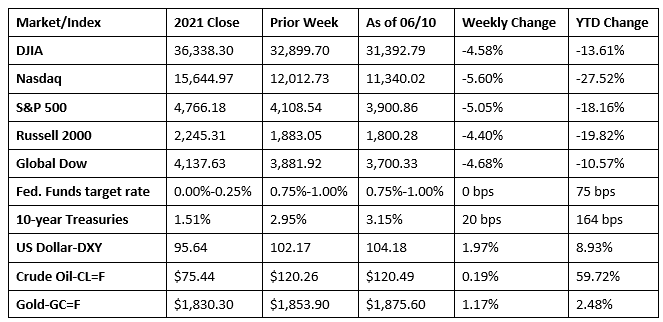

U.S. stocks tumbled with their biggest losses in three weeks, and Treasury yields rose by 20 basis points as inflation continued to push higher. Each of the benchmark indexes listed here declined, led by the Nasdaq and the S&P 500, which dropped by more than 5.0%. Crude oil prices rose marginally, the dollar inched higher, while gold prices rose by more than $22.00 per ounce. Last Friday, the latest data showed that the Consumer Price Index rose 8.6% in May from one year earlier, the fastest pace since 1981. Several factors are driving price pressures including the Russia/Ukraine war, which has impacted energy and crude oil prices; supply-chain disruptions; China’s economic lockdown in response to rising COVID cases; and a tight labor market, with demand for workers far outpacing supply, driving wages higher. Demand for travel and other services has surged with the onset of summer and the receding impact of COVID-19, pushing up prices for airline fares, hotels, and dining. Unfortunately, higher prices are cutting into profits for many businesses. Also, in its attempt to temper inflationary pressures, the Federal Reserve is likely to step up measures to tighten spending by raising interest rates further increasing the cost of borrowing and doing business. For consumers in general and investors in particular, higher prices are likely to impact consumer spending and slow economic activity.

Stocks posted modest gains last Monday. A sell-off in Treasuries sent 10-year yields above 3.0% for the first time since mid-May. The Nasdaq gained 0.4%, while the Global Dow, the Russell 2000, and the S&P 500 rose 0.3%. The Dow eked out a 0.1% advance. Crude oil prices slipped marginally, closing at around $118.50 per barrel. The dollar advanced, while gold prices fell more than $5.00 to $1,845.10 per ounce. China is set to begin easing COVID-related restrictions that could help ease supply-chain pressures. Elsewhere, the European Central Bank is about to end bond purchases and increase borrowing costs, likely in July.

Equities pushed higher last Tuesday led by energy and tech shares. Stocks recovered from a dip early in the day following news that a major retailer cut in its profit outlook. A drop in bond yields helped fuel the surge in stocks. By the close of trading last Tuesday, the Nasdaq and the S&P 500 rose 1.0%, the Dow gained 0.8%, the Russell 2000 jumped 1.6%, and the Global Dow increased 0.3%. Ten-year Treasury yields fell 6.6 basis points to end the day at 2.97%. Crude oil prices continued to push toward $120.00 per barrel after ending the day at $119.63. The dollar slipped lower while gold prices advanced.

Stocks slid lower last Wednesday following a two-day rally. Each of the benchmark indexes lost value, with the Russell 2000 falling nearly 1.6%. The Nasdaq dropped 1.1%, the Dow lost 0.8%, while the S&P 500 and the Global Dow dipped 0.7%. Bond prices declined, with yields on 10-year Treasuries rising 5.7 basis points to reach 3.02%. The dollar and gold prices increased. Crude oil prices continued to advance, climbing another $3.14 to hit $122.55 per barrel. Rising crude oil prices and related gas price increases are prompting concerns that economic growth will be stifled and corporate earnings will take a hit.

Last Thursday saw stocks extend their slide as investors contemplated more economic growth concerns following the European Central Bank’s intention to hike interest rates by a quarter-point next month. Each of the benchmark indexes listed here fell by nearly 1.9%. Ten-year Treasury yields remained above 3.0%, the dollar rose, while gold prices dipped lower. Crude oil prices slipped, down $0.75 to close around $121.36 per barrel.

Investors withdrew from stocks last Friday after the latest jump in the Consumer Price Index likely signaled more economic tightening. The Nasdaq plunged 3.5% on the day, followed by the S&P 500 and the Global Dow (-2.9%), the Dow (-2.7%), and the Russell 2000 (-2.6%). The yield on 10-year Treasuries jumped more than 11 basis points to close at 3.15%. Crude oil prices retreated to $120.49 per barrel. The Dollar rose against a basket of currrencies. Gold prices climbed nearly $23.00 to reach $1,875.60 per ounce.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The Consumer Price Index rose 1.0% in May after advancing 0.3% in April. The CPI has risen 8.6% since May 2021, the highest level in more than 40 years. While the May increase was broad-based, rising prices for shelter, gasoline, and food were the largest contributors. The CPI less food and energy rose 0.6% last month. The latest data is likely to promote further tightening of monetary policy by the Federal Reserve, which meets next week. Gasoline prices jumped 4.1% in May and are up nearly 50.0% over the last 12 months. According to the Energy Information Administration, the average price of regular gasoline was $4.88 per gallon on June 6. Food prices advanced 1.0% in May and 8.6% over the last 12 months. Shelter prices increased 0.6% in May and 5.5% since May 2021.

- The federal Treasury budget deficit was $66.2 billion in May after running a $308.3 billion surplus in April. In May, government receipts declined nearly $474.6 billion to $389.0 billion, while expenditures dipped $100.2 billion to $455.2 billion. Year to date, the budget deficit sits at $426.2 billion, more than 380% lower than the deficit over the same period last year.

- The goods and services trade deficit fell to $87.1 billion in April, a decrease of 19.1% from the prior month’s figure. According to the latest information from the Bureau of Economic Analysis, in April exports increased 3.5% from March, while imports fell 3.4%. Year to date, the goods and services deficit increased $107.9 billion, or 41.1%, from the same period in 2021. Exports increased $151.3 billion, or 18.8%. Imports increased $259.2 billion, or 24.3%. Of particular note in April, the deficit with China decreased $8.5 billion to $34.9 billion, while the deficit with Mexico increased $1.7 billion to $11.5 billion.

- The national average retail price for regular gasoline was $4.876 per gallon on June 6, $0.252 per gallon above the prior week’s price and $1.841 higher than a year ago. Also as of June 6, the East Coast price increased $0.17 to $4.72 per gallon; the Gulf Coast price rose $0.33 to $4.55 per gallon; the Midwest price climbed $0.36 to $4.82 per gallon; the West Coast price increased $0.19 to $5.75 per gallon; and the Rocky Mountain price increased $0.26 to $4.71 per gallon. Residential heating oil prices averaged $4.28 per gallon on June 3, about $0.28 per gallon more than the prior week’s price. According to the U.S. Energy Information Administration forecast, non-OPEC countries will increase petroleum production by 1.9 million barrels per day in 2022 and 1.4 million barrels per day in 2023, compared with an increase of 0.8 million barrels per day in 2021. About 60% of the growth in petroleum production will be driven by the United States, whose production will increase by 1.3 million barrels per day in 2022 and by 1.4 million barrels per day in 2023.

- For the week ended June 4, there were 229,000 new claims for unemployment insurance, an increase of 27,000 from the previous week’s level, which was revised up by 2,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended May 28 was 0.9%, unchanged from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended May 28 was 1,306,000, unchanged from the previous week’s revised level which was revised down by 3,000. States and territories with the highest insured unemployment rates for the week ended May 21 were California (1.9%), New Jersey (1.8%), Alaska (1.5%), New York (1.4%), Puerto Rico (1.4%), Pennsylvania (1.3%), Illinois (1.2%), Massachusetts (1.2%), Rhode Island (1.2%), and the Virgin Islands (1.2%). The largest increases in initial claims for the week ended May 28 were in Mississippi (+1,935), California (+1,911), New York (+1,054), Oklahoma (+753), and Michigan (+582), while the largest decreases were in Kentucky (-3,523), Pennsylvania (-2,127), Georgia (-1,762), Florida (-1,520), and Indiana (-426).

Eye on the Week Ahead

The Federal Open Market Committee meets this week. It is expected that the federal funds rate will be increased 50 basis points to 1.25%-1.50%. While indicators in April appeared to show inflation was slowing, the latest data in May has price increases accelerating at a faster pace.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.