran preferring to lower the target range for the federal funds rate by 50 basis points, while Jeffrey R. Schmid voted for no change to the target range for the federal funds rate. In seeking to achieve its mandate of maximum employment and inflation at 2.0% over the longer run, the Committee based its rate cut on rising downside risks to employment and elevated inflation.

- The federal government enjoyed a surplus of $198 billion in September, the last month of fiscal year 2025. Government receipts were $544 billion, while expenditures totaled $346 billion. For fiscal year 2025, total receipts were $5,235 billion, while outlays were $7,010 billion, leaving a deficit of $1,775 billion, which was less than the FY2024 deficit of $1,817 billion.

- The national average retail price for regular gasoline was $3.035 per gallon on October 27, $0.016 per gallon above the prior week’s price but $0.062 per gallon less than a year ago. Also, as of October 27, the East Coast price increased $0.008 to $2.910 per gallon; the Midwest price rose $0.068 to $2.873 per gallon; the Gulf Coast price climbed $0.024 to $2.580 per gallon; the Rocky Mountain price dropped $0.025 to $2.972 per gallon; and the West Coast price dipped $0.060 to $4.106 per gallon.

Eye on the Week Ahead

There will be little relevant economic data available during the government shutdown.

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2025 Broadridge Financial Solutions, Inc. All Rights Reserved.