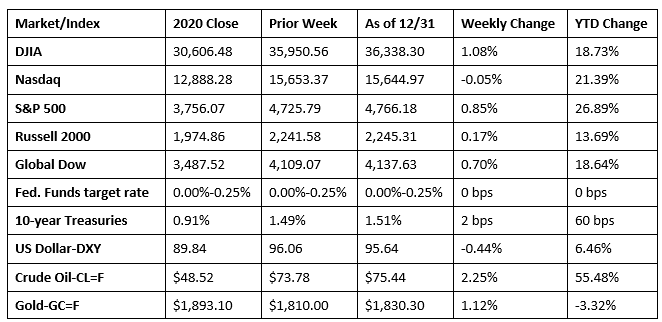

The last week of 2021 saw stocks close generally higher, with only the Nasdaq slipping lower. The Dow ended the week up 1.1%, followed by the S&P 500, the Global Dow, and the Russell 2000. The week between Christmas and New Year’s Day is generally marked by thin trading, and last week was no exception. Most of the market sectors closed the week in the black, led by real estate, utilities, materials, and consumer staples. Ten-year Treasury yields inched higher, crude oil prices rose $1.66 per barrel, while the dollar dipped lower.

Wall Street closed higher for a fourth day last Monday as investors weighed the prospects of a year-end rally against rising COVID cases. The S&P 500 gained 1.4% to mark its 69th record close of 2021. The Nasdaq also rose 1.4% as tech stocks continued to advance higher. The Dow rose 1.0%, the Russell 2000 climbed 0.9%, and the Global Dow added 0.6%. Ten-year Treasury yields slid, while crude oil prices and the dollar advanced. All of the market sectors moved higher, led by energy, real estate, and information technology.

Stocks ended last Tuesday mixed, with only the Global Dow and the Dow gaining 0.3% by the close of trading. The Russell 2000 fell 0.7%, the Nasdaq dropped 0.6%, and the S&P 500 slipped 0.1%. Crude oil prices and the dollar advanced marginally, while 10-year Treasury yields were unchanged at 1.48%. Utilities and consumer staples led the market sectors, while information technology and communication services declined.

The Dow and the S&P 500 each climbed to record highs last Wednesday, while tech shares dragged the Nasdaq marginally lower. Wednesday’s record close for the S&P 500 was the 70th of the year for that index. In what was a day of low trading volume, the Russell 2000 and the Global Dow also posted minimal gains. Bond prices dipped, sending yields higher, with 10-year Treasuries jumping 4.2%. Crude oil prices rose to $76.50 per barrel, while the U.S. Dollar Index slipped to 95.91.

Wall Street’s winning streak ended last Thursday, as each of the benchmark indexes closed in the red. The S&P 500 and the Dow lost 0.3%. The Nasdaq and the Global Dow fell 0.2%, while the Russell 2000 was unchanged. Crude oil prices and 10-year Treasuries slipped, while the dollar inched higher. Among the market sectors, only utilities, real estate, health care, and communication services closed higher. Energy and information technology fell 0.7%.

Stocks closed the week and the year with mixed returns. The Dow, the S&P 500, and the Nasdaq, fell last Friday, while the Russell 2000 and the Global Dow inched higher. The market sectors were also mixed last Friday, with consumer staples, energy, industrials, materials, real estate, and utilities posting gains, while the remaining sectors slid. Ten-year Treasury yields, crude oil prices, and the dollar dipped lower.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The international trade in goods deficit expanded by $14.6 billion, or 17.5%, in November. Exports of goods for November were $154.7 billion, $3.3 billion less than October exports. Imports of goods for November were $252.4 billion, $11.3 billion more than October imports.

- The national average retail price for regular gasoline was $3.275 per gallon on December 27, $0.020 per gallon less than the prior week’s price but $1.032 higher than a year ago. Gasoline production increased during the week ended December 24, averaging 10.1 million barrels per day. U.S. crude oil refinery inputs averaged 15.7 million barrels per day during the week ended December 24 — 115,000 barrels per day less than the previous week’s average. Refineries operated at 89.7% of their operable capacity, 0.2 percentage point below the prior week’s rate of capacity.

- For the week ended December 25, there were 198,000 new claims for unemployment insurance, a decrease of 8,000 from the previous week’s level, which was revised up by 1,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended December 18 was 1.3%, a decrease of 0.1 percentage point from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended December 18 was 1,716,000, a decrease of 140,000 from the prior week’s level, which was revised down by 3,000. This is the lowest level for insured unemployment since March 7, 2020, when it was 1,715,000. During the last week of February 2020 (pre-pandemic), there were 219,000 initial claims for unemployment insurance, and the number of those receiving unemployment insurance benefits was 1,724,000. States and territories with the highest insured unemployment rates for the week ended December 11 were Alaska (3.1%), California (2.7%), Puerto Rico (2.7%), the Virgin Islands (2.5%), New Jersey (2.4%), Illinois (2.3%), Minnesota (2.3%), Hawaii (2.0%), Massachusetts (1.8%), and Nevada (1.8%). The largest increases in initial claims for the week ended December 18 were in Oklahoma (+947), Michigan (+841), Washington (+803), Alabama (+732), and Arkansas (+731), while the largest decreases were in Missouri (-5,549), Pennsylvania (-4,520), Kentucky (-1,915), Georgia (-1,699), and Illinois (-1,321).

Eye on the Week Ahead

There is plenty of important economic data available this week, beginning with the purchasing managers’ manufacturing survey. The manufacturing sector gained traction for much of 2021, only to be sidetracked somewhat by labor shortages and supply chain constrictions. The week ends with the December jobs report. Employment rose by 210,000 in November, well below the monthly average of 550,000.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.