With 83% of the companies in the S&P 500 reporting, 65% have exceeded the average revenue estimate and 75% have beaten the average earnings per share estimate, according to FactSet Research. Earnings growth for the S&P 500 for Q1 is 13.5% as of current reporting.

The market has moved higher since the end of the first quarter supported in part by the positive earnings releases. A rising denominator in the P/E multiple helps support stock prices. As always, there is plenty to worry about but for the time being Mr. Market has chosen to ignore increased federal debt, the potential for substantial interest rate increases, unfunded public pensions, domestic political turmoil, geopolitical risks, etc. There will be plenty of focus on some or all of these negatives at some unpredictable time in the future. For now, however, Mr. Market seems to be in the mood to party.

On The One Hand

- The decline in construction spending of 0.2% in March was more than offset by the revision in the February figure which increased to 1.8% from 0.8%.

- The Trade Balance narrowed in March to a deficit of $43.7 billion from a downwardly revised $43.8 billion deficit for February. The real news is trade is higher from year ago levels with exports up 7% and imports higher by 8.8%.

- Initial unemployment claims declined 19,000 to 238,000 for the week ending April 29. Continuing claims declined by 23,000 to 1.964 million, the lowest level for continuing claims since April 15, 2000.

- Nonfarm payrolls increased by 211,000 in April. Over the past three months, job gains have averaged 174,000 per month. The April unemployment rate was 4.4%.

- The ISM Non-Manufacturing Index rose from 55.2 in March to 57.5 in April, coming in above the consensus expected 55.8.

On The Other Hand

- The ISM Manufacturing Index for April was 54.8, down from 57.2 in March.

- Personal Income increased 0.2% in March and the February figure was revised downward to 0.3% from 0.4%. The Spending Report for March was unchanged for the second month in a row. The PCE Price Index declined 0.2% in March and was up just 1.6% year-over-year.

- U.S. light vehicle sales were at a seasonally adjusted annual rate of 16.88 million units in April versus a 16.62 million units for March. The April run rate was three percent below the 17.40 million units for April 2016.

- Productivity declined at an annual rate of 0.6% in the first quarter on the heels of an upwardly revised 1.8% increase. Unit labor costs were up three percent in the first quarter and fourth quarter productivity was revised downward by 0.4% to an increase of 1.3%.

All Else Being Equal

First Trust summarized last week’s Fed meetings well. “The most important part of today’s statement from the Federal Reserve is that it thinks the slow economic growth in the first quarter is temporary. As a result, the market consensus on the odds of a rate hike by June rose to about 94% after the meeting from about 67% beforehand.

The Fed made other relatively minor changes to its statement, but nothing that should change anyone’s impression of where the Fed is headed. The Fed noted slower consumer spending recently, but said the “fundamentals” supporting consumer spending “remained solid.” No one dissented from the statement, which suggests that even the “doves” are on board with further rate hikes.”

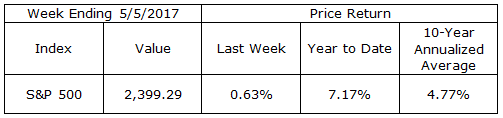

Last Week’s Market

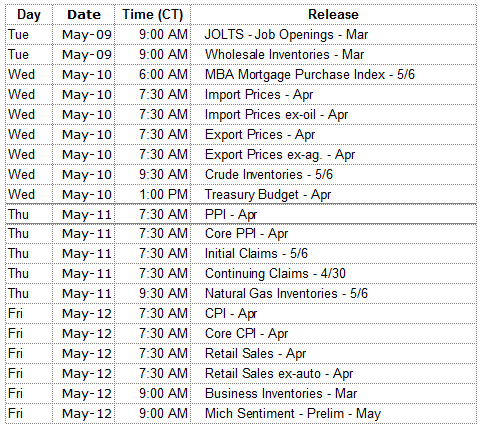

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.