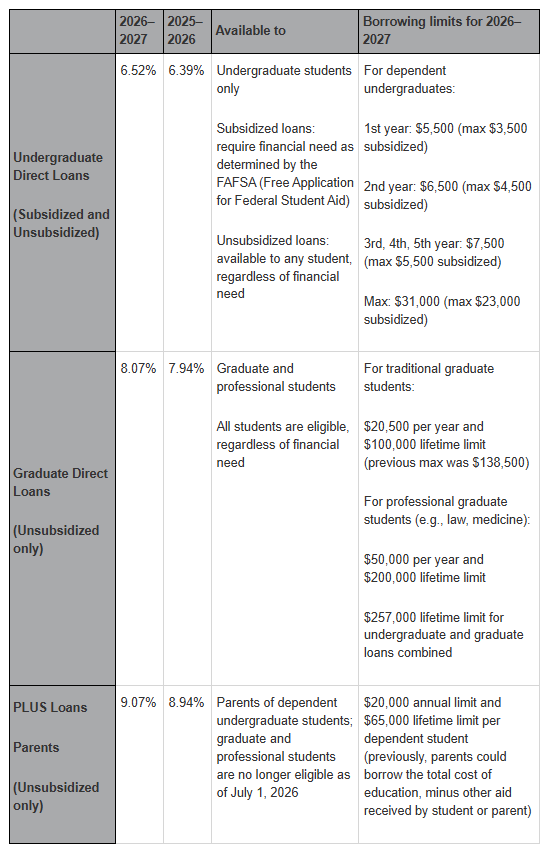

Every May, interest rates on federal student loans are recalculated for the upcoming school year. The rates are determined by combining the yield on the 10-year U.S. Treasury note with an additional fixed amount set by Congress. Based on this formula, interest rates on federal student loans are set to increase slightly for the 2026–2027 school year. The new rates apply to loans issued July 1, 2026, through June 30, 2027, (the rate is fixed for the life of the loan).

Interest rates aren’t the only thing changing for 2026–2027. New borrowing limits take effect July 1, 2026, pursuant to the One Big Beautiful Bill Act (OBBBA) that passed in July 2025. That legislation created new borrowing limits on Direct Loans and PLUS Loans, and eliminated the Grad PLUS Loan program.

Note: With a subsidized loan, the federal government pays the interest that accrues while the student is in school, during the six-month grace period after graduation, and during any authorized deferment periods, so no interest accrues for the borrower during those times.

With an unsubsidized loan, the borrower is responsible for paying the interest that accrues during these periods. If a borrower does not make payments on the accrued interest while in school, it will be added to the principal balance of the loan after graduation, a process called capitalization.

Two new student loan repayment plans

In addition to ushering in new borrowing limits for federal student loan programs, OBBBA also created two new student loan repayment plans that take effect July 1, 2026: the Tiered Standard Repayment Plan and the Repayment Assistance Plan. The plans are available to both undergraduate and graduate students.

Under the Tiered Standard Repayment Plan, a borrower will pay a fixed amount each month over a fixed period of time ranging from 10 to 25 years, depending on the loan balance:

- Less than $25,000 – 10 years

- $25,000 to less than $50,000 – 15 years

- $50,000 to less than $100,000 – 20 years

- $100,000 and over – 25 years

Under the income-based Repayment Assistance Plan, a borrower’s monthly payments will be based on his or her adjusted gross income (AGI) as follows:

- $10,000 or less – flat payment of $10 per month ($120 per year)

- $10,001 to $20,000 – 1%

- $20,001 to $30,000 – 2%

- $30,001 to $40,000 – 3%

- $40,001 to $50,000 – 4%

- $50,001 to $60,000 – 5%

- $60,001 to $70,000 – 6%

- $70,001 to $80,000 – 7%

- $80,001 to $90,000 – 8%

- $90,001 to $100,000 – 9%

- $100,001 and over – 10%

OBBBA also eliminates the Saving on a Valuable Education (SAVE) Repayment Plan, the Pay As You Earn (PAYE) Repayment Plan, and the Income Contingent Repayment (ICR) Plan by July 1, 2028. Borrowers currently enrolled in one of these plans must transition to a new repayment plan by July 1, 2028, which could include either the Tiered Standard Repayment Plan or the Repayment Assistance Plan. Borrowers should receive more information from their loan servicer.

Prepared by Broadridge Advisor Solutions. © 2026 Broadridge Financial Services, Inc.