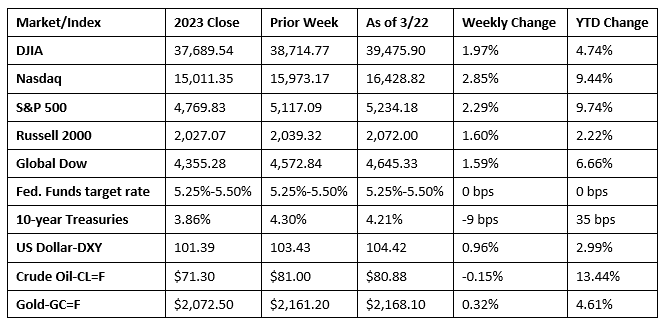

Despite a dip last Friday, stocks closed out last week higher. The S&P 500 recorded its biggest weekly percentage gain of the year, while the Dow and the Nasdaq hit record highs. Investors gained a bit of encouragement after the Federal Reserve maintained projections for three interest rate cuts by year’s end. Each of the market sectors moved higher last week, with communication services and industrials gaining 3.9% and 3.5%, respectively. Both the dollar and gold prices advanced. Crude oil prices declined for the week, influenced by a rising dollar (since oil is priced in dollars, if the dollar goes up, oil prices generally go down, because you need fewer dollars to buy that oil).

Wall Street got off to a good start last week, led by tech and AI stocks. The Nasdaq rose 0.8%, followed by the S&P 500 (0.6%), the Global Dow (0.3%), and the Dow (0.2%). The small caps of the Russell 2000 fell 0.7%. Yields on 10-year Treasuries rose 3.6 basis points to 4.34%. Crude oil prices jumped $1.87 to settle at about $82.91 per barrel, the highest level since October. Reduced crude exports from Iraq and Saudi Arabia, along with rising demand, helped drive crude oil prices higher. The dollar and gold prices inched up 0.2% and 0.1%, respectively.

Stocks advanced for a second straight session last Tuesday as investors awaited the results of the Federal Reserve meeting. While it is widely anticipated that the Fed will maintain interest rates at their current level, attention will be focused on the projected frequency and timing of potential rate cuts. The Dow (0.8%) led the benchmark indexes, followed by the S&P 500 (0.6%), the Russell 2000 (0.5%), the Nasdaq (0.4%), and the Global Dow (0.3%). Ten-year Treasury yields settled at 4.29% after falling 4.3 basis points. Crude oil prices continued to surge, rising $0.75 to $83.47 per barrel. The dollar rose 0.2%, while gold prices dipped 0.2%.

Wall Street rallied last Wednesday as investors were cautiously encouraged by the Federal Reserve’s projections of three interest rate cuts this year. The Russell 2000 advanced 1.9%, the Nasdaq rose 1.3%, the Dow climbed 1.0%, the S&P 500 gained 0.9%, and the Global Dow increased 0.7%. Ten-year Treasury yields dipped 2.4 basis points, settling at 4.27%. Crude oil prices saw the end to a rally as prices fell $1.63 to $81.84 per barrel. The dollar fell 0.4%, while gold prices rose 1.4%.

Stocks continued to climb higher last Thursday, with each of the benchmark indexes listed here advancing. The Russell 2000 led the charge for the second straight session after increasing 1.1%, followed by the Global Dow (0.8%), the Dow (0.7%), the S&P 500 (0.3%), and the Nasdaq (0.2%). Ten-year Treasury yields moved minimally, closing at 4.27%. Crude oil prices dipped for the second consecutive day, settling at $80.90 per barrel. The dollar rose 0.6%, while gold prices rose 1.1%.

Equities closed generally lower last Friday, with only the Nasdaq finishing the session up after gaining 0.2% to reach a record high. The Russell 2000 lost 1.3%, followed by the Dow (-0.8%), the Global Dow (-0.3%), and the S&P 500 (-0.1%). Crude oil prices fell for the third straight session, dipping 0.31%. Ten-year Treasury yields fell 5.3 basis points to 4.21%. The dollar advanced 0.4%, while gold prices were flat

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The Federal Open Market Committee maintained the target range for the federal funds rate at 5.25%-5.50%, as expected. In its statement, the FOMC indicated that, “The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2.0%.” During his press conference following the meeting, Fed Chair Jerome Powell noted that an interest rate cut is not on the immediate horizon. As to the increase in prices over the past few months, Powell said that the Committee anticipated that the path of lowering inflation may be bumpy. However, the FOMC is looking at the performance of inflation over time, not just a few months. The Fed retained its forecast for three rate cuts this year.

- February saw sales of existing homes jump 9.5%, although sales declined 3.3% year over year. Additional supply and consistent demand have helped drive sales throughout the country. Unsold inventory sat at a 2.9-month supply in February, down from 3.0 months in January. The median existing-home sales price was $384,500 in February, up from $378,600 in January, and well above the February 2023 price of $363,600. Existing single-family home sales also grew in February, up 10.3% but down 2.7% from a year earlier. The median price for existing single-family homes was $388,700, higher than the January price of $382,900, and over the February 2023 price of $368,100.

- The number of residential building permits issued in February was 1.9% above the January rate. The number of single-family building permits issued in February increased 1.0%. The number of housing starts in February rose 10.7% above the January estimate, while single-family housing starts increased 11.6%. Housing completions in February rose 19.7% over January. Single-family housing completions advanced 20.2% last month.

- The national average retail price for regular gasoline was $3.453 per gallon on March 18, $0.077 per gallon more than the prior week’s price and $0.031 per gallon more than a year ago. Also, as of March 18, the East Coast price increased $0.084 to $3.349 per gallon; the Midwest price rose $0.022 to $3.309 per gallon; the Gulf Coast price increased $0.154 to $3.099 per gallon; the Rocky Mountain price rose $0.089 to $3.166 per gallon; and the West Coast price increased $0.084 to $4.380 per gallon.

- For the week ended March 16, there were 210,000 new claims for unemployment insurance, a decrease of 2,000 from the previous week’s level, which was revised up by 3,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended March 9 was 1.2%, unchanged from the previous week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended March 9 was 1,807,000, an increase of 4,000 from the previous week’s level, which was revised down by 8,000. States and territories with the highest insured unemployment rates for the week ended March 2 were New Jersey (2.9%), Rhode Island (2.7%), California (2.5%), Minnesota (2.5%), Massachusetts (2.4%), Illinois (2.2%), Montana (2.0%), New York (2.0%), Pennsylvania (2.0%), Alaska (1.9%), Connecticut (1.9%), and Washington (1.9%). The largest increases in initial claims for unemployment insurance for the week ended March 9 were in Oregon (+2,216), California (+462), Indiana (+427), Texas (+392), and Nevada (+342), while the largest decreases were in New York (-14,583), Ohio (-1,453), New Hampshire (-446), Massachusetts (-305), and Vermont (-289).

Eye on the Week Ahead

The last week of March brings with it the final estimate of gross domestic product for the fourth quarter of 2023. According to the second estimate, the economy accelerated at an annualized rate of 3.2%. Also out this week is the February report on personal income and expenditures, which includes the personal consumption expenditures price index, the preferred inflation indicator of the Federal Reserve. With other indicators, such as the Consumer Price Index, showing that inflation rose in February, it is expected the PCE price index will also show in increase consumer prices.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.