Last week started out poorly for equities as investors saw the faint hope of pre-election financial stimulus fade. The major indexes fell to their lowest levels in nearly two weeks by the close of trading last Monday. The Nasdaq and S&P 500 each dropped 1.6%, respectively. The Dow fell 1.4%, the Russell 2000 dipped 1.2%, and the Global Dow lost 0.4%. Treasury bond prices fell, driving yields higher. Crude oil prices and the dollar also lost value. All of the major market sectors closed in the red with energy, information technology, financials, real estate, and health care each falling by at least 1.5%.

Equities rebounded last Tuesday. Investors may have been looking to scoop up some discounted stocks or were encouraged by a glimmer of hope for fiscal stimulus before the election. In any case, each of the benchmarks posted moderate gains, led by the S&P 500 (0.5%), followed by the Dow (0.4%), the Global Dow (0.4%), the Nasdaq (0.3%), and the Russell 2000 (0.3%). Treasury yields and crude oil prices rose while the dollar fell. Among the major market sectors, energy, communication services, consumer discretionary, financials, and real estate were solid. COVID-19 news was mixed with the number of confirmed cases rising, countered by encouraging vaccine reports.

The prior day’s market rebound was short lived as stocks fell last Wednesday. While Democrats and the White House seemed to near a fiscal stimulus package, it does not appear that anything will happen before the November election. The major market indexes ended a volatile day finishing lower, led by the Russell 2000 (-0.9%), followed by the Dow (-0.4%), the Nasdaq (-0.3%), the S&P 500 (-0.2%), and the Global Dow (-0.2%). Most of the major market sectors fell, with energy dropping nearly 2.0%. Crude oil and the dollar lost value while Treasury yields rose.

Investors continue to be influenced by reports emanating from the ongoing negotiations over additional virus-related fiscal stimulus. This time, it was House Speaker Nancy Pelosi who told reporters last Thursday that a deal is “just about there.” That encouraging piece of news was enough to send stocks higher, with each of the benchmark indexes listed posting gains. Treasury yields also rose as bond prices slipped. Crude oil prices jumped 1.6%, and the dollar gained against a basket of currencies. Energy, financials, utilities, and health care gained on the day, while tech stocks fell.

Stocks were mixed by the close of trading last Friday. Poor performance from energy and technology offset strength in financials, materials, health care, and consumer discretionary. The Dow fell 0.1%, while the remaining benchmark indexes gained value, led by the Russell 2000 (0.6%), followed by the Global Dow (0.6%), the Nasdaq (0.4%), and the S&P 500 (0.3%). Treasury yields fell, pulled down by rising bond prices. Crude oil prices dropped 2.2% on the day, and the dollar fell. Investors were apparently unaffected by a lack of movement on the fiscal stimulus talks and last Thursday nights presidential debate.

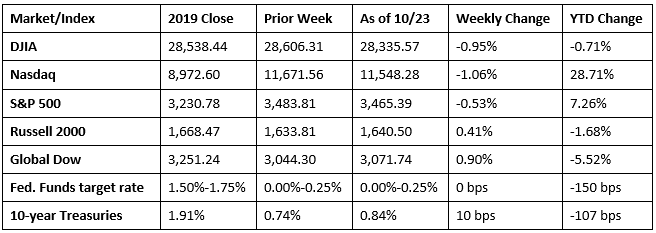

Stimulus rhetoric aside, earnings reporting season is in full force and the results have been mixed, which certainly impacted stock values. For the week, the major indexes were mixed with the Global Dow and the Russell 2000 posting moderate gains, while the Dow, the Nasdaq, and the S&P 500 lost value. Year to date, the Dow fell below its 2019 closing value leaving only the Nasdaq and the S&P 500 ahead of their respective year-end marks.

Crude oil prices fell last week, closing at $39.75 per barrel by late Friday afternoon, down from the prior week’s price of $40.75 per barrel. The price of gold (COMEX) closed the week at $1,904.90, up from the prior week’s price of $1,901.90. The national average retail price for regular gasoline was $2.150 per gallon on October 19, $0.017 lower than the prior week’s price and $0.488 less than a year ago.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The housing sector continued its strong showing in September. According to the Census Bureau, building permits were 5.2% above their August rate and 8.1% higher than September 2019. Housing starts last month were 1.9% above August and 11.1% more than last September. Housing completions soared in September, vaulting 15.3% over their August totals and 25.8% over September 2019. Low interest rates have helped drive new home construction and add to the number of new homes available for sale.

- Existing home sales grew for the fourth consecutive month in September. According to the National Association of Realtors®, sales of existing homes were 9.4% above the August rate and 20.9% ahead of September 2019. The median existing-home price for all housing types in September was $311,800, 0.4% higher than the August price of $310,600, and 14.8% above the September 2019 price ($271,500). Inventory of existing homes for sale fell 1.3% in September from the prior month. Unsold inventory sits at a 2.7-month supply. Sales of single-family homes also advanced last month, outpacing the August rate by 9.7%. Single-family home sales were up 21.8% over the last 12 months. The median existing single-family home price was $316,200 in September, up 0.4% ahead of the August price of $315,000, and 15.2% higher than the price in September 2019.

- For the week ended October 17, there were 787,000 new claims for unemployment insurance, a decrease of 55,000 from the previous week’s level, which was revised down by 56,000. According to the Department of Labor, the advance rate for insured unemployment claims was 5.7% for the week ended October 10, a decrease of 0.7 percentage point from the prior week’s rate, which was revised down by 0.4 percentage point. The advance number of those receiving unemployment insurance benefits during the week ended October 10 was 8,373,000, a decrease of 1,024,000 from the prior week’s level, which was revised down by 621,000. For perspective, a year ago there were 213,000 initial claims for unemployment insurance, the rate for insured unemployment claims was 1.2%, and 1,691,000 people were receiving unemployment insurance benefits.

Eye on the Week Ahead

The last week of October brings with it plenty of important economic reports that can move the market. The first estimate of the third-quarter gross domestic product is available. The economy contracted at an annual rate of 31.4% in the second quarter, largely due to the impact of COVID-19. At the end of this week, the latest information on personal income, expenditures and consumer prices for September is released. Personal income dropped 2.7% in August, while prices for consumer goods and services inched up only 0.3%.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.