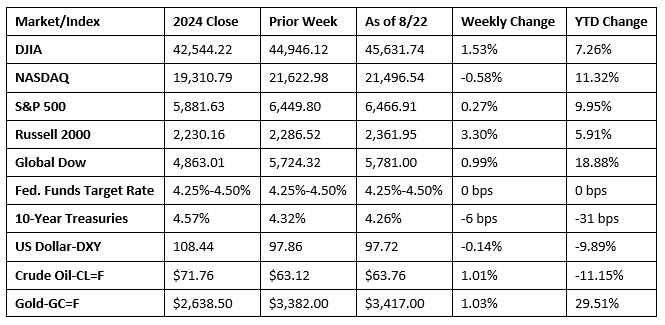

Last week was a volatile one for stocks, largely in response to mixed economic data, corporate earnings reports, and the anticipation of a key speech from Federal Reserve Chair Jerome Powell at the end of the week. The benchmark indexes listed here ebbed and flowed for much of the week until last Friday, when equities surged after Powell hinted at a likely interest rate cut in September. The S&P 500, the Russell 2000, and the Global Dow each posted weekly gains, with the Dow reaching a record high last Friday. The NASDAQ ended the week in the red despite an end-of-week rally. Treasury yields edged higher earlier in the week, but the prospects of an interest rate cut pulled yields lower by week’s end. Crude oil prices posted their first weekly gain after falling in each of the past two weeks.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The number of issued residential building permits fell 2.8% in July and was down 5.7% from July 2024. The number of single-family building permits in July was 0.5% above the June estimate. Housing starts in July were 5.2% above the revised June estimate and 12.9% higher than the July 2024 rate. Single-family housing starts in July were 2.8% above the revised June estimate. The number of housing completions in July was 6.0% above the revised June estimate but was 13.5% below the July 2024 rate. Single-family housing completions in July were 11.6% above the revised June figure.

- Sales of existing homes rose 2.0% in July, reflecting a slight improvement in housing affordability. Existing home sales were up 0.8% from July 2024. Inventory of existing homes ticked down from a supply of 4.7 months in June to 4.6 months last month. The median existing-home price was $422,400 in July, down from $432,700 in June but 0.2% above the July 2024 estimate of $421,400. Sales of existing single-family homes also rose 2.0% in July and were up 1.1% over the last 12 months. The median existing single-family home price was $428,500 in July, lower than the June estimate of $438,600 but higher than the July 2024 figure of $427,200. Inventory of existing single-family homes in July sat at a 4.5-month supply.

- The national average retail price for regular gasoline was $3.125 per gallon on August 18, $0.007 per gallon above the prior week’s price but $0.257 per gallon less than a year ago. Also, as of August 18, the East Coast price decreased $0.008 to $2.997 per gallon; the Midwest price fell $0.003 to $2.994 per gallon; the Gulf Coast price rose $0.065 to $2.745 per gallon; the Rocky Mountain price increased $0.005 to $3.164 per gallon; and the West Coast price rose $0.012 to $4.044 per gallon.

- For the week ended August 16, there were 235,000 new claims for unemployment insurance, an increase of 11,000 from the previous week’s level. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended August 9 was 1.3%, unchanged from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended August 9 was 1,972,000, an increase of 30,000 from the previous week’s level, which was revised down by 11,000. This was the highest level for insured unemployment since November 6, 2021, when it was 2,041,000. States and territories with the highest insured unemployment rates for the week ended August 2 were New Jersey (2.7%), Puerto Rico (2.6%), Rhode Island (2.5%), Minnesota (2.2%), California (2.1%), the District of Columbia (2.1%), Massachusetts (2.1%), Washington (2.1%), Oregon (1.9%), and Pennsylvania (1.9%). The largest increases in initial claims for unemployment insurance for the week ended August 9 were in California (+741), New York (+630), Rhode Island (+570), Michigan (+527), and Maryland (+343), while the largest decreases were in Iowa (-704), Illinois (-334), New Jersey (-251), Pennsylvania (-158), and Oregon (-153).

Eye on the Week Ahead

This week reveals the second iteration of gross domestic product for the second quarter. The initial estimate of GDP had the economy growing at a rate of 3.0%. Also out this week is the July report on personal income and expenditures. Included in that report are the estimates of consumer spending and prices for consumer goods, the Federal Reserve’s preferred measure of inflation.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2025 Broadridge Financial Solutions, Inc. All Rights Reserved.