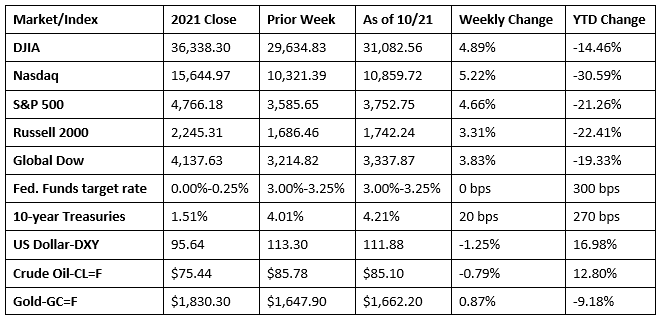

Wall Street enjoyed a notable surge last week, as investors clung to hopes the Federal Reserve may consider scaling back its aggressive policy stance against rising inflation. A report last Friday indicated that some members of the Fed are willing to debate a smaller interest-rate hike in December, while slowing down the pace of increases moving forward. The Dow, the S&P 500, and the Nasdaq notched their largest weekly gains in four months. Investors looked favorably on risk last week after some favorable company quarterly results, lower company stock valuations, and a reversal of economic policy in the United Kingdom, which led to the resignation of its prime minister. Long-term bond yields advanced last week, gold prices closed higher, while the dollar slipped lower. Crude oil prices dipped on fears of a global economic slowdown.

Stocks surged higher last Monday. Investor sentiment was buoyed by a batch of solid earnings data from some major banks, coupled with the United Kingdom’s reversal of fiscal stimulus proposals announced in September. Technology and consumer discretionary shares gained notably, helping push the Nasdaq up 3.4%, while the S&P 500 rose 2.7%, with all 11 sectors posting gains. The Russell 2000 added 3.2%, the Dow climbed 1.9%, and the Global Dow advanced 1.8%. Ten-year Treasury yields gained minimally, closing at 4.01%. Crude oil prices dipped slightly, ending the day around $85.58 per barrel. The dollar swung lower, while gold prices advanced.

Last Tuesday, Wall Street enjoyed a second day of positive returns. Instead of focusing on the potential of an economic recession driven by higher interest rates, investors assessed the impact of actual corporate earnings on the economy. Each of the benchmark indexes listed here added value, with the S&P 500, the Dow, and the Russell 2000 gaining a little more than 1.1%. The Nasdaq and the Global Dow rose 0.9%. Crude oil prices fell $2.26 to $83.20 per barrel on reports that the United States may release more oil from the Strategic Petroleum Reserve. The yield on 10-year Treasuries dipped to 3.99%, the dollar was flat, while gold prices slid lower.

Stocks failed to keep the rally going last Wednesday as each of the benchmark indexes listed here ended the day in the red. The Russell 2000 dropped 1.7% to lead the decline, followed by the Nasdaq (-0.9%), the S&P 500 (-0.7%), the Global Dow (-0.5%), and the Dow (-0.3%). With the decline in stock values, Treasury yields rose higher, with the 10-year note adding 12.9 basis points to end the session at 4.12%. Crude oil prices climbed to $85.88 per barrel. The dollar advanced, while gold prices fell for the second consecutive day.

Last Thursday saw stocks slide lower for the second consecutive day. The Russell 2000 fell 1.2%, followed by the S&P 500 (-0.8%), the Nasdaq (-0.6%), the Global Dow (-0.4%), and the Dow (-0.3%). Ten-year Treasury yields added another 9.9 basis points to hit 4.22%. Crude oil prices fell minimally to $85.71 per barrel. The dollar and gold prices declined.

Following two days of negative returns, stocks surged higher to end the week last Friday. Each of the benchmark indexes listed here closed the day solidly in the black, led by the Dow (2.5%) and followed by the S&P 500 (2.4%), the Nasdaq (2.3%), the Russell 2000 (2.2%), and the Global Dow (1.5%). Ten-year Treasury yields slid marginally lower to 4.21%. Crude oil prices closed at about $85.13 per barrel. The dollar fell, while gold prices advanced.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- Industrial production increased 0.4% in September after declining 0.1% the previous month. In September, manufacturing output rose 0.4% for the second consecutive month. Mining moved up 0.6% while utilities fell 0.3% last month. Overall, total industrial production in September was 5.3% above its year-earlier level.

- The number of issued residential building permits rose 1.4% in September over the August total but remain 3.2% below the September 2021 pace. Issued permits for single-family home construction in September were 3.1% below the previous month’s level. Building permits for multi-family residences drove the overall increase in September, with permits for 2-4 units increasing 2.1% and permits for residences of 5 or more units rising 8.2%. In September, housing starts were 8.1% lower than the August total and 7.7% under the September 2021 rate. Single-family housing starts in September were 4.7% below the August figure. Housing completions rose 6.1% in September and 15.7% above the September 2021 rate. Completions of single-family homes in September were 3.2% above the August pace.

- Sales of existing homes fell 1.5% in September, marking the eighth consecutive month of declines. Since September 2021, existing-home sales are down 23.8%. Relatively low inventory and rising mortgage interest rates, which are nearing 7.0% nationally, are factors that have slowed sales. In September, unsold inventory sat at a 3.2-month supply at the current sales pace, unchanged since July. The median existing-home price in September was $384,800, down from $391,700 in August but higher than the September 2021 price of $355,100. Sales of existing single-family homes slipped 0.9% last month and are down 23.0% over the last 12 months. The median existing single-family home price was $391,000 in September, down from $398,800 in August but up from $361,800 in September 2021.

- Gasoline prices decreased last week. According to the U.S. Energy Administration, the national average retail price for regular gasoline was $3.871 per gallon on October 17, $0.041 per gallon below the prior week’s price but $0.549 higher than a year ago. Also as of October 17, the East Coast price increased $0.045 to $3.524 per gallon; the Gulf Coast price rose $0.025 to $3.319 per gallon; the Midwest price fell $0.093 to $3.788 per gallon; the West Coast price decreased $0.231 to $5.442 per gallon; and the Rocky Mountain price decreased $0.030 to $3.917 per gallon. Residential heating oil prices averaged $5.726 per gallon on October 17, $0.381 above the previous week’s price and $2.360 per gallon more than a year ago.

- For the week ended October 15, there were 214,000 new claims for unemployment insurance, a decrease of 12,000 from the previous week’s level, which was revised down by 2,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended October 8 was 1.0%. The advance number of those receiving unemployment insurance benefits during the week ended October 8 was 1,385,000, an increase of 21,000 from the previous week’s level, which was revised down by 4,000. States and territories with the highest insured unemployment rates for the week ended October 1 were California (1.7%), New Jersey (1.7%), New York (1.3%), Alaska (1.2%), Massachusetts (1.2%), Rhode Island (1.2%), and Nevada (1.1%). The largest increases in initial claims for unemployment insurance for the week ended October 8 were in Florida (+10,665), California (+4,996), New York (+3,387), Texas (+2,382), and Pennsylvania (+1,900), while the largest decreases were in Missouri (-3,137), North Carolina (-1,520), Connecticut (-897), Puerto Rico (-431), and Arkansas (-138).

Eye on the Week Ahead

This is an important week for economic data. The initial estimate of the third-quarter gross domestic product is released this week. GDP has retracted over each of the first two quarters of the year declining 0.6% in the second quarter. Also out this week is the September data on personal income and spending. This report includes the personal consumption expenditures price index, a measure of inflation favored by the Federal Reserve.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.