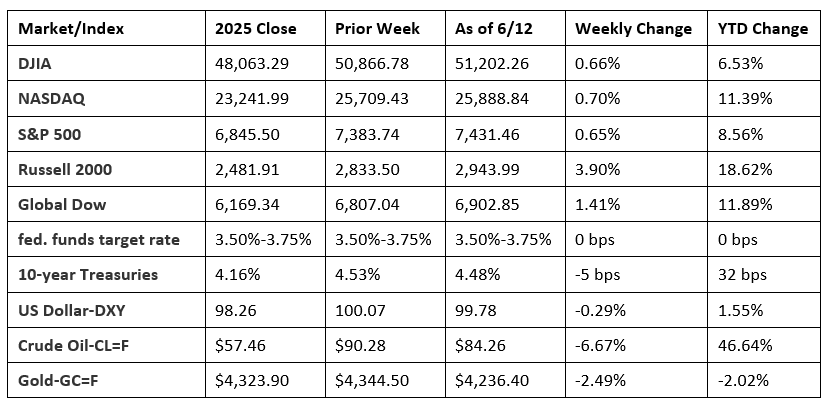

Wall Street began last week with a heavy sell-off as investors appeared anxious about the U.S.-Iran war, elevated inflation, and fears of a potential tech correction. However, stocks staged a massive turnaround midweek, driven by easing tensions in the Middle East and the largest initial public offering in U.S. financial history. Consumer staples and real estate led the market sectors, while information technology and communication services lagged. Crude oil prices reached an eight-week low as the potential for a deal to reopen the Strait of Hormuz gained traction. Gold prices declined for a second straight week on improving risk appetite.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The Consumer Price Index rose 0.5% in May and 4.2% over the last 12 months, marking its highest yearly level since April 2023. Energy prices, which rose 3.9%, accounted for over 60% of the overall May increase. Prices at the pump increased 7.0% in May and 40.5% over the last 12 months. Prices for shelter rose 0.3% in May, while food prices increased 0.2% over the month. Prices less food and energy rose 0.2% in May and 2.9% from a year earlier, which was the highest rate since September 2025.

- The Producer Price Index rose 1.1% in May, the same increase as in April. Producer prices increased 6.5% for the 12 months ended in May, the largest 12-month rise since moving up 7.4% in November 2022. Nearly 80% of the May advance in overall prices was attributable to a 2.8% increase in prices for goods, which was the largest increase since December 2009, when data was first calculated. Energy prices rose 10.7% in May (of which gasoline prices rose 23.4%), accounting for 80% of the overall increase in prices for goods. Goods prices less foods and energy rose 0.8% last month. Prices for foods increased 0.6%. Prices for services moved up 0.3% in May.

- The latest report on international trade in goods and services from the Bureau of Economic Analysis, released June 9, was for April and revealed the trade deficit was $55.9 billion, 1.2% less than the March estimate. April exports were $327.1 billion, 2.6% more than March exports. April imports were $383.0 billion, 2.0% more than March imports. Thus far in 2026, the goods and services deficit decreased $213.5 billion, or 49.1%, from the same period in 2025. Exports increased $128.2 billion, or 11.3%. Imports decreased $85.3 billion, or 5.5%.

- Sales of existing homes in May increased by 3.2% for the month and 3.2% since May 2025. Inventory sat at a 4.5-month supply in May, unchanged from the previous month but down slightly from 4.6 months one year ago. The median sales price, at $429,300, was 2.8% above the April figure and 1.3% higher than the price in May 2025. Sales of existing single-family homes increased 3.5% from April and 3.3% from a year ago. The median sales price for existing single-family homes in May was $434,300, up 2.9% from April and 1.3% higher than the price from May 2025.

- The government deficit for May was $293 billion. This followed April’s surplus of $215 billion. Through the first eight months of the fiscal year, the deficit sits at $1,246 billion, slightly under the deficit of $1,364 billion over the same period in the prior fiscal year.

- For the week ended June 6, there were 229,000 new claims for unemployment insurance, an increase of 4,000 from the previous week’s level. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended May 30 was 1.2%, unchanged from the prior week’s rate. The advance number of those receiving unemployment insurance benefits during the week ended May 30 was 1,795,000, an increase of 24,000 from the previous week’s level, which was revised down by 6,000. States and territories with the highest insured unemployment rates for the week ended May 23 were New Jersey (2.1%), Washington (2.0%), Massachusetts (1.9%), California (1.8%), Oregon (1.7%), Rhode Island (1.7%), Nevada (1.6%), New York (1.6%), Puerto Rico (1.6%), and Illinois (1.4%). The largest increases in initial claims for unemployment insurance for the week ended May 30 were in California (+3,532), Minnesota (+1,706), Tennessee (+1,671), Ohio (+1,342), and Illinois (+1,203), while the largest decreases were in Texas (-2,125), New Jersey (-901), Kansas (-726), Massachusetts (-669), and Florida (-607).

- The national average retail price for regular gasoline was $4.146 per gallon on June 8, $0.159 per gallon below the prior week’s price but $1.038 per gallon higher than a year ago. Also, as of June 8, the East Coast price decreased $0.145 to $3.990 per gallon; the Midwest price dipped $0.190 to $3.945 per gallon; the Gulf Coast price declined $0.161 to $3.643 per gallon; the Rocky Mountain price decreased $0.135 to $4.194 per gallon; and the West Coast price declined $0.142 to $5.358 per gallon.

Eye on the Week Ahead

The Federal Open Market Committee meets this week. With inflation at levels above the Fed’s 2.0% target and solid job gains, it is unlikely that the Committee will lower the federal funds target rate range at this time.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI, Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates).

© 2026 Broadridge Financial Solutions, Inc. All Rights Reserved.