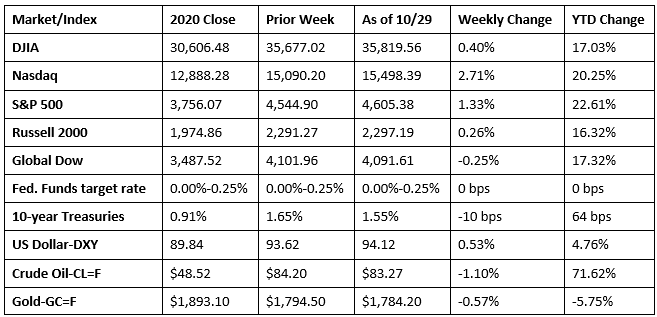

Solid corporate earnings data last week supported a strong week for equities. Investors’ fears that rising inflation, supply-chain snarls, labor shortages, and a surge in COVID-19 cases would hinder corporate earnings have yet to materialize. The Nasdaq led the benchmark indexes, followed by the S&P 500, the Dow, and the Russell 2000. The Global Dow dipped lower. Ten-year Treasury yields, gold, and crude oil prices fell, while the dollar advanced. Among the market sectors, consumer discretionary, communication services, and information technology increased the most, while energy, financials, industrials, and utilities decreased.

Wall Street opened the last week of October in fine fashion, as investors anticipated another spate of positive corporate earnings data. The Dow gained 0.2% and the S&P 500 rose 0.5%, each index closing at a record high. The big gainers were the Nasdaq and the Russell 2000, which added 0.9%. The Global Dow climbed 0.3%. Consumer discretionary, energy, and materials led the market sectors. Crude oil prices and 10-year Treasury yields dipped, while the dollar inched higher.

Last Tuesday proved to be another strong day for equities, with only the Russell 2000 failing to post a gain among the benchmark indexes listed here. The Dow was up 0.4%, and the S&P 500 rose 0.2% to eke out new record highs. The Nasdaq finished up 0.1% and the Global Dow advanced 0.3%. Crude oil and the dollar closed higher, while 10-year Treasuries fell for the fourth consecutive trading day. Most of the market sectors advanced, led by energy, utilities, and health care. Communication services and industrials declined.

The Dow and the S&P 500 fell last Wednesday after setting new records the previous day. The Russell 2000 and the Global Dow also drifted lower, while the Nasdaq was flat. Communication services and consumer discretionary were the only market sectors to advance by the close of trading. Energy fell 2.9% and financials dipped 1.7%. Ten-year Treasury yields closed below 1.60% for the first time in two weeks. Crude oil prices and the dollar also retreated.

Stocks rebounded last Thursday on another round of strong corporate earnings data. Real estate, industrials, and consumer discretionary helped drive the S&P 500 up 1.0% to a new record high. The Dow also recovered from Wednesday’s losses, gaining 0.7%, while the Nasdaq jumped 1.4% to reach a record high. Prices on 10-year Treasuries fell pushing yields higher. Crude oil prices rose to $83.13 per barrel. The dollar dipped nearly 0.5% against a basket of currencies.

Equities closed last week mixed, with the Dow, the S&P 500, and the Nasdaq posting gains, while the Russell 2000 and the Global Dow dipped lower. Ten-year Treasury yields fell on rising inflation and the prospect of interest-rate hikes. Crude oil prices and the dollar advanced. Communication services, health care, and information technology led the market sectors. Real estate, energy, utilities, and materials lost ground.

The national average retail price for regular gasoline was $3.383 per gallon on October 25, $0.061 per gallon more than the prior week’s price and $1.240 higher than a year ago. Gasoline production increased during the week ended October 22, averaging 10.1 million barrels per day. U.S. crude oil refinery inputs averaged 15.0 million barrels per day during the week ended October 22 — 58,000 barrels per day more than the previous week’s average. Refineries operated at 85.1% of their operable capacity, up from the prior week’s level of 84.7%.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The initial or “advance” estimate of third-quarter gross domestic product showed that economic growth slowed more than expected, as rising cases of the Delta variant led to new restrictions and delays in business reopenings. Gross domestic product increased at an annual rate of 2.0% in the third quarter. In the second quarter, GDP increased 6.7%. Consumer spending, as measured by personal consumption expenditures, increased 1.6% compared with an increase of 12.0% in the second quarter, likely reflective of decreasing government assistance. Consumer spending on services rose 7.9% in the third quarter, while durable goods expenditures contracted 26.2%. Fixed investment dipped 0.8%, driven lower by a 7.7% drop in residential fixed investment. Exports decreased 2.55%, while imports (a negative in the calculation of GDP) rose 6.1%. The personal savings rate fell from 10.5% in the second quarter to 8.9% in the third quarter. Disposable (after-tax) personal income decreased 0.7% compared to a 25.7% drop in the second quarter. The personal consumption expenditures price index, a measure of inflation, increased 5.3% in the third quarter, compared with an increase of 6.5% in the second quarter.

- Personal income (-1.0%) and disposable personal income (-1.3%) fell in September, reflective of a decrease in government social benefit payments in response to the pandemic. Wages and salaries rose 0.8% and personal income receipts on assets increased 0.2%. The drop in personal income didn’t greatly impact consumer spending, which advanced 0.6% in September. Consumer prices for goods and services increased 0.3% in September, the same increase as in August. For the 12 months ended in September, consumer prices have risen 4.4%. Excluding food and energy, consumer prices are up 3.6% since September 2020.

- Sales of new single-family homes surged in September, climbing 14.0% above the August rate. Despite the September increase, new home sales are 17.6% below the September 2020 estimate. The median sales price of new houses sold in September 2021 was $408,800. The average sales price was $451,700. The estimate of new houses for sale at the end of September was 379,000, which represents a supply of 5.7 months at the current sales pace.

- New orders for long-lasting, durable goods slipped in September, falling 0.4% following four consecutive monthly increases. Excluding transportation, new orders increased 0.4%. Excluding defense, new orders decreased 2.0%. Transportation equipment, down two of the last three months, drove the decrease, dropping $1.8 billion, or 2.3%. Several categories saw new orders fall in September including computers and electronic products (-0.3%), electrical equipment, appliances, and components (-0.5%), motor vehicles and parts (-2.9%), and nondefense aircraft and parts (-27.9%). New orders for defense aircraft and parts increased 104.3% in September. New orders for capital goods (used in the production of other consumer goods) dipped 0.4%, pulled lower by a 4.2% drop in nondefense capital goods. New orders for defense capital goods rose 28.4%.

- The advance report on international trade in goods for September showed the deficit increased $8.1 billion, or 9.2%, to $96.3 billion. Exports of goods for September were $142.2 billion, $7.0 billion, or 4.7%, less than August exports. Imports of goods for September were $238.4 billion, $1.1 billion, or 0.5%, more than August imports.

- For the week ended October 23, there were 281,000 new claims for unemployment insurance, a decrease of 10,000 from the previous week’s level, which was revised up by 1,000. This is the lowest level for initial claims since March 14, 2020, when it was 256,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended October 16 was 1.7%, a decrease of 0.1 percentage point from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended October 16 was 2,243,000, a decrease of 237,000 from the prior week’s level, which was revised down by 1,000. This is the lowest level for insured unemployment since March 14, 2020, when it was 1,770,000. For comparison, last year at this time, there were 768,000 initial claims for unemployment insurance, and the rate for unemployment claims was 5.3%. During the last week of February 2020 (pre-pandemic), there were 219,000 initial claims for unemployment insurance, and the number of those receiving unemployment insurance benefits was 1,724,000. States and territories with the highest insured unemployment rates for the week ended October 9 were the District of Columbia (7.4%), Puerto Rico (3.7%), California (3.2%), Georgia (2.7%), Illinois (2.7%), Hawaii (2.6%), New Jersey (2.5%), Nevada (2.4%), the Virgin Islands (2.4%), and Alaska (2.3%). The largest increases in initial claims for the week ended October 16 were in California (+9,748), Tennessee (+1,688), Florida (+1,266), Georgia (+1,088), and Illinois (+512), while the largest decreases were in Virginia (-7,380), Michigan (-4,083), Pennsylvania (-4,033), Kentucky (-2,753), and Ohio (-2,287).

Eye on the Week Ahead

The latest employment figures for October are available at the end of this week. September saw 194,000 new jobs added, although the unemployment rate continued to fall, settling at 4.8%. The Markit purchasing managers surveys for manufacturing and services are also out this week. Survey respondents have noted that supply bottlenecks and labor shortages have hindered overall production.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.