In observance of Good Friday, the stock market closed for business at the final bell last Thursday. The week started out with a bang as stocks soared in value on Monday with each of the benchmark indexes posting sizable gains. Investors were buoyed by the latest data, which showed that the spread of COVID-19 may be slowing in New York, the epicenter of the pandemic in the United States. The Dow, S&P 500, and Nasdaq enjoyed the largest single-day gains since March 24. Unfortunately, the gains were given back on Tuesday as investors wondered whether the virus was actually slowing. Oil prices sank and bond prices dropped, pushing yields higher.

Stocks soared midweek on word late Wednesday afternoon that the federal government was considering easing the containment restrictions put in place to fight the spread of COVID-19. The official end of the presidential bid by Bernie Sanders who pledged to tighten restrictions on Wall Street and big corporations, also may have played a part in the market surge. By the close of the day, the Dow and S&P 500 had gained nearly 3.5%, the Nasdaq had climbed about 2.6%, and the small caps of the Russell 2000, which had been hit particularly hard of late, had vaulted ahead by more than 4.6%.

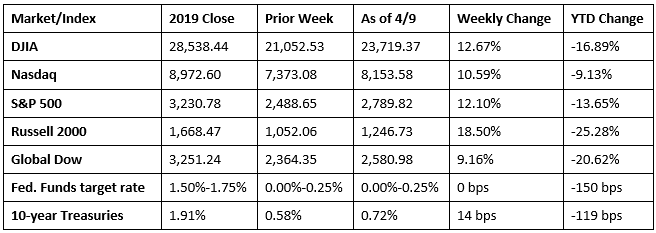

Stocks closed the holiday-shortened week ahead for a change. Thursday’s trading resulted in further gains on the news that the Federal Reserve would release $2.3 trillion in funds through its lending programs to states, cities, and midsized businesses. The Fed also said it would support riskier corporate bonds. Investors were also encouraged by the proposed agreement by major oil exporters to cut production. Each of the benchmark indexes listed here posted solid weekly gains, led by the Russell 2000, which climbed more than 18.0%. The remaining indexes all boasted gains of more than 10.0%. While the upswing in market returns is encouraging, economic indicators are not so positive. Another 6 million claims for unemployment insurance were filed, and oil prices, despite the potential rollback in production, remain muted.

Despite news that some major oil-producing nations may be nearing an agreement to cut production, prices fell last week, closing at $23.19 per barrel by late Thursday afternoon, down from the prior week’s price of $28.79. The price of gold (COMEX) continued to climb last week, closing at $1,715.40 by late Thursday afternoon, up from the prior week’s price of $1,649.30. The national average retail regular gasoline price was $1.924 per gallon on April 6, 2020, $0.081 lower than the prior week’s price and $0.821 less than a year ago.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- Consumer prices fell 0.4% in March, the largest monthly decline since January 2015. Over the last 12 months ended in March, consumer prices have increased a scant 1.5%. Once again, falling gasoline prices dragged the overall Consumer Price Index down. Last month, gas prices dropped 10.5%, while overall energy prices sank 5.8%. Consumer prices less food and energy fell 0.1% in March, the first such decrease since January 2010. Prices for airline fares, lodging, apparel, and new vehicles all decreased in March.

- The prices producers receive for goods and services fell 0.2% in March after dropping 0.6% in February. For the last 12 months ended in March, producer prices have inched up 0.7%. Goods prices at the producer level decreased 1.0% last month, the largest decline since moving down 1.1% in September 2015. The primary factor in pushing goods prices lower was a 6.7% decrease in energy prices, particularly gasoline prices, which fell 16.8%. Prices for services actually rose 0.2% in March after falling 0.3% the previous month.

- The total number of job openings fell slightly in February, according to the latest Job Openings and Labor Turnover report. There were 6.882 million job openings in February, down from January’s total of 7.012 million. Both total hires and separations also dropped in February from the previous month. In February, job openings decreased in real estate and rental and leasing (-30,000) and information (-29,000). Durable goods manufacturing saw a notable uptick in hires. Over the 12 months ended in February, hires totaled 70.3 million and separations totaled 67.9 million, yielding a net employment gain of 2.4 million.

- The federal government deficit for March was $119.1 billion. Year to date, the deficit sits at $743.6 billion — 7.6% higher than the deficit over the same period last fiscal year.

- COVID-19 continues to impact the number of initial claims for unemployment insurance. For the week ended April 4, there were 6,606,000, a decrease of 261,000 from the previous week’s level, which was revised up by 219,000. According to the Department of Labor, the advance rate for insured unemployment claims jumped from 2.1% for the week ended March 21 to 5.1% for the week ended March 28. The advance number of those receiving unemployment insurance benefits during the week ended March 28 was 7,455,000, an increase of 4,396,000 from the prior week’s level, which was revised up by 30,000. This marks the highest level of insured unemployment in the history of the series. The previous high was 6,635,000 in May 2009.

Eye on the Week Ahead

The March figures on industrial production, released by the Federal Reserve, are out this week. According to the surveys of purchasing managers, manufacturing output is expected to drop notably. The report on housing starts is also available this week. Lower interest rates could be an incentive for shoppers looking for newly constructed homes, but with so many people out of work, home builders may see a drop in ready buyers.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.