In its annual Retirement Confidence Survey of current workers and retirees, the Employee Benefit Research Institute found that workers’ confidence in their ability to fund retirement fell by the largest extent since the financial crisis of 2008, to levels not seen since 2018. Retirees’ confidence also took a substantial hit. Overall, just 20% of respondents felt very confident they will be able to afford a comfortable retirement.

The percentage of workers who felt at least somewhat confident in their ability to afford retirement plummeted nine percentage points, from 73% in 2022 to just 64% in 2023. For retirees, the drop was four percentage points — from 77% in 2022 to 73% in 2023. Although retirees’ confidence remained higher than workers’ — a historical trend — just 27% of retirees were very confident, down from 33% last year and the lowest percentage since 2009.

The top two reasons workers gave for a lack of confidence were having little or no savings/being unprepared/can’t afford it (40% of respondents) and the rising cost of living/inflation (29%). Those reasons mirrored retiree responses, but in reverse order; 42% of retirees who lack confidence were concerned about inflation, while 25% said they had little or no savings, were unprepared, or unable to afford it.

Cost of living a major worry

Inflation was a recurring theme throughout this year’s report.

- 84% of workers and 67% of retirees were concerned that inflation will make it harder to save money.

- 73% of workers and 58% of retirees were worried that they will have to cut their spending substantially due to inflation.

- Nearly half of retirees said their overall spending is higher than expected, compared with just 36% in 2022.

- Just 58% of workers (down from 67% in 2022) believed they would have enough money to keep up with the rising cost of living in retirement.

In fact, inflation and the economy were the two most common concerns cited by both groups.

Percentage of workers and retirees who said they were at least somewhat concerned about the event affecting their finances in retirement. The survey was conducted in January and February 2023.

A perspective on income strategies

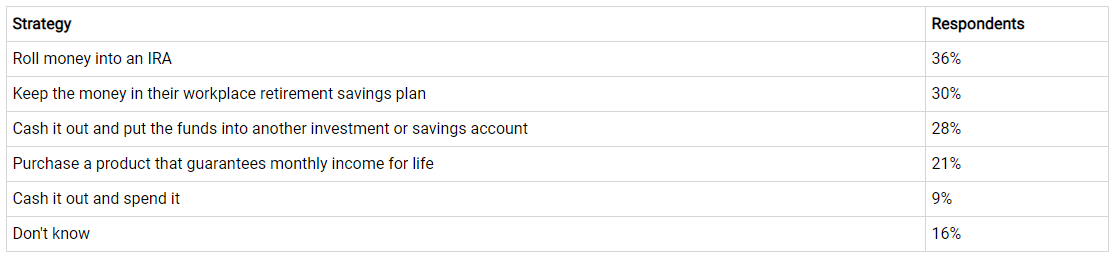

When asked what they intend to do with their workplace retirement savings plan money when they retire, workers gave the following responses:

Younger workers were more likely than older workers to say they would cash out the plan and put the money into another investment or savings account or buy a guaranteed income product. Those with at least $100,000 were more likely than those with less than $10,000 to report that they would roll over the money to an IRA.

More workers seem to be seeking experienced guidance when it comes to managing their retirement strategies; 34% are currently working with a financial professional, up from 29% in 2022, and more than half expect to do so in the future, up from 45% in 2022.