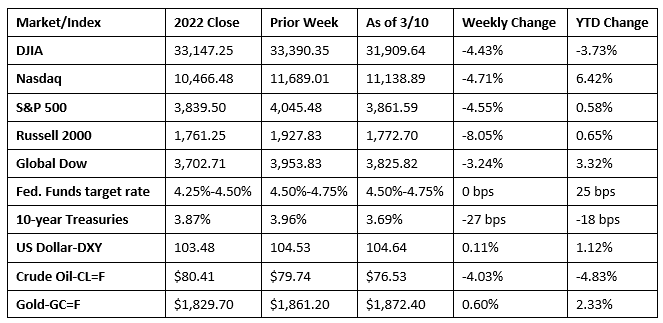

Entering last week, investors were poised to review the latest employment data and its potential impact on the course of the Federal Reserve. Instead, last Friday saw financial regulators close Silicon Valley Bank as the Federal Deposit Insurance Corporation (FDIC) took control of the bank’s assets. All in all, Wall Street suffered through its worst week in 2023. Each of the benchmark indexes listed here lost notable value, led by the Russell 2000, which dropped more than 8.0%. The Dow has now fallen more than 3.7% below its 2022 closing value. The yield on 10-year Treasuries dropped from around 4.0% earlier in the week to 3.7% last Friday. The dollar ended the week eking out a gain, while gold prices were buoyed by a weaker dollar and reduced expectations that the Fed will be more aggressive with its interest-rate hikes.

Stocks began last Monday on an upswing, only to end the day finishing mixed. For most of the day, it appeared Wall Street was going to continue the rally from the previous week. Unfortunately, the Nasdaq (-0.1%) and the Russell 2000 (-1.5%) closed lower, while the Dow and the S&P 500 barely eked out gains of 0.1%. Ten-year Treasury yields inched higher, closing at 3.98%. Crude oil prices cracked the $80.00 mark, finishing at $80.56 per barrel. The dollar and gold prices slid lower.

Last Tuesday, Wall Street responded negatively to Federal Reserve Chair Jerome Powell’s assertion that interest rates would likely be raised more than previously suggested in order to fight rising inflation and cool the economy. Equities fell, while shorter-term Treasury yields and the dollar climbed higher. Each of the benchmark indexes listed here declined, with the Dow falling 1.7%, followed by the S&P 500 and the Global Dow (-1.5%), the Nasdaq (-1.3%), and the Russell 2000 (-1.1%). Yields on 10-year Treasuries dipped to 3.97%. Crude oil ended its five-session rally, declining $3.15 to $77.31 per barrel, the largest single-day drop in two months. Gold prices fell nearly 2.0%, while the dollar rose 1.3%.

Stocks finished mixed last Wednesday, with the Dow (-0.2%) and the Global Dow (-0.1%) falling, while the Nasdaq (0.4%) and the S&P 500 (0.1%) eked out gains. The Russell 2000 ended the day where it began. Crude oil prices declined for the second straight session, down $1.10 to $76.48 per barrel. Ten-year Treasury yields moved little, remaining at 3.97%. The dollar rose minimally, while gold prices slid for the third session in a row.

Wall Street endured a poor day last Thursday, with stocks moving lower. The financial sector was hit particularly hard, although all of the major sectors ended the session in the red. Among the benchmark indexes listed here, the Russell 2000 fell the furthest, dropping 2.8%, followed by the Nasdaq (-2.1%), the S&P 500 (-1.9%), the Dow (-1.7%), and the Global Dow (-0.8%). Bond prices advanced, pulling yields lower, with 10-year Treasury yields dipping 5.1 basis points to close at 3.92%. Crude oil prices continued to drop, closing down about $1.12 to $75.54 per barrel. The dollar slipped lower, while gold prices advanced for the first time in several sessions.

Stocks fell for the fourth straight session last Friday. Each of the benchmark indexes listed here ended the day in the red, with the Russell 2000 (-3.0%) and the Nasdaq (-1.8%) falling the furthest. The S&P 500 slid 1.5%, the Global Dow dropped 1.3%, and the Dow lost 1.1%. Ten-year Treasury yields gave back 23.0 basis points to close at 3.69%. Crude oil prices gained $0.81 to hit $76.53 per barrel. The dollar dipped lower, while gold prices vaulted up $37.80 to $1,872.40 per ounce.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- There were 311,000 new jobs added in February, although the unemployment rate edged up 0.2 percentage point to 3.6%. The average monthly job gain over the past six months was 343,000. Last month, notable job gains occurred in leisure and hospitality, retail trade, government, and health care. Employment declined in information and in transportation and warehousing. The number of unemployed, at 5.9 million, edged up by 242,000 in February from the previous month. In February, the labor force participation rate was little changed at 62.5%, and the employment-population ratio held at 60.2%. These measures have shown little net change since early 2022 and remain below their pre-pandemic February 2020 levels (63.3% and 61.1%, respectively). In February, average hourly earnings rose $0.08 to $33.09. Over the past 12 months, average hourly earnings increased by 4.6%. The average workweek edged down by 0.1 hour to 34.5 hours in February.

- In January, there were 10.8 million job openings, a decrease of a little more than 400,000 from the December amount. The number of hires and total separations in January were little changed from their respective totals in December. In January, employees were less willing to voluntarily leave their jobs, while employers were more inclined to dismiss employees. The number of quits declined by about 200,000, while the number of layoffs and discharges increased by 241,000.

- According to the Bureau of Economic Analysis, the goods and services trade deficit was $68.3 billion in January, up $1.1 billion, or 1.6%, from the December deficit. January exports were $257.5 billion, $8.5 billion, or 3.4%, more than December exports. January imports were $325.8 billion, $9.6 billion, or 3.0%, more than December imports. Year over year, the goods and services deficit decreased $19.2 billion, or 21.9%, from January 2022.

- The international trade in goods deficit expanded by 2.0% in January over December. Exports of goods were $173.8 billion, 4.2% more than December exports. Imports of goods were $265.3 billion, 3.4% above the December total. The trade in goods deficit in January was 16.7% less than the deficit in January 2022.

- The government deficit jumped to $262.4 billion in February, $223.6 billion greater than the January deficit and $45.8 billion more than the February 2022 deficit. In February, government receipts were $262.1 billion ($447.3 billion in January), while government outlays were $524.5 billion ($486.1 billion in January). Through the first five months of the fiscal year, the total government deficit sits at $722.6 billion, $247.0 billion greater than the deficit over the same period in the previous fiscal year.

- The national average retail price for regular gasoline was $3.389 per gallon on March 6, $0.047 per gallon more than the prior week’s price, but $0.713 less than a year ago. Also, as of March 6, the East Coast price decreased $0.002 to $3.242 per gallon; the Gulf Coast price increased $0.067 to $2.979 per gallon; the Midwest price rose $0.095 to $3.265 per gallon; the Rocky Mountain price decreased $0.040 to $3.742 per gallon; and the West Coast price increased $0.091 to $4.341 per gallon. Residential heating oil prices averaged $4.243 per gallon on March 6, $0.013 above the previous week’s price, but $0.679 per gallon less than a year ago. According to the U.S. Energy Information Administration, in 2022, the United States exported 5.97 million barrels of petroleum product per day, an increase of 7.0% compared with 2021, setting a new record for total petroleum product exports.

- Both the number of new claims for unemployment insurance and the number of workers receiving insurance benefits increased sharply over the last reporting period. For the week ended March 4, there were 211,000 new claims for unemployment insurance, an increase of 21,000 from the previous week’s level. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended February 25 was 1.2%, an increase of 0.1 percentage point from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended February 25 was 1,718,000, an increase of 69,000 from the previous week’s level, which was revised down by 6,000. States and territories with the highest insured unemployment rates for the week ended February 18 were New Jersey (2.7%), Rhode Island (2.5%), Massachusetts (2.3%), Minnesota (2.3%), California (2.2%), Alaska (2.1%), Illinois (2.0%), Montana (2.0%), New York (1.9%), Connecticut (1.8%), Pennsylvania (1.8%), and Puerto Rico (1.8%). The largest increases in initial claims for unemployment insurance for the week ended February 25 were in Massachusetts (+4,438), Rhode Island (+1,210), New Jersey (+742), Arkansas (+619), and the District of Columbia (+494), while the largest decreases were in Kentucky (-6,164), California (-2,844), Texas (-1,426), Ohio (-1,274), and Michigan (-1,020).

Eye on the Week Ahead

The latest information on inflation is available this week with the February release of the Consumer Price Index, the Producer Price Index, and the retail sales report. Inflation rose in January after falling in the previous two months, setting up the likelihood that the Federal Reserve will initiate more interest-rate hikes over a longer period of time.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.