Monday kicked off last week on a high note for stocks. Each of the benchmark indexes listed here posted gains, with the Nasdaq advancing 1.4% to lead the way. The S&P 500 gained 1.0%, the Russell 2000 climbed 0.6%, the Dow and the Global Dow each added 0.5%. Information technology and communication services led the market sectors, each rising 1.8%, followed by real estate (1.1%), energy (1.0%), and consumer discretionary (1.0%). The yield on 10-year Treasuries declined 1.5%. The dollar slipped, while crude oil prices climbed 3.7%.

Stocks ended last Tuesday slightly lower as consumer confidence slipped amid concerns of rising inflation. The small caps of the Russell 2000 fell 1.0%, while the Dow, the S&P 500, the Nasdaq, and the Global Dow each dipped no more than 0.2%. The market sectors were mixed, with consumer discretionary, real estate, communication services, consumer staples, and information technology advancing, while industrials, health care, materials, financials, utilities, and energy slid. Treasury yields, crude oil prices, and the dollar declined.

Small caps and tech shares pushed the Russell 2000 and the Nasdaq higher last Wednesday. The Dow and the S&P 500 closed slightly higher, while the Global Dow was unchanged. The yield on 10-year Treasuries fell for the third consecutive day, falling below 1.6%. The dollar and crude oil prices advanced. Only health care and consumer staples failed to advance, as the remaining market sectors pushed higher, led by energy and consumer discretionary.

Last Thursday saw stocks close mostly higher, supported by a drop in initial jobless claims and solid economic data. The Russell 2000 led the way, closing up 2.0%, followed by the Dow (0.4%), the Global Dow (0.3%), and the S&P 500 (0.1%). The Nasdaq was unchanged from the previous day. Treasury yields broke a three-day trend, closing higher. Crude oil prices rose, while the dollar was mixed. Industrials and financials led the market sectors, with consumer staples, utilities, and information technology lagging.

Stocks closed generally higher last Friday with only the Russell 2000 losing value. The Global Dow advanced 0.4%, followed by the Dow (0.2%). The S&P 500 and the Nasdaq each gained 0.1%. Treasury yields and crude oil prices lagged, while the dollar was mixed. Real estate and utilities led the market sectors, which otherwise closed the day mixed.

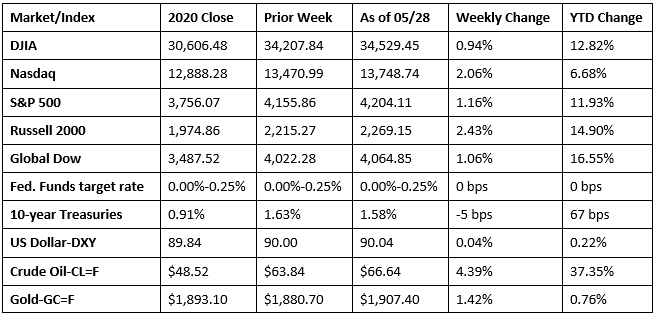

Although last week had its ups and downs, stocks closed generally higher. The Russell 2000 climbed 2.4%. Tech stocks drove the Nasdaq 2.1% higher last week, followed by the S&P 500, the Global Dow, and the Dow. Year to date, the Global Dow has outpaced the other benchmark indexes, with the Russell 2000 close behind. Gold prices continued to advance and crude oil prices climbed $2.80 per barrel. The dollar was little changed, and the yield on 10-year Treasuries dipped. The majority of the market sectors increased last week with only consumer staples, health care, and utilities losing ground.

The national average retail price for regular gasoline was $3.020 per gallon on May 24, $0.008 per gallon lower than the prior week’s price but $1.060 higher than a year ago. U.S. crude oil refinery inputs averaged 15.2 million barrels per day during the week ended May 21, which was 123,000 barrels per day more than the previous week’s average. Refineries operated at 87.0% of their operable capacity last week. Gasoline production decreased last week, averaging 9.7 million barrels per day, down from the prior week’s average of 9.8 million barrels per day.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- Gross domestic product increased at an annual rate of 6.4% in the first quarter of 2021, according to the second estimate released by the Bureau of Economic Analysis. In the fourth quarter of 2020, GDP increased 4.3%. The GDP increase in the first quarter reflected increases in personal consumption expenditures (consumer spending), nonresidential (business) fixed investment, federal government spending, residential fixed investment, and state and local government spending that were partly offset by decreases in private inventory investment and exports. Imports, which are subtracted from GDP, increased. The rise in consumer spending reflected increases in durable goods (led by motor vehicles and parts), nondurable goods (led by food and beverages), and services (led by food services and accommodations). Consumer prices increased 3.7% in the first quarter, compared with an increase of 1.5% in the fourth quarter of 2020. Excluding food and energy, prices increased 2.5%, compared with an increase of 1.3%.

- In what may worry some investors, inflation, as measured by the personal consumption expenditures price index, rose 0.6% in April, and is up 3.6% since April 2020. Prices, less food and energy, advanced 0.7% in April and 3.1% since April 2020. Personal income fell 13.1% in April as government subsidy payments and unemployment insurance decreased. Disposable personal income dipped 14.6% in April. Personal consumption expenditures (consumer spending) rose 0.5% in April.

- Orders for long-lasting (durable) goods declined in April for the first time following 11 consecutive monthly increases. New orders in April fell 1.3% from the March total, but are 22.4% over the April 2020 estimate. Excluding transportation, new orders for durable goods advanced 1.0% in April. Excluding defense, new orders were virtually unchanged in April from the previous month. Transportation equipment, down two consecutive months, drove the April decrease, falling 6.7%. In April, shipments of durable goods increased 0.6%, unfilled orders rose 0.2%, and inventories climbed 0.5%. New orders for nondefense capital goods increased 3.5% in April, while new orders for defense capital goods fell 25.8%.

- The easing of COVID restrictions may be having a positive impact on cross-the-border trade. The international trade in goods (excluding services) deficit in April was $85.2 billion, down $6.8 billion, or 7.3%, from March. Exports of goods for April were $144.7 billion, $1.7 billion, or 1.2%, more than March exports. Imports of goods for April were $229.9 billion, $5.1 billion, or 2.2%, less than March imports. Exports of capital goods rose 4.8% in April, while exports of automotive vehicles fell 8.0%. Imports of foods, feeds, and beverages increased 3.4%, while imports of consumer goods fell 4.2%.

- New home sales dipped in April, according to the latest information from the Census Bureau. Sales of new, single-family homes fell 5.9% from the March estimate. Nevertheless, new home sales are up 48.3% from April 2020. Sales fell in the Northeast (-13.7%), the Midwest (-8.3%), and the South (-8.2%). New home sales increased 7.9% in the West. The median sales price of new houses sold in April was $372,400 (+11.4% from March). The average sales price was $435,400 (+8.7% from March). The estimate of new homes for sale at the end of April was 316,000, which represents a supply of 4.4 months (4.0 months in March).

- For the week ended May 22, there were 406,000 new claims for unemployment insurance, a decrease of 38,000 from the previous week’s level. This is the lowest level for initial claims since March 14, 2020, when it was 256,000. According to the Department of Labor, the advance rate for insured unemployment claims was 2.6% for the week ended May 15, a decrease of 0.1 percentage point from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended May 15 was 3,642,000, a decrease of 96,000 from the prior week’s level, which was revised down by 13,000. For comparison, during the same period last year, there were 1,887,000 initial claims for unemployment insurance, and the insured unemployment claims rate was 13.2%. During the last week of February 2020 (pre-pandemic), there were 219,000 initial claims for unemployment insurance, and the number of those receiving unemployment insurance benefits was 1,724,000. States and territories with the highest insured unemployment rates in the week ended May 8 were in Nevada (5.7%), Connecticut (4.5%), Rhode Island (4.5%), Alaska (4.3%), Puerto Rico (4.3%), California (3.9%), New York (3.9%), Pennsylvania (3.9%), Illinois (3.7%), and Vermont (3.6%). The largest increases in initial claims for the week ended May 15 were in New Jersey (+4,812), Washington (+3,023), Minnesota (+1,806), West Virginia (+907), and Rhode Island (+792), while the largest decreases were in Georgia (-7,392), Kentucky (-7,123), Texas (-3,881), Michigan (-3,560), and Florida (-2,994).

Eye on the Week Ahead

The labor figures for May are out this week. April saw 266,000 new jobs added, which was below expectations, but still encouraging. The May reports on the manufacturing and services sectors are also available this week. Purchasing managers saw favorable increases in both manufacturing and services in April.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.