Stocks rebounded last Monday with each of the benchmark indexes gaining value, led by the Russell 2000, which added 2.0%, followed by the Global Dow, the Dow, the S&P 500, and the Nasdaq. Treasury yields fell while the dollar and crude oil prices advanced. It is unclear what drove the market uptick. Some analysts suggest investors may see fiscal relief coming shortly after the election, while others proffer that the market gains were nothing more than dip-buying following last week’s selloff. Each of the major market sectors ended the day in the black, with energy and materials each advancing more than 3.0%.

Equities continued to rally last Tuesday. Election day saw the small caps of the Russell 2000 jump over 3.0% while each of the other benchmark indexes gained at least 1.8%. Treasury yields climbed nearly 4.0% as banks and financials posted solid gains. Crude oil prices advanced 2.9%, but remain below $40 per barrel. The dollar weakened. Although crude oil prices rose, overall energy was the only major sector to lose value last Tuesday. In addition to financials, consumer discretionary and industrials each gained more than 2.0% on the day.

Communication services, technology, health care, and consumer discretionary sectors posted robust gains, pushing market indexes higher last Wednesday. Although the election had yet to be officially decided, investors may be anticipating a fiscal stimulus package, which would provide more resources for investment. The Nasdaq was the big winner, gaining 3.9% on the day, followed by the S&P 500 (2.2%), the Dow (1.6%), the Global Dow (0.6%), and the Russell 2000 (0.05%). Treasury yields and the dollar dropped, while crude oil prices advanced for the third consecutive day.

The market continued to rally last Thursday. The S&P 500 climbed 2.0% and was on track for its best week since April. Tech stocks surged, pushing the Nasdaq ahead 2.6% on the day and more than 9.0% for the week. The Russell 2000 led the pack, advancing 2.8% by the end of trading. Globally, stocks also posted notable gains, driving the Global Dow up 2.1%. Treasury prices fell, moving yields higher. Crude oil prices sank and the dollar fell to its lowest level in more than two years. Among the market sectors, only energy lost, while technology and materials gained 3.1% and 4.1%, respectively.

Stocks were flat to close out the week, with the Global Dow and the Nasdaq posting modest gains, while the remaining benchmark indexes listed here lost value. Among the market sectors, information technology, consumer staples, health care, industrials, and materials advanced marginally. Energy dropped 2.1%. Crude oil and the dollar fell, while Treasury yields advanced.

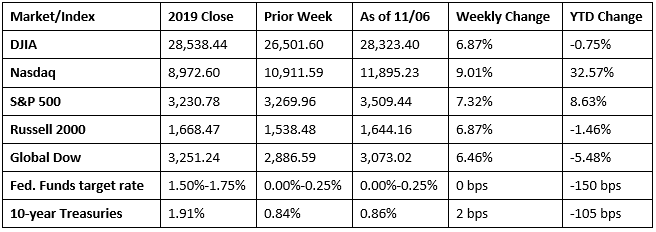

Despite last Friday’s tepid returns, stocks enjoyed their best week since April. Investors may have been anticipating that former Vice President Joe Biden would win the presidential election and Republicans would maintain control of the Senate. This scenario might lead to additional fiscal stimulus but marginal tax increases, if any. While this is purely speculation, it could have been enough to drive investors to stocks last week. The tech-heavy Nasdaq gained 9.0%, followed by the S&P 500, the Dow, the Russell 2000, and the Global Dow. Year to date, The Nasdaq is more than 32.0% above last year’s closing value, while the S&P 500 is more than 8.6% ahead. The Dow has again come within 1.0 percentage point of hitting its 2019 closing mark as the indexes continue to push ahead following the COVID-19 downturn.

Crude oil prices advanced last week, closing at $37.39 per barrel by late Friday afternoon, up from the prior week’s price of $35.61 per barrel. The price of gold (COMEX) closed the week at $1,953.10, up from the prior week’s price of $1,878.00. The national average retail price for regular gasoline was $2.112 per gallon on November 2, $0.031 lower than the prior week’s price and $0.493 less than a year ago.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- October saw 638,000 new jobs added and the unemployment rate drop to 6.9%. While the number of new jobs added has decreased each month since August, the unemployment rate and the number of unemployed persons (11.1 million in October) have declined for six consecutive months. Nevertheless, both the unemployment rate and the number of unemployed persons are nearly twice their February levels, indicative of the impact of the COVID-19 virus. Notable job gains last month occurred in leisure and hospitality; food services and drinking places; arts, entertainment, and recreation; and accommodation. In October, 15.1 million persons reported that they had been unable to work because their employer closed or lost business due to the pandemic, down from 19.4 million in September. In October, 21.2% of employed persons teleworked because of the pandemic, down from 22.7% in September. The labor force participation rate increased by 0.3 percentage point to 61.7% in October, 1.7 percentage points below the February level. The employment-population ratio increased by 0.8 percentage point to 57.4% in October, 3.7 percentage points lower than in February. In October, average hourly earnings increased by $0.04 to $29.50. Average hourly earnings have increased 4.5% over the past 12 months ended in October. The average work week was unchanged at 34.8 hours in October.

- Following its meeting last week, the Federal Open Market Committee decided to leave the target range for the federal funds rate at its current 0%-0.25%. According to the Committee, although economic activity and employment have continued to recover, they remain well below their levels prior to the beginning of the year. Weaker demand and earlier declines in oil prices have been holding down consumer price inflation. The course of the COVID-19 virus will continue to weigh on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term. In addition to maintaining the federal funds target range, the Committee also indicated that it would increase its holdings of Treasury securities and agency mortgage-back securities at the current pace to sustain smooth market functioning and help foster accommodative financial conditions in an effort to support the flow of credit to households and businesses.

- According to the latest Manufacturing ISM® Report On Business®, manufacturing registered 59.3%, up 3.9 percentage points over the September reading and the highest since September 2018, when the index was 59.3%. Survey respondents reported an increase in new orders, production, employment, deliveries, inventories, and prices. Both import and export orders also increased in October over the prior month’s totals.

- Economic activity in the services sector increased in October but at a slower rate, according to the latest Services ISM® Report On Business®. The services purchasing managers’ index registered 56.6% last month, 1.2 percentage points lower than the September reading. A reading above 50% indicates growth. Supplier deliveries, prices, and new export and import orders each increased. Business activity/production, new orders, and employment slowed in October from September.

- According to the Bureau of Economic Analysis, the international trade in goods and services deficit was $63.9 billion in September, 4.7% lower than the August trade deficit. September exports were $176.4 billion, $4.4 billion, or 2.6%, more than August exports. September imports were $240.2 billion, $1.2 billion, or 0.5%, more than August imports. Year to date, the goods and services deficit increased $38.5 billion, or 8.6%, from the same period in 2019. Exports decreased $329.0 billion, or 17.4%. Imports decreased $290.4 billion, or 12.4%.

- For the week ended October 31, there were 751,000 new claims for unemployment insurance, a decrease of 7,000 from the previous week’s level, which was revised up by 7,000. According to the Department of Labor, the advance rate for insured unemployment claims was 5.0% for the week ended October 24, a decrease of 0.3 percentage point from the prior week’s rate. For comparison, during the same period last year, there were 212,00 new jobs added and the insured unemployment claims rate was 1.2%> The advance number of those receiving unemployment insurance benefits during the week ended October 24 was 7,285,000, a decrease of 538,000 from the prior week’s level, which was revised up by 67,000. The highest insured unemployment rates in the week ended October 17 were in Hawaii (11.3%), the Virgin Islands (9.6%), California (9.5%), Nevada (9.2%), and New Mexico (9.0%). The largest increases in initial claims for the week ended October 24 were in Illinois (+6,190), Michigan (+5,442), Massachusetts (+2,483), Minnesota (+1,848), and Connecticut (+1,621), while the largest decreases were in Texas (-10,113), California (-7,700), Florida (-6,528), New York (-3,291), and Louisiana (-3,096).

Eye on the Week Ahead

The predominant question this week continues to focus on the impact that the election will have on the economy in general, and on the market in particular. Economic reports available this month focus on October, so it will take a few months at the very least before we may get a clearer picture of where the economy and market are headed. In any case, economic reports this week focus on consumer and producer prices in October. Also, the Treasury statement is available for October, the first month of fiscal year 2021.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.