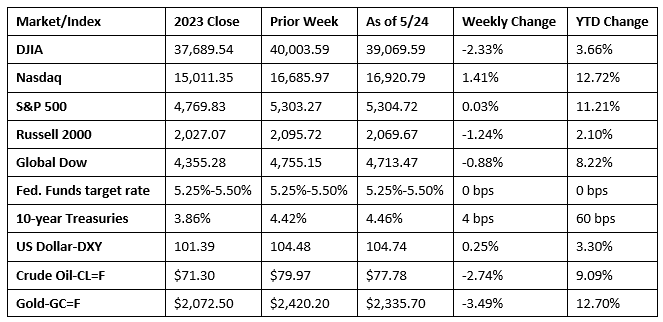

Tech shares, particularly AI stocks, helped push the Nasdaq, and to a much lesser extent, the S&P 500 higher last week. The Dow, the Russell 2000, and the Global Dow declined. During a week when volume was relatively light, investors latched onto favorable corporate earnings data from some major tech and AI companies. Among the market sectors, only information technology and communication services closed higher. Real estate and energy fell the furthest. Treasury yields inched higher, while crude oil prices fell 2.74%, yet remain up 9.1% year to date. Gold prices, which had been soaring, had their worst week in a while, although they are up nearly 13.0% from the beginning of the year.

Wall Street kicked off last week on a high note, with the Nasdaq securing a new record high. Each of the benchmark indexes listed here gained ground by the close of trading, with the exception of the Dow, which lost 0.5%. Technology led the market sectors, while consumer discretionary and energy fell the most. Ten-year Treasury yields inched up 1.7 basis points to close at 4.43%. Crude oil prices fell $0.35 to settle at about $79.71 per barrel. The dollar and gold prices advanced.

Stocks ended last Tuesday with mixed results. The Russell 2000 fell 0.2%, while the Global Dow was flat. However, the S&P 500 gained 0.3%, and both the Nasdaq and the Dow advanced 0.2%. The S&P 500 and the Nasdaq reached new record highs, while the Dow finished near its record level. Investors saw favorable earnings data from several retailers, while trying to gauge when the Fed might begin cutting interest rates. Yields on 10-year Treasuries dipped to 4.41%. Crude oil prices slid $0.75 to $79.08 per barrel. The dollar gained about 0.1%, while gold prices fell 0.5%.

The benchmark indexes listed here fell back last Wednesday. Investors awaited earnings data from a major AI company, while digesting the minutes from the last Federal Reserve meeting, in which some officials indicated a willingness to hike rates if necessary. The Russell 2000 fell the furthest (-0.8%), followed by the Dow and the Global Dow (-0.5%), the S&P 500 (-0.3%), and the Nasdaq (-0.2%). Ten-year Treasury yields rose 2.0 basis points to close at 4.43%. Crude oil prices declined for the third straight session after falling $1.32 to $77.34 per barrel. The dollar rose 0.3%, while gold prices dipped 1.8%.

The markets closed lower last Thursday as rising bond yields weighed on stocks. Once again, the Russell 2000 led the declines after falling 1.6%. The Dow lost 1.5%, the S&P 500 and the Global Dow dipped 0.7%, while the Nasdaq decreased 0.4%. Ten-year Treasury yields climbed to 4.47% after adding 4.1 basis points. Crude oil prices fell for the fourth straight day, losing $0.70 to settle at $76.87 per barrel. The dollar inched up 0.1%, while gold prices fell 2.5%.

Stocks closed higher ahead of the Memorial Day weekend. The Nasdaq (1.1%) reached a record high as AI stocks rallied. The Russell 2000 rose 1.0%, followed by the S&P 500 (0.7%), and the Global Dow (0.2%). The Dow ticked up less than 0.1%. Yields on 10-year Treasuries dipped to 4.46%. Crude oil prices rose for the first time in a week, gaining $0.91 to settle at $77.78 per barrel. The dollar and gold prices declined.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- April saw sales of existing homes decrease 1.9% from the prior month’s estimate. Existing home sales are down 1.9% from April 2023. Total inventory sits at a 3.5-month supply, up from 3.2 months in March. The median existing home price in April was $407,600 ($392,900 in March), an increase of 5.7% from the previous year ($385,800). Single-family home sales fell 2.1% in April and 1.3% from a year earlier. The median existing single-family home price was $412,100 in April, higher than the March price of $396,600, and up 5.6% from April 2023. According to Freddie Mac, the 30-year fixed-rate mortgage averaged 7.02% as of May 16. That’s down from 7.09% the previous week but up from 6.39% one year ago.

- Sales of new single-family houses in April were 4.7% below the March rate and 7.7% under the April 2023 estimate. The median price for new houses sold in April was $433,500 ($439,500 in March). The average sales price was $505,700 ($527,400 in March). The number of houses for sale in April represented a 9.1-month supply at the current sales pace.

- New orders for manufactured durable goods rose for the third straight month after increasing 0.7% in April. Since April 2023, new orders for durable goods have increased 0.5%. Excluding transportation, new orders increased 0.4%. Excluding defense, new orders were virtually unchanged. Transportation equipment, also up three consecutive months, led the increase, up 1.2%. Nondefense new orders for capital goods decreased 1.5% in April. New orders for defense capital goods increased 15.2%.

- The national average retail price for regular gasoline was $3.584 per gallon on May 20, $0.024 per gallon below the prior week’s price but $0.050 per gallon more than a year ago. Also, as of May 20, the East Coast price fell $0.016 to $3.475 per gallon; the Midwest price dipped $0.002 to $3.432 per gallon; the Gulf Coast price decreased $0.055 to $3.113 per gallon; the Rocky Mountain price increased $0.029 to $3.430 per gallon; and the West Coast price decreased $0.070 to $4.624 per gallon.

- For the week ended May 18, there were 215,000 new claims for unemployment insurance, a decrease of 8,000 from the previous week’s level, which was revised up by 1,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended May 11 was 1.2%, unchanged from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended May 11 was 1,794,000, an increase of 8,000 from the previous week’s level, which was revised down by 8,000. States and territories with the highest insured unemployment rates for the week ended May 4 were New Jersey (2.3%), California (2.2%), Rhode Island (1.7%), Massachusetts (1.6%), Nevada (1.6%), New York (1.6%), Washington (1.6%), Alaska (1.5%), Illinois (1.5%), Minnesota (1.5%), and Puerto Rico (1.5%). The largest increases in initial claims for unemployment insurance for the week ended May 11 were in Florida (+1,331), Pennsylvania (+924), Minnesota (+542), Louisiana (+537), and Massachusetts (+363), while the largest decreases were in New York (-9,543), Illinois (-2,567), California (-1,189), Indiana (-1,079), and Michigan (-513).

Eye on the Week Ahead

There are some important economic reports released during the holiday-shortened week. The second estimate of gross domestic product for the first quarter is out this week. The initial estimate showed economic growth slowed to an annual rate of 1.6%. Also available this week is the latest report on personal income and outlays. The previous report showed consumer spending rose 0.8% in March, while consumer prices advanced 0.3%.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.