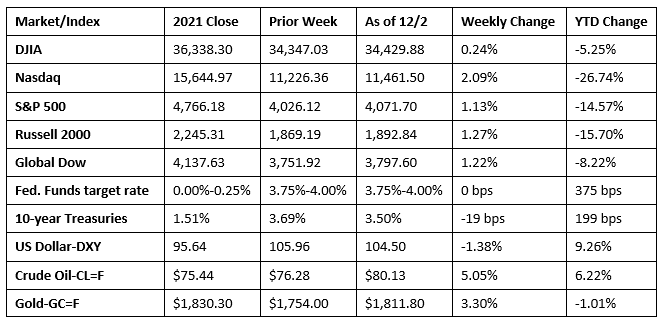

Wall Street extended its rally for the second consecutive week as each of the benchmark indexes listed here posted gains. As is most often the case lately, the market experienced plenty of volatility last week. Ultimately, a hotter-than-expected labor report reignited inflation concerns and the continuation of an aggressive monetary policy by the Federal Reserve. Average hourly earnings have steadily increased over the past three months, while solid monthly job gains have shown that there are more positions to be filled. Investors not only dealt with inflation concerns and the Fed’s response, but traders had to assess the impact of the ongoing Russia/Ukraine war and China’s response to rising COVID cases. Despite the tumult, stocks continued to advance. Ten-year Treasury yields fell as bond prices climbed higher. Crude oil prices rallied from a three-week lag, advancing 5.0%. The dollar slid lower, while gold prices posted gains for the second week in a row.

Last Monday, Wall Street reacted negatively to the likelihood of more interest-rate hikes and the potential economic impact of China’s COVID-related lockdowns. The small caps of the Russell 2000 dropped 2.1% to lead the declining benchmark indexes. The Nasdaq fell 1.6%, while the S&P 500 and the Dow lost 1.5%. The Global Dow slid 1.4%. Ten-year Treasury yields inched up 1.2 basis points to 3.70%. Crude oil prices and the dollar advanced marginally, while gold prices fell 0.8%. Investors were discouraged to hear several Federal Reserve officials indicate that more work has to be done to curb inflation, including more substantial interest-rate increases. China’s response to rising COVID cases has led to demonstrations, which has added to that country’s uncertain economic situation.

Stocks ended mixed last Tuesday, with the Nasdaq (-0.6%) and the S&P 500 (-0.2%) declining, while the Russell 2000 (0.4%) and the Global Dow (0.2%) eked out gains. The Dow ended the session flat. The yield on 10-year Treasuries climbed 4.5 basis points to close at 3.74%. Crude oil prices, gold prices, and the dollar advanced. Investors may have tempered their enthusiasm for risk in anticipation of Federal Reserve Chair Jerome Powell’s speech on Wednesday.

News that the Federal Reserve may soften the pace of interest-rate hikes sent stocks higher last Wednesday. The Nasdaq surged 4.4% and the S&P 500 gained 3.1% to lead the benchmark indexes listed here. The Russell 2000 advanced 2.6%, followed by the Dow (2.2%) and the Global Dow (1.7%). Crude oil prices rose for the first time in several sessions following a report that U.S. reserves declined and that China may lessen COVID-related restrictions. Long-term bond prices advanced, pulling yields lower. Ten-year Treasury yields slid 4.5 basis points to 3.70%. The dollar slid lower, while gold prices increased.

Stocks closed last Thursday mixed following the prior day’s rally as investors awaited the latest jobs report due out the following day. Of the benchmark indexes listed here, only the Nasdaq (0.1%) and the Global Dow (0.9%) closed in the black. The Dow (-0.6%) led the declining indexes, followed by the Russell 2000 (-0.3%) and the S&P 500 (-0.1%). Ten-year Treasury yields dropped 17.4 basis points to 3.52% as bond prices jumped higher. The dollar declined, while gold prices climbed notably higher, gaining $57.20 to reach $1,817.10 per ounce. Crude oil prices advanced minimally, closing at about $81.33 per barrel.

Last Friday saw stocks close with mixed results. The Russell 2000 gained 0.6%, while the Dow and the Global Dow barely eked out gains. The Nasdaq slid 0.2% and the S&P 500 dipped 0.1%. The much anticipated jobs report (see below) came in better than expected, adding to the likelihood that the Federal Reserve will keep tightening even if the pace of interest-rate hikes slows. Ten-year Treasury yields fell for the third straight session, down 2.3 basis points to close at 3.50%. Crude oil prices scaled back after a brief rally, dipping $1.10 to end the session at about $80.13 per barrel. The dollar and gold prices declined.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- There were 263,000 new jobs added in November, in line with average growth over the prior three months (282,000). By comparison, 647,000 new jobs were added in November 2021. Job growth has averaged 392,000 in 2022, evidencing a slowdown in the number of new jobs added over the second half of the year. In November, notable job gains occurred in leisure and hospitality, health care, and government. Employment declined in retail trade and in transportation and warehousing. The unemployment rate, at 3.7%, was unchanged in November and has sat within a range of 3.5% to 3.7% since March. The number of unemployed persons slid by 48,000 to 6.0 million in November. Both the labor force participation rate and the employment-population ratio dipped one percentage point to 62.1% and 59.9%, respectively. In November, average hourly earnings rose by $0.18, or 0.6%, to $32.82. Over the past 12 months, average hourly earnings have increased by 5.1%. In November, the average work week declined by 0.1 hour to 34.4 hours.

- The second estimate of gross domestic product revealed that the economy accelerated at an annualized rate of 2.9% in the third quarter. The initial estimate showed the GDP advanced 2.6%. GDP decreased 0.6% in the second quarter. The increase in GDP reflected increases in exports, consumer spending, nonresidential (business) fixed investment, state and local government spending, and federal government spending that were partly offset by decreases in residential fixed investment and private inventory investment. Imports, which are a negative in the calculation of GDP, decreased. Personal consumption expenditures, a measure of consumer spending, rose 1.7% in the third quarter, while the personal consumption expenditures price index, a measure of inflation, increased 4.3%.

- Personal income advanced a notable 0.7% in October, according to the latest data from the Bureau of Economic Analysis. Consumers were apparently undeterred by rising prices and interest rates as personal consumption expenditures advanced 0.8% in October. The personal consumption expenditures price index, a measure of inflation, advanced 0.3% in October and 6.0% for the last 12 months, down from 6.2% for the 12 months ended in September. Core prices, excluding food and energy, rose 0.2% in October and 5.0% since October 2021, down 0.2 percentage point from the same period ended in September.

- In October, the number of job openings edged down 353,000 to 10.3 million, according to the latest Job Openings and Labor Turnover Summary. In October, job openings decreased in state and local government (excluding education), nondurable goods manufacturing, and federal government. The number of job openings increased in other services and in finance and insurance. In October, the number and rate of hires changed little at 6.0 million and 3.9%, respectively. In October, the number of total separations, which include quits, layoffs, and discharges, changed little at 5.7 million, and the rate was unchanged at 3.7%.

- The manufacturing sector weakened in November, according to the S&P Global US Manufacturing PMI™. The purchasing managers’ index posted 47.7 in November, down from 50.4 in October, marking the first decline in the manufacturing sector since June 2020. The downturn in operating conditions was widespread, with decreases in production, output, and new orders. Employment growth slowed as backlogs of work waned.

- According to the latest data from the Census Bureau, the international trade in goods deficit increased 7.7% to $99.0 billion in October. Exports fell $4.7 billion, or 2.6%, while imports increased $2.4 billion, or 0.9%.

- According to the U.S. Energy Administration, the national average retail price for regular gasoline was $3.534 per gallon on November 28, $0.114 per gallon below the prior week’s price but $0.154 higher than a year ago. Also as of November 28, the East Coast price decreased $0.070 to $3.468 per gallon; the Gulf Coast price fell $0.106 to $2.915 per gallon; the Midwest price declined $0.145 to $3.374 per gallon; the West Coast price dropped $0.187 to $4.592 per gallon; and the Rocky Mountain price decreased $0.097 to $3.539 per gallon. Residential heating oil prices averaged $5.147 per gallon on November 28, $0.284 below the previous week’s price but $1.784 per gallon more than a year ago.

- Claims for unemployment insurance declined during the last reporting period. For the week ended November 26, there were 225,000 new claims for unemployment insurance, a decrease of 16,000 from the previous week’s level, which was revised up by 1,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended November 19 remained at 1.1%. The advance number of those receiving unemployment insurance benefits during the week ended November 19 was 1,608,000, an increase of 57,000 from the previous week’s level. States and territories with the highest insured unemployment rates for the week ended November 12 were Puerto Rico (2.1%), Alaska (2.0%), New Jersey (2.0%), California (1.8%), New York (1.4%), Massachusetts (1.3%), Montana (1.3%), Rhode Island (1.3%), Minnesota (1.2%), Washington (1.2%), and Oregon (1.2%). The largest increases in initial claims for unemployment insurance for the week ended November 19 were in Illinois (+6,586), California (+4,423), Georgia (+3,717), Michigan (+3,031), and Minnesota (+2,896), while the largest decreases were in Montana (-318), North Carolina (-133), and Arkansas (-131).

Eye on the Week Ahead

The Producer Price Index for November is available at the end of this week. The PPI is a measure of the change in prices received by producers of goods and services, and is an indicator of inflation. October saw producer prices rise by 0.2%, which was below expectations. For the year, producer prices fell from 8.5% for the 12 months ended in September to 8.0% for the year ended in October.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.