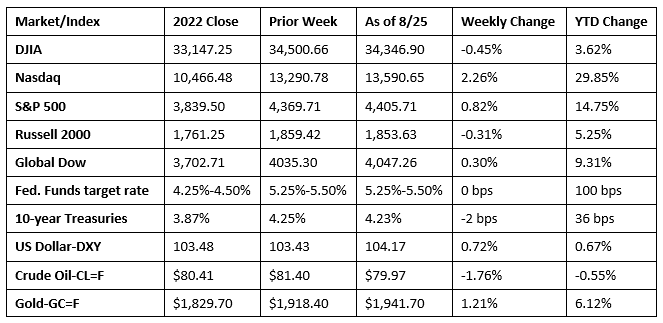

Last week saw Wall Street generally close with a mixed bag of results. The Nasdaq, the S&P 500, and the Global Dow ended the week higher, while the Dow and the Russell 2000 lost value. Investors tried to digest Federal Reserve Chair Jerome Powell’s comments from the annual Jackson Hole Economic Symposium last Friday. Powell indicated that, despite inflation coming down, prices remain too high. The central bank is prepared to hike interest rates further until inflation steadies at the Fed’s 2.0% target. Powell’s suggestion of more interest rate increases sent bond yields higher, with two-year Treasury yields rising to 5.07%. Among the market sectors, consumer discretionary and information technology gained 2.0%. Crude oil prices declined for the second straight week, while the dollar rose for the fourth consecutive week.

Stocks closed mixed to begin last week. The Dow (-0.1%) and the Russell 2000 (-0.2%) closed marginally lower, while the S&P 500 (0.7%) and the Global Dow (0.1%) closed higher. The Nasdaq ended a four-day losing streak after climbing 1.6%. Ten-year Treasury yields jumped to a 16-year high after settling at 4.34%. Information technology and consumer discretionary led the market sectors, while interest-rate sensitive sectors such as utilities and real estate fell. Crude oil prices slid 0.4% to close the day at around $80.90 per barrel. The dollar was flat, while gold prices edged up 0.4%.

Most of the benchmark indexes listed here closed lower last Tuesday, with the exception of the Nasdaq and the Global Dow, which eked out 0.1% gains. The Dow (-0.5%), the S&P 500 (-0.3%), and the Russell 2000 (-0.3%) slid lower. Yields on 10-year Treasuries slipped 1.4 basis points, but remained near the 16-year high at 4.32%. Crude oil prices declined 0.6%, settling at $80.25 per barrel. The dollar and gold prices advanced 0.3% and 0.2%, respectively.

Tech stocks rallied and bond yields fell last Wednesday. The Nasdaq led the benchmark indexes listed here, gaining 1.6%, followed by the S&P 500 (1.1%), the Russell 2000 (1.0%), the Global Dow (0.9%), and the Dow (0.5%). Ten-year Treasury yields fell 13.0 basis points to close at 4.19%. The dollar slipped lower, while gold prices rose 1.0%. Several large retailers saw their stock values fall on disappointing quarterly earnings. Nevertheless, each of the market sectors posted gains (with the exception of energy), led by information technology and communication services.

Wall Street saw stocks tumble lower last Thursday, with each of the benchmark indexes listed here losing value. The Nasdaq dropped 1.9% despite a major chip maker exceeding quarterly earnings predictions. Each of the S&P 500 market sectors declined, with information technology, consumer discretionary, and communication services dipping more than 2.0%. The S&P 500 fell 1.4%, followed by the Russell 2000 (-1.3%), the Dow (-1.1%), and the Global Dow (-0.7%). Long-term bond yields remained steady, gaining 3.1 basis points to settle at 4.23%. The dollar resumed its upward momentum, gaining 0.6%. Gold prices slipped 0.2%. Crude oil prices were flat on the day, settling at about $78.88 per barrel.

Stocks closed higher last Friday, despite hawkish comments from Fed Chair Jerome Powell. The Nasdaq reversed course from the prior day, closing up 0.9%, followed by the Dow and the S&P 500 (0.7%), while the Russell 2000 rose 0.4%. The Global Dow ticked lower (-0.1%). Ten-year Treasury yields were flat on the day. Crude oil prices bounced back from a slow week, gaining 1.2%. The dollar edged up 0.2%, while gold prices dipped 0.3%.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- Sales of existing homes declined 2.2% in July and 16.6% since July 2022. Once again, low inventory and high mortgage interest rates cooled the market for existing homes. Total housing inventory in July sat at a 3.3-month supply at the current sales pace. The median existing home price in July was $406,700, down from $410,000 in June, but up from $399,000 in July 2022. Sales of single-family existing homes fell 1.9% in July and 16.3% from July 2022. The supply of single-family existing homes in July was 3.2 months, up slightly from 3.1 months in June and unchanged from the supply in July 2022. The median existing single-family existing home price in July was $412,300, down from the June price of $415,700 but higher than the July 2022 price of $405,800.

- Unlike sales of existing homes, the market for new single-family homes accelerated in July. According to the latest report from the Census Bureau, sales of new single-family homes rose 4.4% last month and were 31.5% above the July 2022 estimate. Both the median sales price and the average sales price for new houses increased in July. The median sales price for new houses sold was $436,700 ($416,700 in June). The average sales price was $513,000 ($507,300 in June). The supply of new homes for sale stood at 7.3 months at the current sales pace, down slightly from the June supply of 7.5 months. Despite the July increases in the median and average sales prices, both are well below their respective values from a year ago. The median sales price is 9.5% under the July 2022 estimate, while the average sales price is down 10.1%.

- New orders for durable goods declined 5.2% in July, the first monthly decrease since February. Excluding transportation, new orders increased 0.5%. Excluding defense, new orders decreased 5.4%. Transportation equipment, also down following four consecutive monthly increases, drove the decrease, falling 14.3% last month.

- The national average retail price for regular gasoline was $3.868 per gallon on August 21, $0.018 per gallon higher than the prior week’s price but $0.012 less than a year ago. Also, as of August 21, the East Coast price increased $0.017 to $3.728 per gallon; the Midwest price fell $0.048 to $3.720 per gallon; the Gulf Coast price rose $0.043 to $3.458 per gallon; the Rocky Mountain price climbed $0.085 to $4.039 per gallon; and the West Coast price advanced $0.107 to $4.866 per gallon. According to the U.S. Energy Information Administration, unplanned refinery outages and lower gasoline production capacity are increasing the costs of producing summer-grade gasoline in the United States this summer.

- For the week ended August 19, there were 230,000 new claims for unemployment insurance, a decrease of 10,000 from the previous week’s level, which was revised up by 1,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended August 12 was 1.1%, a decrease of 0.1% from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended August 12 was 1,702,000, a decrease of 9,000 from the previous week’s level, which was revised down by 5,000. States and territories with the highest insured unemployment rates for the week ended August 5 were New Jersey (2.5%), Puerto Rico (2.4%), California (2.2%), Rhode Island (2.1%), Massachusetts (2.0%), New York (1.9%), Oregon (1.9%), Connecticut (1.8%), Pennsylvania (1.8%), and Minnesota (1.7%). The largest increases in initial claims for unemployment insurance for the week ended August 12 were in Virginia (+940), Iowa (+860), Illinois (+769), Hawaii (+664), and Arkansas (+388), while the largest decreases were in California (-3,959), Texas (-1,641), Pennsylvania (-1,155), Michigan (-1,129), and New York (-963).

Eye on the Week Ahead

The last week of August includes many important economic reports. The second estimate for the second-quarter gross domestic product is out this week. The initial estimate showed the economy expanded at an annualized rate of 2.4% over the first quarter. The report on personal income and expenditures for July is available this week. Investors should pay particular attention to the personal consumption expenditures price index, a measure of inflation favored by the Federal Reserve. Finally, the week ends with the July employment figures. Job growth expanded in June, but at a much slower pace compared to the monthly average for 2023.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.