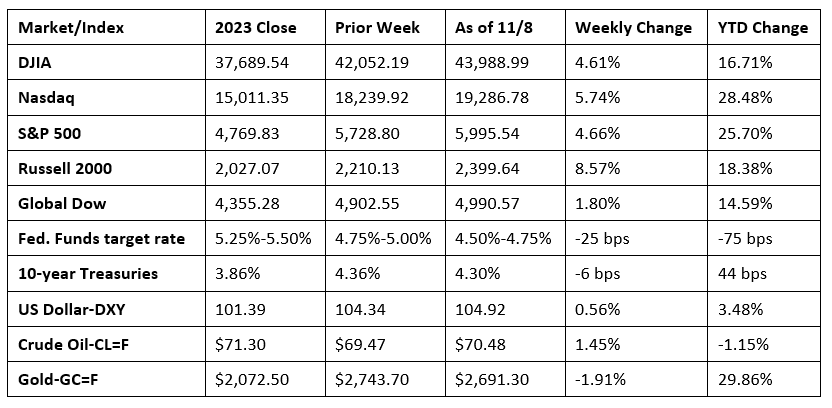

Investors had plenty to think about last week as they focused on the results of the presidential election and the Federal Reserve’s move to further reduce interest rates (see below). Each of the benchmark indexes listed here closed up by the end of the week, with consumer discretionary, information technology, and financials outperforming. Bond prices ended the week higher, pulling yields lower. Crude oil prices rose to over $72.00 per barrel only to slip back a bit at the end of the week. The dollar inched higher, while gold prices declined. According to Freddie Mac, mortgage rates rose to 6.79% on November 7, the highest they’ve been in nearly four months.

Last Monday saw stocks tumble as election uncertainty weighed on the markets. Of the benchmark indexes listed here, only the Russell 2000 (0.4%) posted a gain. The Dow lost 0.6%, the NASDAQ and the S&P 500 each fell 0.3%, and the Global Dow dipped 0.1%. Ten-year Treasury yields fell 5.2 basis points to close at 4.30%. Crude oil prices rose 3.2% to reach $71.69 per barrel. The dollar lost 0.4%, while gold prices slipped 0.1%.

Stocks rallied last Tuesday as investors awaited the results of the presidential election. The Russell 2000 led the benchmark indexes listed here, gaining 1.9%. The NASDAQ rose 1.4%, the S&P 500 gained 1.2%, the Dow advanced 1.0%, and the Global Dow climbed 0.9%. Ten-Year Treasury yields closed at 4.28%. Crude oil prices rose 1.0%, closing at $72.16 per barrel. The dollar slipped 0.4%, while gold prices advanced 0.2%.

Wall Street enjoyed a robust day following the presidential election. Investors showed optimism that a second Trump administration may favor businesses and boost economic growth. Each of the benchmark indexes jumped higher, led by the Russell 2000 (5.8%), followed by the Dow (3.6%), the NASDAQ (3.0%), the S&P 500 (2.5%), and the Global Dow (0.7%). Yields on 10-year Treasuries rose more than 13.0 basis points to 4.42%. The dollar index, at 105.14, reached its highest level in four months. Crude oil prices dipped 0.2%, settling at $71.84 per barrel. Gold prices fell nearly 3.0%.

Stocks closed mostly higher last Thursday, with the NASDAQ (1.5%), the S&P 500 (0.7%), and the Global Dow (0.7%) advancing, while the Russell 2000 fell 0.4%. The Dow was flat. The ten-year Treasury yield slid to 4.34%. Crude oil prices rose to $72.16 per barrel. The dollar fell 0.7%, while gold prices rose 1.4%.

The S&P 500 (0.4%) and the Dow (0.6%) closed at record highs last Friday, buoyed by the Fed’s latest interest rate cut. The Russell 2000 gained 0.7%, the NASDAQ rose 0.1%, while the Global Dow fell 0.5%. Ten-year Treasury yields continued to tumble, closing the session at 4.30%. Crude oil prices dipped 2.7%, gold prices lost 0.5%, while the dollar climbed 0.4%.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- By a unanimous vote, the Federal Open Market Committee (FOMC) decided to cut interest rates an additional 25.0 basis points. The federal funds target rate range is now 4.50%-4.75%. The Committee noted that economic activity has continued to expand at a solid pace, labor market conditions have generally eased, and the unemployment rate moved up but remained low. Inflation has progressed toward the Committee’s 2.0% objective but remained somewhat elevated. In sum, the Committee would be prepared to adjust its monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals of 2.0% inflation and maximum employment.

- The international trade in goods and services deficit was $84.4 billion in September, up $13.6 billion, or 19.2%, from $70.8 billion in August, revised. September exports were $267.9 billion, $3.2 billion, or 1.2%, less than August exports. September imports were $352.3 billion, $10.3 billion, or 3.0%, more than August imports. Year to date, the goods and services deficit increased $69.6 billion, or 11.8%, from the same period in 2023. Exports increased $84.7 billion, or 3.7%. Imports increased $154.4 billion, or 5.3%.

- The S&P Global US Services PMI® Business Activity Index registered 55.0 in October, down slightly from 55.2 in September. A reading of 50.0 or higher indicates growth, thus services activity expanded solidly last month but at a slightly slower pace than in September. The services sector has expanded in each of the past 21 months. New orders grew at a solid pace in October. However, firms continued to scale back staffing levels amid uncertainty over future demand.

- The national average retail price for regular gasoline was $3.069 per gallon on November 4, $0.028 per gallon below the prior week’s price and $0.327 per gallon less than a year ago. Also, as of November 4, the East Coast price declined $0.053 to $2.992 per gallon; the Midwest price increased $0.014 to $2.937 per gallon; the Gulf Coast price fell $0.027 to $2.619 per gallon; the Rocky Mountain price dipped $0.095 to $3.103 per gallon; and the West Coast price fell $0.028 to $3.945 per gallon.

- For the week ended November 2, there were 221,000 new claims for unemployment insurance, an increase of 3,000 from the previous week’s level, which was revised up by 2,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended October 26 was 1.2%, unchanged from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended October 26 was 1,892,000, an increase of 39,000 from the previous week’s level, which was revised down by 9,000. This is the highest level for insured unemployment since November 13, 2021, when it was 1,974,000. States and territories with the highest insured unemployment rates for the week ended October 19 were New Jersey (2.2%), California (1.9%), Puerto Rico (1.8%), Washington (1.7%), Nevada (1.6%), Rhode Island (1.6%), Massachusetts (1.5%), New York (1.5%), Alaska (1.4%), Illinois (1.4%), and Pennsylvania (1.4%). The largest increases in initial claims for unemployment insurance for the week ended October 26 were in New York (+1,983), Michigan (+1,722), Illinois (+1,066), Texas (+757), and Ohio (+706), while the largest decreases were in North Carolina (-2,859), Florida (-2,429), California (-1,876), Virginia (-824), and Washington (-698).

Eye on the Week Ahead

The latest inflation data for October is available this week with the release of the Consumer Price Index, the Producer Price Index, and the report on import and export prices. The CPI rose 0.2% in September but ticked down 0.1 percentage point to 2.4% year over year. Producer prices, on the other hand, were flat in September and up only 1.8% since September 2023.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.