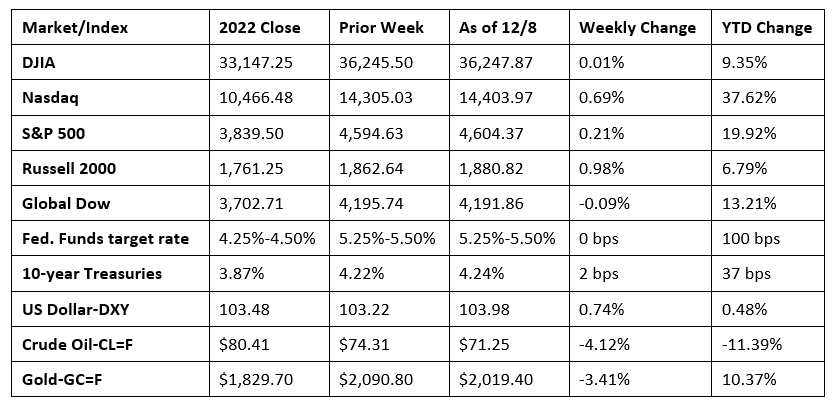

The first week of December saw stocks close higher. Megacaps fueled much of the increase. A better-than-expected jobs report (see below) encouraged investor sentiment about a soft landing for the economy, while cooling expectations of an early cut in interest rates by the Federal Reserve. Each of the benchmark indexes listed here ended last week higher, with the exception of the Global Dow. Several market sectors advanced, led by consumer discretionary, real estate, industrials, communication services, and information technology. Energy, consumer staples, and materials lagged. Ten-year Treasury yields rode a wave of ebbs and flows during the week, ultimately closing about where they began. A late-week rally wasn’t enough to keep crude oil prices from falling for the sixth straight week. The dollar edged higher, while gold prices declined.

Wall Street began last week on a bit of a sour note. Megacaps retreated, dragging the Nasdaq down 0.8%. The S&P 500 fell 0.5%, the Global Dow lost 0.2%, and the Dow slipped 0.1%. The small caps of the Russell 2000 gained 1.0%. Communication services, information technology, and energy were the worst performing sectors. Ten-year Treasury yields rose 6.2 basis points to 4.28% as bond prices dipped. Crude oil prices fell nearly 1.0% to $73.34 per barrel. The dollar advanced, while gold prices declined.

Tech stocks helped boost the Nasdaq last Tuesday, while long-term bonds resumed their rally. Of the benchmark indexes listed here, only the Nasdaq closed higher, gaining 0.3%. The Russell 2000 (-1.4%), the Global Dow (-0.3%), the Dow (-0.2%), and the S&P 500 (-0.1%) ended the session lower. Ten-year Treasury yields shed 11.7 basis points, closing at 4.16%. Crude oil prices continued to tumble after falling 0.9% to close at $72.37 per barrel. The dollar gained 0.3%, while gold prices fell 0.2%.

Stocks tumbled lower for the third straight session last Wednesday. The Nasdaq (-0.6%) and the S&P 500 (-0.4%) declined the furthest among the benchmark indexes listed here, followed by the Dow and the Russell 2000, which dipped 0.2%. The Global Dow edged up 0.2%. Crude oil prices declined to the lowest levels since June after dropping 4.2% to $69.26 per barrel. Yields on 10-year Treasuries lost 5.0 basis points to close at 4.12%. The dollar ticked up for the second straight session, while gold prices advanced for the first time after falling three straight days.

Megacaps fueled a rebound in the markets last Thursday, with investors favoring artificial intelligence stocks. The Nasdaq closed up 1.4%, followed by the Russell 2000 (0.9%) and the S&P 500 (0.8%), while the Global Dow and the Dow gained 0.2%. Ten-year Treasury yields closed where they began at 4.12%. Crude oil prices inched up about $0.40 to $69.66 per barrel. Both the dollar and gold prices slid lower.

Stocks closed higher last Friday with the small caps of the Russell 2000 leading the way after gaining 0.8%. The Nasdaq rose 0.5%, while the Dow and the S&P 500 advanced 0.4%. The Global Dow ticked up 0.1%. Crude oil prices were boosted by a minor rally, gaining about 2.7% to close above $71.00 per barrel. Ten-year treasury yields jumped 11.6 basis points, closing at 4.24%. The dollar gained 0.4%, while gold prices fell 1.4%.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- According to the latest jobs report from the Bureau of Labor Statistics, there were 199,000 new jobs added in November, up from 150,000 new jobs added in October. Nevertheless, employment growth was below the average monthly gain of 240,000 over the prior 12 months but is in line with job growth in recent months. Job gains occurred in health care and government. Employment also increased in manufacturing, reflecting the return of workers from a strike. Employment in retail trade declined. The November unemployment rate edged down 0.2 percentage point to 3.7%. The total number of unemployed declined by 215,000 to 6.3 million. The employment-population ratio increased by 0.3 percentage point to 60.5% in November. The labor force participation rate was little changed at 62.8% and has been essentially flat since August. In November, average hourly earnings rose by $0.12, or 0.4%, to $34.10. Over the past 12 months, average hourly earnings have increased by 4.0%. The average workweek edged up by 0.1 hour to 34.4 hours in November. The change in employment for September was revised down by 35,000, from 297,000 to 262,000, while the change for October remained at 150,000. With these revisions, employment in September and October combined was 35,000 lower than previously reported.

- According to the latest Job Openings and Labor Turnover Summary, the number of job openings decreased 617,000 to 8.7 million in October. Over the month, job openings decreased in health care and social assistance (-236,000), finance and insurance (-168,000), and real estate and rental and leasing (-49,000). Job openings increased in information (+39,000). The number of hires dipped 18,000 to 5.9 million. The number of total separations was little changed in October from September. The October number of quits, layoffs, and discharges was relatively unchanged from the previous month.

- The latest report on international trade in goods and services was released on December 6 and is for October. The goods and services deficit was $64.3 billion, up 5.1% from the previous month. Exports fell 1.0%, while imports rose 0.2%. Year to date, the goods and services deficit decreased $161.4 billion, or 19.8%, from the same period in 2022. Exports increased $28.0 billion, or 1.1%. Imports decreased $133.4 billion, or 4.0%. The third quarter showed trade surpluses, in billions of dollars, with South and Central America ($21.8), Netherlands ($14.6), Australia ($8.3), Singapore ($6.8), Hong Kong ($6.6), Brazil ($4.8), Belgium ($3.3), United Kingdom ($3.1), Saudi Arabia ($2.0), and Switzerland ($1.6). Trade deficits, in billions of dollars, were reported with China ($63.8), Mexico ($39.1), European Union ($26.5), Vietnam ($26.2), Germany ($20.5), Japan ($14.9), Taiwan ($12.8), South Korea ($11.5), India ($11.5), Italy ($10.9), Canada ($10.0), Malaysia ($5.5), France ($4.2), Ireland ($4.1), and Israel ($2.2).

- Business activity in the services sector expanded marginally in November. The S&P Global US Services PMI Business Activity Index posted 50.8 in November, up from October’s 50.6. Survey respondents noted a minimal increase in new orders following a three-month decline as new business from abroad ticked up. Employment rose at the weakest pace in over a year. Costs to services providers eased to the slowest rate in over three years, largely attributable to waning inflation.

- The national average retail price for regular gasoline was $3.231 per gallon on December 4, $0.007 per gallon lower than the prior week’s price and $0.159 less than a year ago. Also, as of December 4, the East Coast price increased $0.051 to $3.206 per gallon; the Midwest price fell $0.040 to $2.991 per gallon; the Gulf Coast price rose $0.028 to $2.738 per gallon; the Rocky Mountain price dropped $0.091 to $3.015 per gallon; and the West Coast price decreased $0.111 to $4.252 per gallon.

- For the week ended December 2, there were 220,000 new claims for unemployment insurance, an increase of 1,000 from the previous week’s level, which was revised up by 1,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended November 25 was 1.2%, a decrease of 0.1 percentage point from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended November 25 was 1,861,000, a decrease of 64,000 from the previous week’s level, which was revised down by 2,000. States and territories with the highest insured unemployment rates for the week ended November 18 were New Jersey (2.1%), Alaska (2.0%), California (1.8%), Hawaii (1.7%), Puerto Rico (1.7%), Massachusetts (1.6%), New York (1.6%), Oregon (1.6%), Rhode Island (1.6%), Pennsylvania (1.5%), and Washington (1.5%).The largest increases in initial claims for unemployment insurance for the week ended November 25 were in Wisconsin (+1,750), Kansas (+1,194), Ohio (+1,130), Pennsylvania (+609), and Idaho (+525), while the largest decreases were in California (-14,223), Texas (-5,560), Oregon (-2,980), Florida (-2,234), and New York (-2,073).

Eye on the Week Ahead

There’s plenty of important data being released this week. The Federal Open Market Committee meets for the last time this year. The FOMC hasn’t increased interest rates since July, however they have left the door open for more rate hikes should inflation reverse course and accelerate. Speaking of inflation, several inflationary indicators are out this week. The Consumer Price Index for November is available. The CPI was unchanged in October and saw its annual rate drop from 3.7% to 3.2%. The Producer Price Index, also out this week, fell 0.5% in October.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.