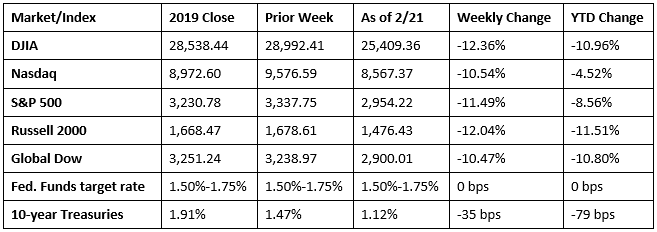

Panicked investors continued a major sell-off last week, pushing stocks to double-digit losses. Fears of a major global economic impact increased as the coronavirus continued to spread across multiple countries. By the end of last week, each of the major benchmark indexes listed here fell by more than 10%, headed by the Dow, which lost close to 12.5%. Following the Dow were the small caps of the Russell 2000, the S&P 500, the Nasdaq, and the Global Dow. Money flowed from stocks and into long-term bonds. The yield on 10-year Treasuries plummeted 35 basis points to 1.12% as bond prices soared. The price of oil was also hit hard, falling more than $8 per barrel by the end of last week.

Oil prices plunged last week, closing at $45.19 per barrel by late Friday afternoon, down from the prior week’s price of $53.35. The price of gold (COMEX) fell back last week, closing at $1,585.80 by late Friday afternoon, down from the prior week’s price of $1,646.10. The national average retail regular gasoline price was $2.466 per gallon on February 24, 2020, $0.038 higher than the prior week’s price and $0.076 more than a year ago.

Last Week’s Economic News

- There was no change in the growth of the economy in the fourth quarter as the second estimate mirrored the first, with the economy expanding at an annual rate of 2.1%. The third-quarter GDP also advanced 2.1%. The price index for gross domestic purchases increased 1.4% in the fourth quarter, the same increase as in the third quarter. The personal consumption price index increased 1.3%, compared with a third-quarter increase of 1.5%. Excluding food and energy prices, the PCE price index increased 1.2%, compared with an increase of 2.1% in the prior quarter.

- Inflationary pressures remained muted in January as prices for consumer goods and services inched up 0.1%. Over the last 12 months, the personal consumption price index is up 1.7%, well below the Fed’s target of 2.0%. Prices less food and energy also rose 0.1% in January and 1.6% for the year. Personal income advanced 0.6% in January (after-tax personal income also advanced 0.6%) and consumer spending climbed 0.2% for the month.

- Manufacturing continues to slide, down two of the last three months. New orders for durable goods fell 0.2% in January and are- rf down 2.2% over the last 12 months. Excluding transportation, new orders increased 0.9%. Excluding defense, new orders increased 3.6%. Transportation equipment, down four of the last five months, drove the decrease, falling 2.2%. Shipments of manufactured durable goods in January, down seven consecutive months, decreased 0.2%. On the plus side of this latest report, new orders for nondefense capital goods in January increased 12.4%. Capital goods are tangible assets produced by one manufacturer and used by another manufacturer or business to produce consumer goods.

- While sales of existing homes may have fallen in January, the same didn’t hold true for new home sales. According to the Census Bureau, sales of new single-family homes were 7.9% above the December rate and 18.6% higher than January 2019. The median sales price of new houses sold in January 2020 was $348,200, and the average sales price was $402,300 — both of which were higher than December’s respective sales prices. The estimate of new houses for sale at the end of January was 324,000, which represents a supply of 5.1 months at the current sales rate.

- The international trade in goods deficit was a little smaller in January compared to the prior month. At $65.5 billion, the deficit was $3.2 billion below December’s deficit figure. Exports were $1.4 billion less than December’s exports. Imports were $4.6 billion less than December’s imports.

- For the week ended February 22, there were 219,000 claims for unemployment insurance, an increase of 8,000 from the previous week’s level, which was revised up by 1,000. According to the Department of Labor, the advance rate for insured unemployment claims remained at 1.2% for the week ended February 15. The advance number of those receiving unemployment insurance benefits during the week ended February 15 was 1,724,000, a decrease of 9,000 from the prior week’s level, which was revised up by 7,000.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Eye on the Week Ahead

Reports on the manufacturing sector kick off the week. Purchasing managers reported some growth in new orders and production in January, but manufacturing has been generally weak for quite some time. On the other hand, employment has been solid with 225,000 new jobs added in January. It will be hard to top that total in February. Average weekly wages grew 3.1% over the 12 months ended in January. Investors will no doubt be watching the coronavirus to see if it continues to spread and its effect on global supply chains.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.