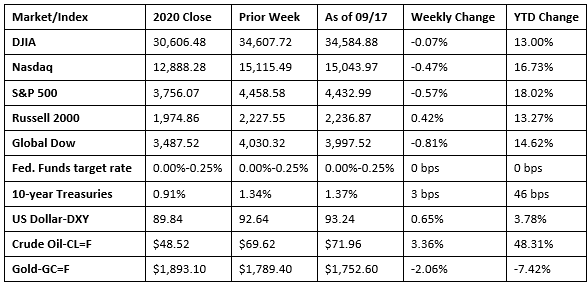

Stocks have generally retreated in September on concerns that the Delta variant is slowing the economy’s rebound and that the markets, which had been surging, may be primed for a decline. The benchmark indexes generally lost ground for the second consecutive week, with only the Russell 2000 able to close the week in the black. Ten-year Treasury yields climbed 3 basis points last week, the dollar climbed higher, and crude oil prices increased $2.34 per barrel. Among the market sectors, only consumer discretionary (0.5%) and energy (3.3%) advanced. The remaining sectors lost value, led by materials (3.2%) and utilities (3.1%).

Wall Street opened last week mostly higher, with each of the benchmark indexes listed here advancing, except for the Nasdaq (-0.1%). The large caps of the Dow (0.8%) and the S&P 500 (0.2%) gained ground, as did the small caps of the Russell 2000 (0.6%) and the Global Dow (0.7%). The market sectors were mixed to higher, with energy gaining 2.9% and financials climbing 1.1%, while health care (-0.6%) and utilities (-0.2%) dipped. Crude oil prices eclipsed the $70.00-per-barrel price for the first time since early August. The dollar was little changed, and 10-year Treasury yields slid.

Last Tuesday was another rough day on Wall Street. Each of the benchmark indexes fell, as the spread of a COVID-19 outbreak in a Chinese province raised trade concerns and worries that economic growth would be hindered. The Russell 2000 dropped 1.1%, followed by the Dow (-0.8%), the Global Dow (-0.6%), the S&P 500 (-0.6%), and the Nasdaq (-0.5%). Yields on 10-year Treasuries dipped to 1.27%, while crude oil prices and the dollar advanced. The market sectors hung back, with energy (-1.6%), financials (-1.4%), industrials (-1.2%), and materials (-1.2%) dipping the furthest.

Stocks closed higher last Wednesday as energy shares advanced notably. Aside from utilities, each of the market sectors rose, with energy climbing 3.8%, followed by industrials, materials, and financials. The Dow, the S&P 500, and the Nasdaq finished at least 0.7% in the black for the day. Ten-year Treasury yields and crude oil prices rose, while the dollar dipped.

Wall Street followed a positive Wednesday by retreating on Thursday. Among the indexes listed here, only the Nasdaq inched higher, as the remaining benchmarks ended the day in the red. Treasury yields rose and the dollar strengthened. Crude oil prices slipped lower. The energy sector has been volatile in September. Following a notable gain last Wednesday, energy fell 1.1% on Thursday. Among the remaining market sectors, only real estate and consumer discretionary edged higher.

Equities closed the week generally lower last Friday. Only the Russell 2000 was able to eke out a 0.2% gain. The Nasdaq and the S&P 500 fell 0.9%. The Global Dow dropped 1.0%, and the Dow declined 0.5%. Treasury yields and the dollar advanced. Crude oil prices dropped. Several of the market sectors decreased, with materials (-2.01%), utilities (-1.6%), information technology (-1.5%), communication services (-1.3%), and industrials (-1.1%) tumbling the furthest.

The national average retail price for regular gasoline was $3.165 per gallon on September 13, $0.011 per gallon less than the prior week’s price but $0.982 higher than a year ago. Gasoline production decreased during the week ended September 10, averaging 9.3 million barrels per day. U.S. crude oil refinery inputs averaged 14.4 million barrels per day during the week ended September 10 — 85,000 barrels per day more than the previous week’s average. Refineries operated at 82.1% of their operable capacity, up from the prior week’s level of 81.9%.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Last Week’s Economic News

- The August federal government deficit was $170.6 billion, down from July’s $302.1 billion. August expenditures totaled $439.0 billion ($564.1 billion in July), while receipts equaled $268.4 billion ($262.0 billion in July). Of the total receipts in August, $231.0 billion is attributable to corporate and individual income taxes. Social Security ($95.0 billion) and income security ($93.0 billion) accounted for 57% of the total government outlays in August. Year to date, the government deficit sits at $2,710.6 billion, 10.9% lower than the government deficit ($3,007.3 billion) over the same period last fiscal year.

- The Consumer Price Index rose 0.3% in August after rising 0.5% in July. Over the last 12 months ended in August, consumer prices have advanced 5.3%. The index less food and energy rose 0.1% in August, its smallest increase since February 2021. Price increases in gasoline (2.8%), household furnishings and operations (1.3%), food (0.4%), and shelter (0.2%) contributed to the overall CPI increase in August. Several indexes declined in August, including airline fares (-9.1%), used cars and trucks (-1.5%), transportation services (-2.3%), and motor vehicle insurance (-2.8%).

- Import prices fell 0.3% in August, the first decrease since October 2020. The August downturn was mostly driven by a 2.4% decline in petroleum prices. Despite the declines in August, prices for import fuel rose 56.5% over the past year. Export prices rose 0.4% last month, the smallest one-month advance since October 2020. Agricultural export prices increased 1.1%, while nonagricultural export prices inched up 0.2%, the smallest monthly increase since last October.

- Industrial production rose 0.4% in August after climbing 0.8% the previous month. Late-month shutdowns related to Hurricane Ida held down the gain in industrial production by an estimated 0.3 percentage point. Despite interruptions caused by the hurricane, manufacturing output increased 0.2%. Hurricane Ida impacted mining production, which fell 0.6%. Utilities increased 3.3%, as unseasonably warm temperatures boosted demand for air conditioning.

- Retail sales rose 0.7% in August over July. Retail sales have risen 15.1% since August 2020. Retail trade sales were up 0.8% last month and up 13.1% from a year ago. Clothing and clothing accessories stores sales were up 38.8% from August 2020, while gasoline station sales were up 35.7% from last year. Online sales jumped 5.3% in August after falling 4.6% the previous month.

- For the week ended September 11, there were 332,000 new claims for unemployment insurance, an increase of 20,000 from the previous week’s level, which was revised up by 2,000. According to the Department of Labor, the advance rate for insured unemployment claims for the week ended September 4 was 1.9%, a decrease of 0.2 percentage point from the previous week’s rate, which was revised up by 0.1 percentage point. The advance number of those receiving unemployment insurance benefits during the week ended September 4 was 2,665,000, a decrease of 187,000 from the prior week’s level, which was revised up by 69,000. This is the lowest level for insured unemployment since March 14, 2020, when it was 1,770,000. For comparison, during the same period last year, there were 860,000 initial claims for unemployment insurance, and the insured unemployment claims rate was 8.7%. During the last week of February 2020 (pre-pandemic), there were 219,000 initial claims for unemployment insurance, and the number of those receiving unemployment insurance benefits was 1,724,000. States and territories with the highest insured unemployment rates for the week ended August 28 were Puerto Rico (4.5%), California (3.7%), New Jersey (3.4%), the District of Columbia (3.3%), Illinois (3.1%), New York (3.0%), Rhode Island (2.9%), Connecticut (2.8%), Georgia (2.8%), and Hawaii (2.6%). States and territories with the largest increases in initial claims for the week ended September 4 were Louisiana (+7,664), Michigan (+5,318), California (+1,209), Kansas (+528), and Nevada (+420), while the largest decreases were in Missouri (-6,949), New York (-3,020), Florida (-2,482), Tennessee (-1,923), and Georgia (-1,814).

Eye on the Week Ahead

August data for the housing sector is available this week. The pace of sales for both new and existing homes has slowed from its torrid pace earlier in the year. The big news this week focuses on the meeting of the Federal Open Market Committee. It is possible that the Committee will present a firmer timeline for scaling back its current bond purchasing program.

The Week Ahead

The information provided is obtained from sources believed to be reliable. Forecasts cannot be guaranteed. Past performance is not a guarantee of future results.

© 2021 Broadridge Financial Solutions, Inc. All Rights Reserved.