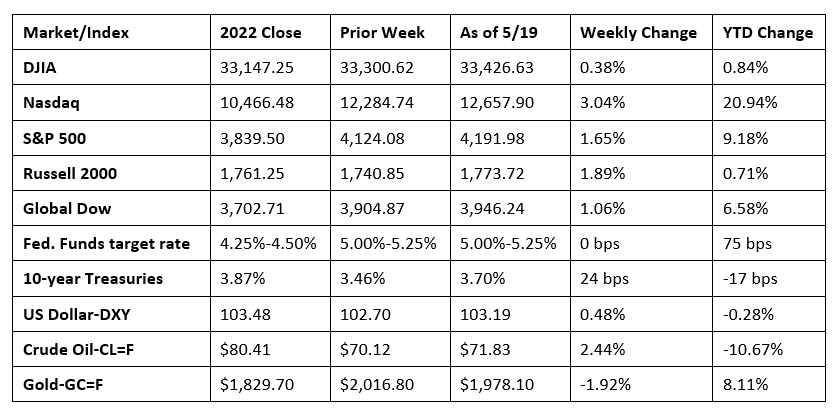

Most of last week, investors seemed to react to negotiations concerning the debt ceiling. Despite a lackluster ending to the week, stocks closed generally higher. Tech shares climbed nearly 4.0%, while consumer discretionary stocks also posted gains. Overall, each of the benchmark indexes listed here ended last week higher, led by the Nasdaq, followed by the Russell 2000, the S&P 500, the Global Dow, and the Dow. In fact, the Nasdaq and the S&P 500 had their best week since March. Ten-year Treasury yields added 24 basis points. The dollar advanced, while gold prices slid. Crude oil prices gained about $1.70.

A jump in tech shares pushed stocks higher last Monday, as investors continued to focus on debt ceiling negotiations at the White House. The small caps of the Russell 2000 outperformed the indexes listed here, climbing 1.2%. The Nasdaq rose 0.7%, followed by the Global Dow (0.5%), the S&P 500 (0.3%), and the Dow (0.1%). Crude oil prices gained 1.8% to $71.28 per barrel, as OPEC+ prepared to cut supplies. Ten-year Treasury yields added 4.5 basis points to reach 3.50%. The dollar slipped, while gold prices inched higher.

Stocks declined last Tuesday as investors worried about the lack of progress on debt ceiling negotiations. The Russell 2000 gave back Monday’s gains after tumbling 1.4%. The Dow dipped 1.0%, followed by the S&P 500 (-0.6%), the Global Dow (-0.5%), and the Nasdaq (-0.2%). Bond prices also slipped, pushing yields higher. Ten-year Treasury yields rose 4.1 basis points to 3.54%. Crude oil prices reversed the prior day’s uptick, falling 0.9% to $70.49 per barrel. The dollar gained, while gold prices fell 1.4% to close under $2,000.00 per ounce for the first time this month.

Wall Street rallied last Wednesday, fueled by optimism that an agreement could be reached on the debt ceiling. The small caps of the Russell 2000, which is sensitive to economic developments, jumped 2.2% by the close of trading. The Nasdaq rose 1.3%, followed by the Dow and the S&P 500, which advanced 1.2%. The Global Dow climbed 0.5%. Crude oil prices reached the highest price in over a week closing at $72.75 per barrel. The dollar advanced, while gold prices fell. Ten-year Treasury yields settled at 3.58%, an increase of 3.2 basis points.

Stocks rose for a second straight session last Thursday, as investors received more encouraging news on a potential debt ceiling deal. Tech shares advanced, helping to move the benchmark indexes higher. The Nasdaq gained 1.5%, followed by the S&P 500 (0.9%), the Russell 2000 (0.6%), the Global Dow (0.4%), and the Dow (0.3%). Ten-year Treasury yields rose to the highest level in two months after gaining 6.7 basis points to 3.64%. Crude oil prices fell back, dropping 1.2% to $71.98 per barrel. The dollar increased for the third straight session, while gold prices declined for the third consecutive day.

Last Friday, an abrupt halt to debt ceiling talks sent investors scurrying away from stocks. Of the benchmark indexes listed here, only the Global Dow (0.2%) advanced by the close of trading. The Russell 2000 declined 0.6%, while the Dow, the S&P 500, and the Nasdaq slipped between 0.1% and 0.3%. Ten-year Treasury yields added 5.7 basis points to close at 3.7%. The dollar dipped, while gold prices advanced. Crude oil prices moved little, closing at around $71.83 per barrel.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- Retail sales rose 0.4% in April after declining 0.7% in March. For the 12 months ended in April, retail sales have increased 1.6%. Several categories contributed to the April advance in retail sales including motor vehicle and parts dealers (0.4%), building material and garden equipment and supplies dealers (0.5%), health and personal care stores (0.9%), general merchandise stores (0.9%), miscellaneous store retailers (2.4%), nonstore (online) retailers (1.2%), and food services and drinking places (0.6%). Retailers that saw sales decrease include furniture and home furnishing stores (-0.7%), electronics and appliance stores (-0.5%), food and beverage stores (-0.2%), grocery stores (-0.4%), gasoline stations (-0.8%), clothing and clothing accessories stores (-0.3%), sporting goods, hobby, musical instrument, and book stores (-3.3%), and department stores (-1.1%).

- According to the latest data from the Federal Reserve, industrial production rose 0.5% in April following two consecutive flat months. In April, manufacturing increased 1.0%, bolstered by a strong gain in the output of motor vehicles and parts. Factory output, excluding motor vehicles and parts, moved up 0.4%.The index for mining rose 0.6%, while the index for utilities dropped 3.1%, as milder temperatures in April lowered demand for heating. Total industrial production in April was 0.2% above its year-earlier level.

- The number of building permits issued for residential housing construction declined 1.5% in April and was 21.1% below the April 2022 rate. However, building permits issued for single-family construction increased 3.1% last month. Housing starts rose 2.2%, while single-family housing starts advanced 1.6%. Housing completions fell 10.4% in April, while single-family housing completions were down 6.5%.

- Sales of existing homes fell 3.4% in April and were down 23.2% from April 2022. Total housing inventory sat at a 2.9-month supply. The median existing-home price in April was $388,800, 3.6% above the March price of $375,400 but 1.7% below the April 2022 price of $395,500. Single-family home sales also declined in April, falling 3.5% from March. The median existing single-family home price was $393,300 in April, 3.6% above the March price ($379,500) but 2.1% under the April 2022 price ($401,700).

- The national average retail price for regular gasoline was $3.536 per gallon on May 15, $0.003 per gallon higher than the prior week’s price but $0.955 less than a year ago. Also, as of May 15, the East Coast price decreased $0.030 to $3.397 per gallon; the Gulf Coast price rose $0.034 to $3.079 per gallon; the Midwest price increased $0.047 to $3.440 per gallon; the Rocky Mountain price declined $0.020 to $3.518 per gallon; and the West Coast price dipped $0.011 to $4.519 per gallon.

- For the week ended May 13, there were 242,000 new claims for unemployment insurance, a decrease of 22,000 from the previous week’s level. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended May 6 was 1.2%, unchanged from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended May 6 was 1,799,000, a decrease of 8,000 from the previous week’s level, which was revised down by 6,000. States and territories with the highest insured unemployment rates for the week ended April 29 were California (2.4%), New Jersey (2.2%), Massachusetts (2.0%), Alaska (1.7%), Illinois (1.6%), New York (1.6%), Oregon (1.6%), Rhode Island (1.6%), Minnesota (1.5%), Puerto Rico (1.5%), and Washington (1.5%). The largest increases in initial claims for unemployment insurance for the week ended May 6 were in Massachusetts (+6,420), Missouri (+2,596), California (+1,997), Texas (+1,707), and New York (+1,212), while the largest decreases were in Kentucky (-3,026), Colorado (-1,526), Georgia (-916), Wisconsin (-494), and New Hampshire (-428).

Eye on the Week Ahead

This is a busy week for important economic data. New single-family home sales figures for April are released this week. March saw sales increase 9.6% for the fifth straight month. The second estimate of first-quarter gross domestic product is out this week. The first estimate showed the economy accelerated at an annualized rate of 1.1%. The personal income and outlays report for April is also available this week. Data from the last report showed consumer spending was flat in March, while consumer prices for goods and services rose 0.3%.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.