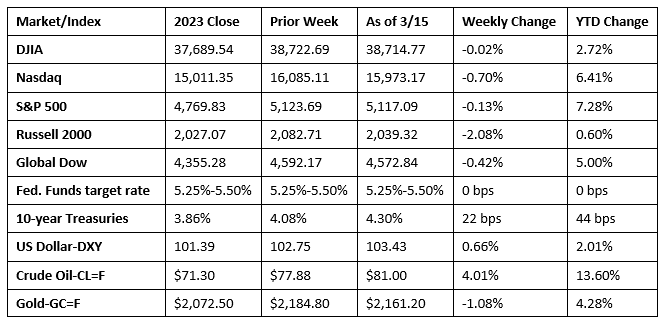

Equities closed lower for the second straight week, with the Russell 2000 losing nearly 2.0%. A sell-off in tech shares pulled the Nasdaq down 0.7%, marking the first back-to-back weekly losses since last October. Higher-than-expected inflation data may have raised investor concerns that the Federal Reserve may keep interest rates elevated for longer than hoped for. Information technology, consumer discretionary, health care, industrials, real estate, and utilities underperformed, while energy jumped more than 4.0%. Long-term bond prices slipped, driving yields higher. The dollar ended the week higher. Crude oil prices rose 4.0%. Gold prices declined, ending a three-week rally.

Stocks mostly slipped lower to start the week, with only the Dow inching up 0.1%, as investors may have exercised caution ahead of the upcoming Consumer Price Index report. The Russell 2000 (-0.8%), the Nasdaq (-0.4%), the Global Dow (-0.4%), and the S&P 500 (-0.1%) lost value last Monday. Ten-year Treasury yields gained 1.5 basis points to close at 4.10%. Crude oil prices ticked up 0.1% to reach $78.09 per barrel. The dollar and gold prices rose 0.1%.

Wall Street saw stocks edge higher last Tuesday, despite a slight bump in the February Consumer Price Index (see below). The Nasdaq (1.5%) and the S&P 500 (1.1%) led the benchmark indexes listed here, followed by the Dow (0.6%) and the Global Dow (0.5%). The Russell 2000 declined less than 0.1%. The expected increase in prices did not dampen investors’ expectations that the Federal Reserve will cut rates, possibly in June. Tech and AI shares resumed their recent rally, helping to push stocks higher. Ten-year Treasury yields closed at 4.15% after adding 5.1 basis points. Crude oil prices slipped $0.19 to $77.74 per barrel as Houthi forces stepped up Red Sea attacks. The dollar inched up 0.1%, while gold prices fell for the first time in several sessions, declining 1.2%.

The Russell 2000 (0.3%), the Global Dow (0.2%), and the Dow (0.1%) advanced last Wednesday, while the Nasdaq (-0.5%) and the S&P 500 (-0.2%) declined, as the tech rally slowed. Yields on 10-year Treasuries gained 3.7 basis points to close at 4.19%. Crude oil prices rose to $79.73 per barrel after increasing $2.17. The dollar dipped 0.1%, while gold prices rose 0.5%.

Stocks closed lower last Thursday, likely in response to another batch of higher-than-expected inflation data. Ten-year Treasury yields also jumped 10.6 basis points to 4.29% as bond prices slid lower. Crude oil prices reached a four-month high after hitting $80.08 per barrel. The dollar advanced 0.6%, while gold prices fell 0.7%. Each of the benchmark indexes listed here lost value, led by the Russell 2000, which fell 2.0%. The Global Dow declined 0.5%, the Dow lost 0.4%, while the Nasdaq and the S&P 500 dipped 0.3%.

Friday saw stocks fall, with the Nasdaq (-1.0%) and the S&P 500 (-0.7%) dropping the furthest among the benchmark indexes listed here. The Dow lost 0.5% and the Global Dow dipped 0.3%. The Russell 2000 rose 0.4%. Ten-year Treasury yields ticked up less than 1.0 basis point. Crude oil prices followed two days of advances by slipping 0.3%. The dollar inched up 0.1%, while gold prices fell 0.3%.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- Inflation rose for the second straight month in February. The Consumer Price Index increased 0.4% last month after rising 0.3% in January. Over the last 12 months, the CPI increased 3.2%. Prices for shelter rose 0.4% in February and prices for gasoline increased 3.8%. Combined, these two indexes contributed over 60.0% of the monthly increase. Prices for food were unchanged in February. Energy prices rose 2.3%, while prices less food and energy advanced 0.4%. Over the last 12 months, prices for food rose 2.2% while energy prices decreased 1.9%. Prices less food and energy increased 3.8% since February 2023. Shelter prices increased 5.7% over the last year, accounting for roughly two thirds of the total 12-month increase in prices less food and energy. Other indexes with notable increases over the last year include motor vehicle insurance (20.6%), medical care (1.4%), recreation (2.1%), and personal care (4.2%).

- The Producer Price Index rose a higher-than-expected 0.6% in February, following a 0.3% increase in January. Excluding prices for food and energy, producer prices rose 0.3% in February. For the 12 months ended in February, the PPI advanced 1.6%, the largest increase since the 12-month period ended in September 2023. In February, nearly two thirds of the rise in producer prices could be traced to prices for goods, which advanced 1.2%. Prices for services moved up 0.3%. The increase in producer prices is in line with the Consumer Price Index, which showed price pressures have held firmer than expected.

- Retail and food services sales rose 0.6% last month and 1.5% over the February 2023 rate. Retail trade sales increased 0.6% in February and 0.8% above last year. Nonstore (internet) retail sales dipped 0.1% in February but were up 6.4% over the last 12 months.

- Prices for both imports and exports advanced in February. Import prices rose 0.3% last month after rising 0.8% in January. Despite the recent increases, import prices decreased 0.8% over the past 12 months. Import fuel prices rose 1.8% in February, while nonfuel import prices ticked up 0.2%. Export prices increased 0.8% in February after rising 0.9% in January. Nevertheless, since February 2023, export prices have fallen 1.8%, which was the smallest 12-month decrease since the 12-month period ended in February 2023.

- The Treasury budget deficit was $296.0 billion in February, up from $22.0 billion in January. Total receipts were $271.0 billion, while outlays were $567.0 billion. Through the first five months of the fiscal year, the deficit is $828.0 billion, about $100.0 billion above the deficit over the same period for the last fiscal year.

- Industrial production edged up 0.1% in February after declining 0.5% in January. In February, manufacturing rose 0.8% after declining 1.1% in January. Mining climbed 2.2%. The gains in manufacturing and mining partly reflected recoveries from weather-related declines in January. Utilities fell 7.5% in February because of warmer-than-typical temperatures. Total industrial production in February was 0.2% below its year-earlier level.

- The national average retail price for regular gasoline was $3.376 per gallon on March 11, $0.026 per gallon more than the prior week’s price but $0.080 per gallon less than a year ago. Also, as of March 11, the East Coast price increased $0.025 to $3.265 per gallon; the Midwest price rose $0.018 to $3.287 per gallon; the Gulf Coast price fell $0.004 to $2.945 per gallon; the Rocky Mountain price rose $0.063 to $3.077 per gallon; and the West Coast price increased $0.067 to $4.296 per gallon.

- For the week ended March 9, there were 209,000 new claims for unemployment insurance, a decrease of 1,000 from the previous week’s level, which was revised down by 7,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended March 2 was 1.2%, unchanged from the previous week’s rate, which was revised down by 0.1%. The advance number of those receiving unemployment insurance benefits during the week ended March 2 was 1,811,000, an increase of 17,000 from the previous week’s level, which was revised down by 112,000. States and territories with the highest insured unemployment rates for the week ended February 24 were Rhode Island (3.1%), New Jersey (2.9%), Massachusetts (2.6%), California (2.4%), Minnesota (2.4%), Illinois (2.2%), New York (2.2%), Connecticut (2.1%), Montana (2.0%), and Pennsylvania (2.0%). The largest increases in initial claims for unemployment insurance for the week ended February 24 were in New York (+14,176), California (+5,549), Texas (+2,102), Michigan (+979), and Florida (+783), while the largest decreases were in Massachusetts (-3,894), Rhode Island (-1,955), Oregon (-1,063), Georgia (-882), and Tennessee (-335).

Eye on the Week Ahead

The Federal Open Market Committee meets this week. It is not expected that the Committee will lower interest rates at this time, however, it may give some more discernible indication as to when rates may be decreased. The FOMC does not meet again until the beginning of May.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.