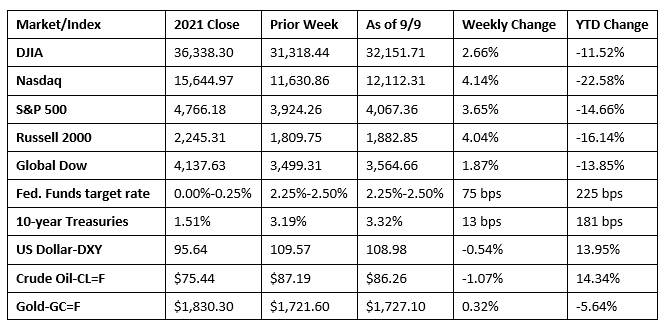

Are investors accepting the Federal Reserve’s hawkish path to reduce inflation? Last week’s market performance may lend credence to that possibility, as each of the benchmark indexes listed here posted solid gains, reversing three weeks of losses. A jump in tech shares pushed the Nasdaq up to its highest level since late August. The S&P 500 passed its 100-day average, and the Russell 2000 added more than 4.0%. The dollar dipped lower, moving away from a record high. Gold prices increased. Crude oil prices decreased for the second consecutive week. There have been few signs that the aggressive interest-rate hike agenda pushed by the Fed will hinder the economy, possibly easing investor worries.

Stocks edged lower last Tuesday to kick off the holiday-shortened week. The Russell 2000 dropped 1.0%, followed by the Nasdaq (-0.7%), the Dow and the Global Dow (-0.6%), and the S&P 500 (-0.4%). Every market sector except energy moved higher. The yield on 10-year Treasuries jumped 15.0 basis points to 3.34%. Crude oil prices fell nearly $0.50, settling at $86.73 per barrel. The dollar rose, while gold prices fell.

Wall Street enjoyed its best day in a month last Wednesday as stocks rebounded and bond yields tumbled. The Nasdaq surged to its biggest jump in three weeks after gaining 2.1%. The small caps of the Russell 2000 added 2.1%, while the S&P 500 (1.8%) and the Dow (1.4%) notched gains. The Global Dow rose 0.6%. Crude oil prices fell to a new seven-month low after settling at $81.87 per barrel. Ten-year Treasury yields dipped 7.5 basis points to 3.26%. The dollar declined 0.6%, while gold prices jumped nearly $16.00 to $1,728.60 per ounce.

Last Thursday, gains by financial and health-care stocks helped drive Wall Street to its second consecutive positive session. While each of the benchmark indexes listed here gained ground, markets across the globe declined over worries that aggressive policies aimed at curtailing inflation would stall the economy. Indicative of monetary tightening, the European Central Bank hiked interest rates by 75 basis points and indicated further hikes were likely. Domestically, the Russell 2000 and the Global Dow rose 0.8%. The S&P 500 gained 0.7%, while the Dow and the Nasdaq added 0.6%. Ten-year Treasury yields climbed 2.7 basis points, ending the day at 3.29%. Crude oil prices inched higher, the dollar dipped lower, and gold prices fell 0.5% to $1,719.30 per ounce.

Stocks extended last Thursday’s gains into Friday as investors gobbled up perceived bargains after three weeks of declines. Each of the benchmark indexes added value last Friday, led by the Nasdaq (2.1%), followed by the Russell 2000 (1.9%), the Global Dow (1.7%), the S&P 500 (1.5%), and the Dow (1.2%). The market sectors rose higher, led by communication services, consumer discretionary, energy, and information technology. Crude oil prices rose $2.72 to $86.26 per barrel. Gold prices advanced, while the dollar dipped lower. Yields on 10-year Treasuries increased 2.9 basis points, reaching 3.32%.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- According to the latest report the S&P Global US Services PMI™ revealed that business activity in the services sector in August contracted at its sharpest pace since May 2020. Weak domestic and foreign demand stunted new orders, which led to the softest rate of hiring in the services sector since January. Input and output cost inflation eased to the slowest rate in a year and a half.

- The goods and services trade deficit for July declined by $10.2 billion, or 12.6%, from June. A marginal (0.2%) increase in exports was outpaced by a 2.9% drop in imports. Year to date, the goods and services deficit increased by $136.6 billion, or 29.0%, from the same period in 2021. Exports increased 19.9%, while imports increased 22.1%.

- The national average retail price for regular gasoline was $3.746 per gallon on September 5, $0.081 per gallon below the prior week’s price but $0.570 higher than a year ago. Also as of September 5, the East Coast price decreased $0.109 to $3.613 per gallon; the Gulf Coast price fell $0.127 to $3.229 per gallon; the Midwest price dropped $0.037 to $3.638 per gallon; the West Coast price slid $0.042 to $4.741 per gallon; and the Rocky Mountain price fell $0.080 to $3.940 per gallon. Residential heating oil prices averaged $3.578 per gallon on September 2, about $0.430 per gallon less than the prior week’s price.

- For the week ended September 3, there were 222,000 new claims for unemployment insurance, a decrease of 6,000 from the previous week’s level, which was revised down by 4,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended August 27 was 1.0%, unchanged from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended August 27 was 1,473,000, an increase of 36,000 from the previous week’s level, which was revised down by 1,000. States and territories with the highest insured unemployment rates for the week ended August 20 were New Jersey (2.2%), California (1.9%), Rhode Island (1.8%), Connecticut (1.7%), New York (1.7%), Puerto Rico (1.7%), Massachusetts (1.5%), Pennsylvania (1.3%), and Nevada (1.2%). The largest increases in initial claims for the week ended August 27 were in New York (+4,630), Michigan (+1,199), South Carolina (+290), Hawaii (+263), and New Jersey (+256), while the largest decreases were in Connecticut (-2,635), Oklahoma (-1,260), Missouri (-1,250), Georgia (-853), and California (-802).

Eye on the Week Ahead

Several important indicators of inflation are out this week with the August releases of the Consumer Price Index, the Producer Price Index, and the report on import and export prices. Each of these indicators showed that inflation subsided in July with the CPI registering no change, while producer prices fell 0.5%, import prices dipped 1.4%, and export prices slid 3.3%. Similar data for August may influence the Federal Reserve to scale back its current aggressive economic tightening policy.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.